Moody’s with the note:

As economic recoveries proceed at different speeds and stages around the globe, there is rising interest about when normalisation of monetary policy will begin. Many central banks have had interest rates sitting at the lower bound since providing unprecedented monetary support at the height of the global pandemic. Normalisation of the U.S. federal funds rate could begin in early 2023, while tapering of the Federal Reserve’s quantitative easing could begin in January. This will likely prompt some emerging markets, including in Asia, to follow suit. Indeed, Mexico’s central bank surprised on Thursday with a rate hike, encouraged by high inflation. Market pricing suggests further increases are coming in Mexico in the near term.

Interest rate hikes in 2022 are looking more probable for some developed Asia-Pacific economies, including New Zealand, provided economic recoveries remain on track.

Australia could move sooner than expected

Central banks in South Korea and New Zealand have been the first in the region to openly float the idea of interest rate increases. The Reserve Bank of New Zealand has predicted that its official cash rate will begin increasing in the second half of 2022. The Bank of Korea has begun talking about an “orderly exit” from record low rates sometime in the future, with the second half of 2022 also the likely start date.

The Reserve Bank of Australia has indicated that it will not increase rates until the economy is at full employment and inflation sustainably returns to the 2% to 3% target, a situation unlikely to occur until the second half of 2023. But rate increases could come earlier. Strong labour market figures for May, where the unemployment rate dropped to 5.1% from 5.5% in April thanks to strong gains in employment even as the participation rate increased, suggest that the likelihood of this rate profile being brought forward has increased.

The sustained low interest rate environment is leading to pockets of rising concern in Australia, with household credit sustainability a particular pressure point.

Macroprudential tools useful for the housing market

Macroprudential tools are particularly useful with sustained low interest rates, because they can target pockets of concern. The Australian Prudential Regulation Authority is on the verge of intervening in the housing market to cool the spectacular momentum experienced across capital cities; similar intervention has previously occurred.

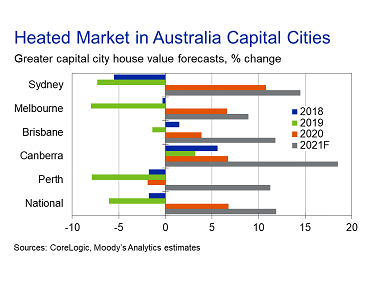

National dwelling values have increased 9.1% y/y in May, according to CoreLogic data. Sydney dwellings have increased 11.2%, Brisbane was up 12.1%, and Melbourne has gained 5%. The strong runup in home values has been spurred by sustained low interest rates and unprecedented fiscal support against the backdrop of an economy that is healing from the worst of COVID-19.

We forecast national dwelling values to rise 12% in 2021, after the 6.8% expansion in 2020. Sydney is forecast to rise 14.5% in 2021 after gaining 10.8% in 2020. Melbourne is forecast to rise 8.9% and Canberra an impressive 18.5%.

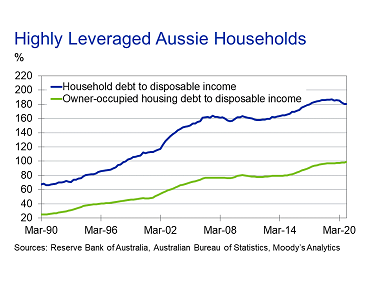

An environment where credit growth far outpaces income growth is unsustainable. Household debt is already elevated, sitting at 180.4% of disposable income in the December quarter. The ratio of owner-occupied housing debt to disposable income was 99% in the December quarter, up from 94.3% in 2017. There is a strong causal link in Australia between rising house prices and household debt.

An underlying concern is that when interest rates do eventually rise, highly leveraged households need to be able to continue servicing their loans, even if rate increases are forecast to be gradual.

Taking a broader view, household consumption typically accounts for around 55% of GDP. If households are put under stress from rising lending rates, there will be broader macroeconomic implications as they pull back on spending in other areas. In addition, most home mortgages in Australia are floating, making households vulnerable to interest rate shocks.

An estimated 20% of Australia’s population is under “mortgage stress”—a concern given lending rates are at historical lows. Mortgage stress is defined as those who pay over 30% of household income in mortgage repayments.

The underlying concern prompting likely regulator intervention has been that lending standards do not remain sound. In mid-June, the Council of Financial Regulators (composed of the APRA, RBA, Australia Securities and Investments Commission, and Treasury) acknowledged that there had been some deterioration, a first since late 2018, when the CFR began issuing quarterly statements of concern around the housing market.

New Zealand’s similar experience

Australia isn’t alone in the region when it comes to high household debt. South Korea and New Zealand also have relatively high household debt-to-disposable income ratios. A key driver of South Korea’s elevated household debt is credit card spending. In New Zealand, as in Australia, it is the housing market.

New Zealand’s heated housing market attracted action from the regulator earlier this year, after national prices rose 20% in 2020. New Zealand has made it less attractive for investors to speculate in the property market in addition to increasing deposit requirements. Debt-to-income limits will be applied to limit borrowing capacity. It’s likely Australia will follow a similar path. There is a lag of at least six months between intervention and housing value growth materially cooling.

Macroprudential tools are particularly useful in the sustained low interest rate environment. Rate increases are not expected in Australia for at least another year. It is likely they will be increasingly used throughout Asia-Pacific as low interest rates and burgeoning economic recoveries lead to pockets of concern. Household credit sustainability will be a particular pressure point.