Recent data from the Reserve Bank of New Zealand (RBNZ), collated by Interest.co.nz, showed that Kiwis leveraged big time into property ahead of the Ardern Government’s investor tax reforms (announced in late March).

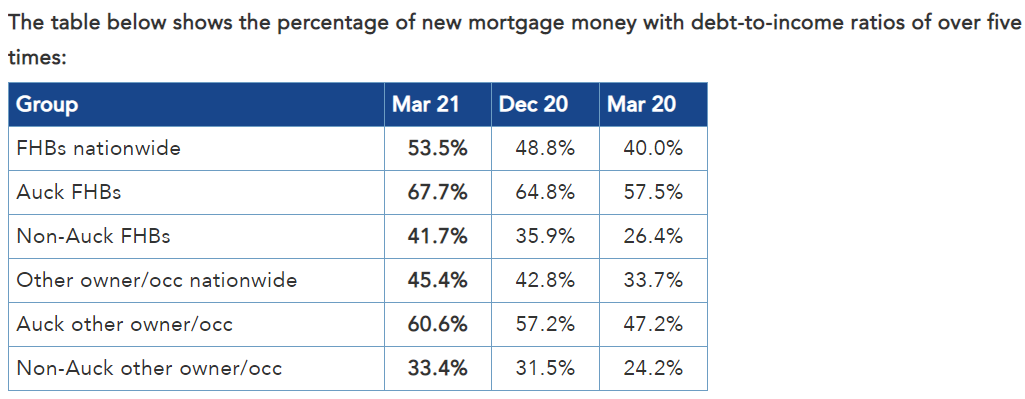

The proportion of new mortgages taken out with debt-to-income (DTI) ratios above five soared over the March quarter, with all borrower groups rising:

New Zealand DTIs rose significantly as property prices surged.