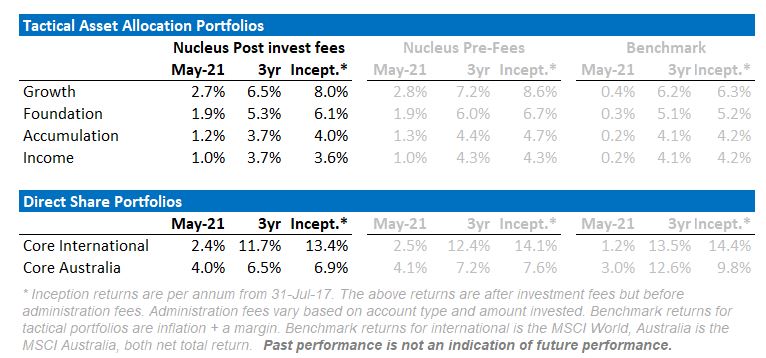

The market is oscillating between value and growth months. In May it was the turn of value portfolios (including ours) to outperform. Our direct equity portfolios beat benchmarks by over 1% on the month and our tactical asset portfolios finished up between 1% and 2.7%.

We have, however, called time on the value trade. The current inflation spike looks to be short term and will likely recede over the next six months.

Portfolio Repositioning

We repositioned portfolios accordingly in early June.

Our bond holdings were huddled at the short end of the curve, largely protected from rising rates. While bond yields did rise over the last few months, the bond market never really believed the “inflation is back” story. Bond pricing looks about right given the risks, and so we don’t feel the need to take too much of a bet in either direction. We are now much more “normally” positioned.

In our share portfolios, we have made some substantial changes to reduce weight to the stocks we perceive will be the losers from the new environment: banks, resources and value stocks.

The replacements are similar to the winners from 2020: quality growth (think profitable technology) and defensive. In effect it is a barbell portfolio containing part:

- Defensive stocks that are interest-rate sensitive. i.e. stocks whose valuations will benefit from lower interest rates

- Quality growth stocks. In a low growth world, stocks that can grow considerably above-trend become more attractive

If you were looking for maximum returns, you might buy “junk” growth stocks, ones with little to no earnings which often perform best in this type of environment. We look at our portfolios differently though. Risk is an important factor, and the junk growth stocks are far from cheap and have as much downside as they do upside.

Chinese growth is a major consideration. Debt growth has slowed considerably, and a broad range of measures are rolling over. There is a reasonable risk case that current conditions morph into a 2015-style Chinese slowdown which saw commodity prices tumble 50%+ and share prices down 10-15%. I’m much more comfortable owning quality stocks in that type of environment.

Over the month we put up a number of posts on inflation. This is the final in our series of four posts on the contrarian view for inflation. This time we look at what to do from an investment perspective.

The inflation head-fake

In part one, we looked at inflation today not being the same as inflation in the 1970s.

We looked in particular at issues that caused inflation in the 1970s and how the rules have changed since then. We looked at technology being inherently deflationary. Net result: a financial system overengineered to prevent inflation.

We looked at changes in inflation expectations and how it took 20 years to fall despite persistently low inflation. We looked at trade, demographics, debt accumulation and manufacturing. Net Effect: All suggest inflation will be harder to create.

Interested in discussing an investment with Nucleus Wealth with a member of a financial advice team? We offer complimentary sessions to discuss how the themes we discuss are affecting markets and how our portfolios are positioned to take advantage of them

