From ANZ’s New Zealand economics team:

Housing market overview

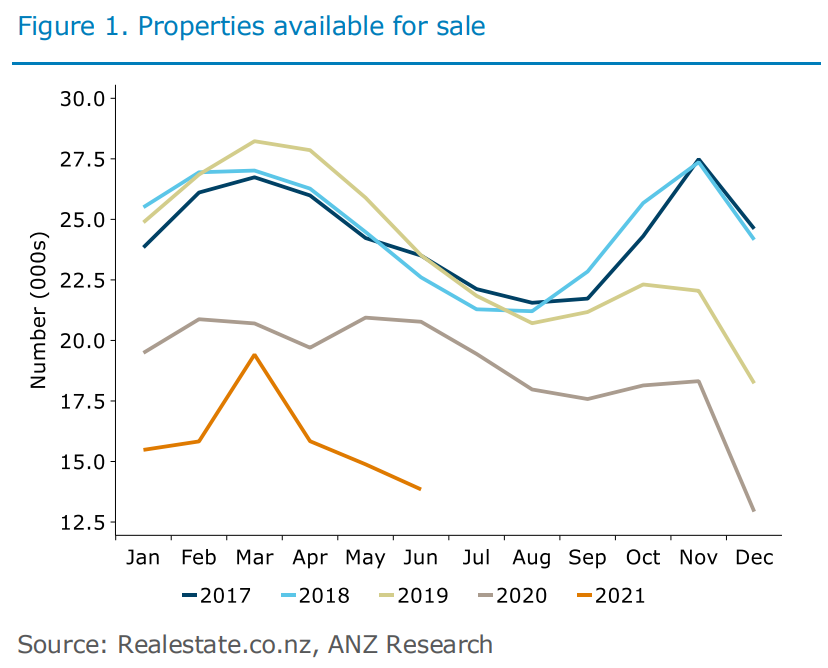

A few months have now passed since the Government announced its suite of housing policy changes, and as the dust settles, a rather robust market is being revealed. It’s still early days of course, but the experience to date suggests policy changes so far are not on their own going to bring about different, and more equitable, housing outcomes. House price inflation is still running at an elevated monthly pace, and while we think the annual profile is very close to its peak, the ratio of house prices to incomes is simply off the chart. Properties

available for sale remain very low, and the only real solution to this madness in the longer run is to build more houses. For now, the market remains tight, but a higher OCR from August should help take some of the heat out.

A tight market…

Housing indicators continue to point to a very tight market. Days to sell remain low, coming in at 30 in June (historical average: 39) and properties available for sale remain exceptionally low (figure 1). It’s no wonder price pressures have remained elevated as investors have taken a back step – low inventory means first-home buyers are competing for properties just as hard as ever.