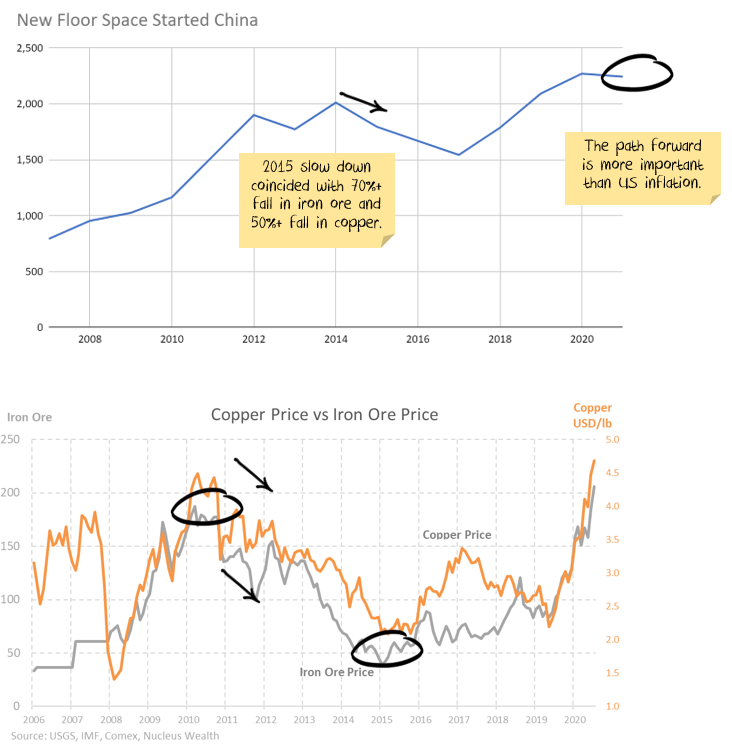

In part two, we approached the China inflation problem. Namely that commodity inflation is far more leveraged to Chinese stimulus than developed market stimulus.

We broke down the numbers to show that a bet on commodity prices is, in effect, a bet on Chinese housing construction. And the signs are ominous.

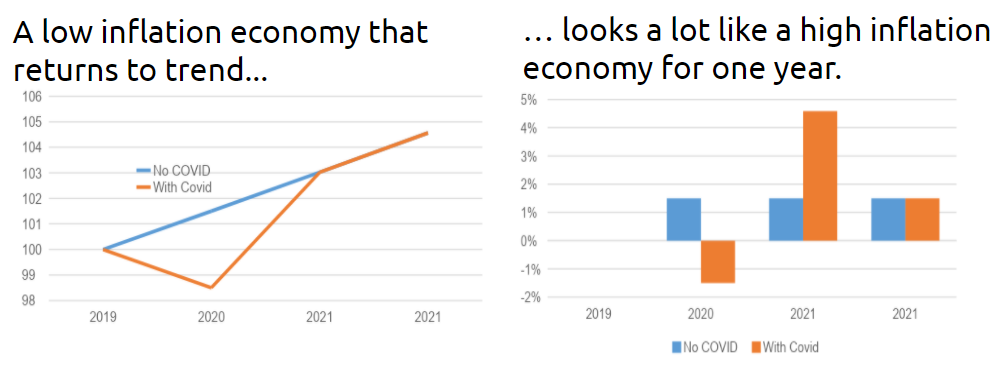

In part 3, we looked at the inventory supercycle. First we looked at how an inventory cycle disproportionally affects manufacturers on both upwards and downwards. We are in the upcycle now.

In addition to the usual cycle effects, retail demand has been juiced by a mix of stimulus cheques, lack of services, pent-up savings. Consumers have been spending on goods because they couldn’t spend on services. Manufacturing supply has been limited by COVID, the Suez canal blockage and changing demand patterns.

But inventory cycles are short. The price signals of today are building the excess capacity of tomorrow. The signs are good for economic growth but are not indicative of rampant inflation.

How should this shape your investment

The factor rotations that have dominated stocks this year can be divided into three narratives:

- Good news is bad news because rising inflation will drive bond yields higher and stock prices lower.

- Bad news is good news because low inflation will keep yields low enough for stocks to remain high.

- Good news is good news because Goldilocks inflation is enough to pop the “growth” stock bubble, but it will be offset by the rise of “value” stocks.

So far this calendar year, the last narrative has been the right one. If I may say so, it is also the narrative promulgated by MB Fund. So we positioned our post-COVID portfolio to capture the value upside and dodged growth stocks. We have outperformed in 2021 as a result.

Now we see conditions reverting back to bad news is good news as inflation falls, bonds rally and quality/growth stocks outperform for a time.

This is an investment timeframe of 12-18 months as the inventory supercycle and commodities bubble deflate owing to a combined Chinese and US growth air pocket that ends the great stimulus and global reopening boom.

From there, we will still have low unemployment in the US with a large $400bn per annum Biden stimulus lifting US growth towards 3% per annum for years. This holds out the real prospect for better wage gains and a grind higher for inflation through the cycle.

Therefore, we expect further dynamic portfolio management ahead.

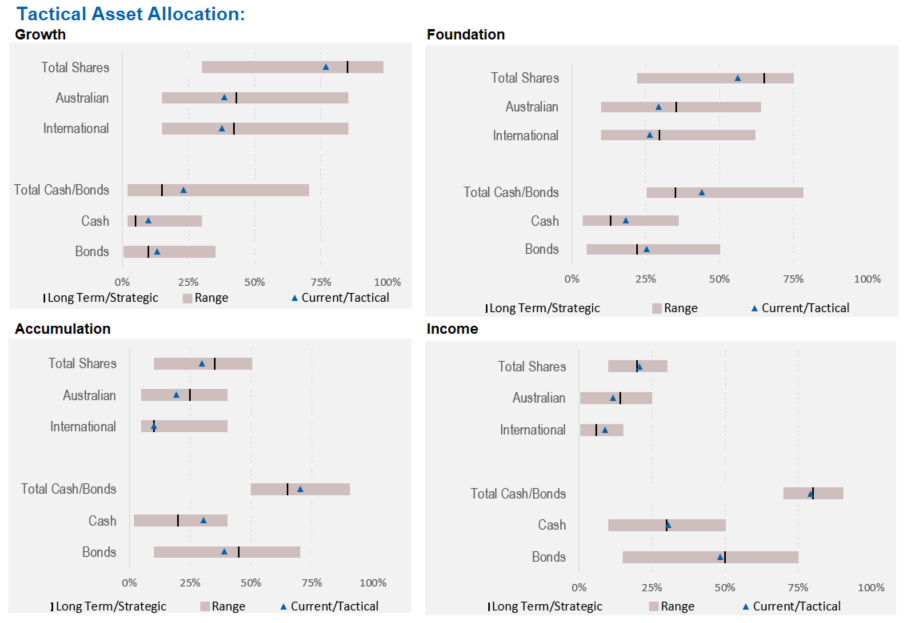

Asset Allocation

Markets continue to be expensive and while the grind higher is likely, there are also considerable downside risks. After a sell-off in mid-May, the equity markets rebounded and continued to climb over the month, maintaining the year-to-date momentum. Our Core portfolios performed strongly, outperforming their respective indices, as our Cyclical stocks and Gold offset the sell-down in Travel and Technology stocks.

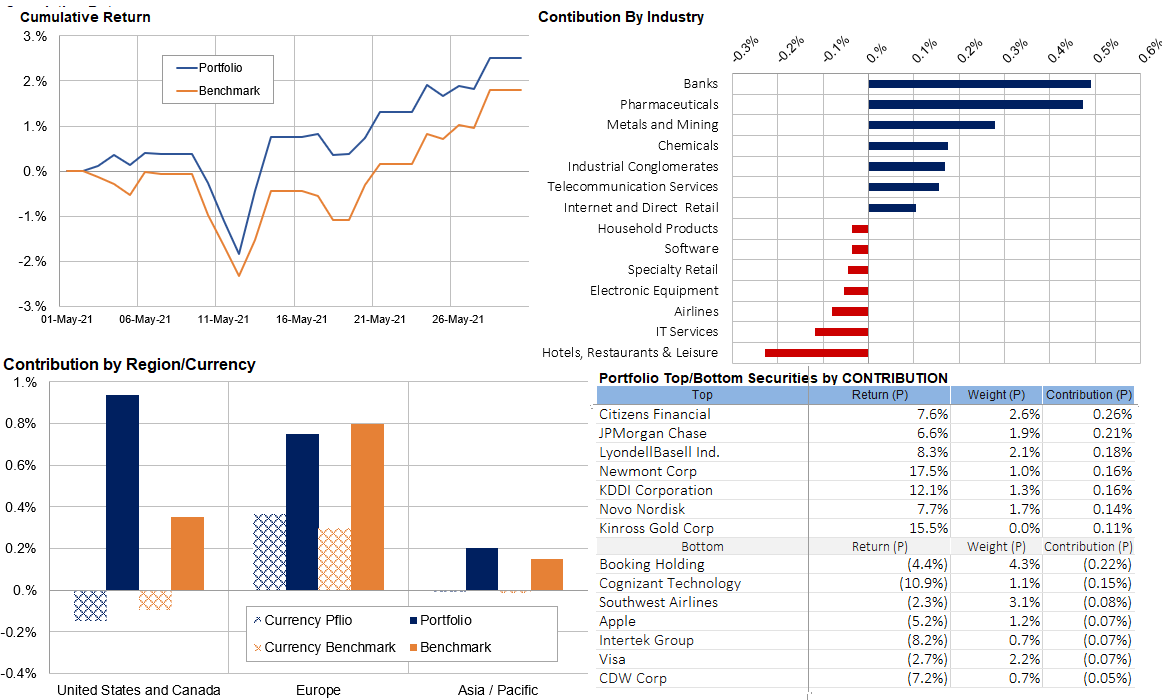

Core International Performance

Our international portfolio saw a 2.4% increase over May helped by US banks and Gold stocks, but our European Stocks put in a strong contribution this month. The currency effect further assisted our European returns while the stronger USD saw some modest headwinds for our North American exposures. Towards the end of the month, we took profits in some of our Gold and US Banks and increased exposure to REITs and other financial service providers.

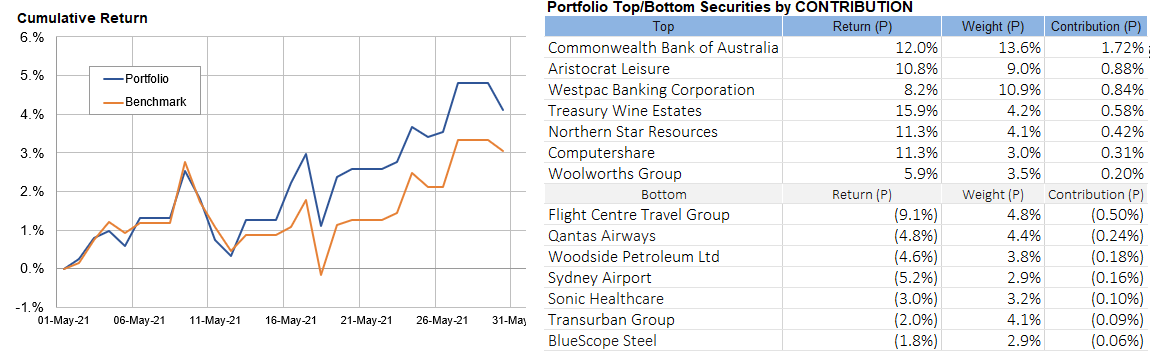

Core Australia Performance

The Core Australian portfolio outperformed the index this month as Banks put in a strong performance month and USD earners reversed last month’s weakness. Travel stocks were hit as Covid-19 fears resurfaced domestically. Over the month we trimmed out CBA, exited Worley and re-assigned it to CSL.

If you like to book a call with us then click through the below:

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.