Risk markets were once again constrained by the upcoming US unemployment print tomorrow night with Wall Street barely clocking over some gains despite a good lead from Asian shares yesterday. The Fed’s Biege Book surprised to the upside while the latest German retail sales number fell back unexpectedly. This caused a bit of volatility on currency markets with a lot of whipsaws but no real change at the end of the day as traders are poised for the NFP print instead. Commodity prices were also mixed with oil moving higher, making good on its recent breakout while copper and gold fell back.

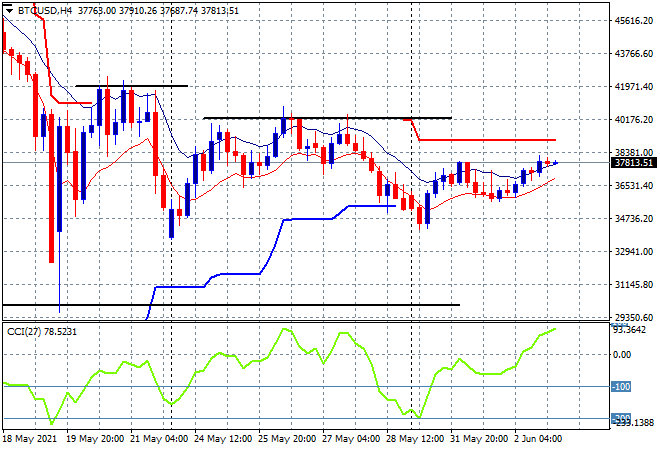

Bitcoin is trying to make some headway with a slight uptick overnight to just below the $38K level, trying to return to resistance at the $40K level from last week. Breakout above ATR resistance on the four hourly chart at the $39K would be a precursor to a wider move higher, but momentum is not yet accelerating:

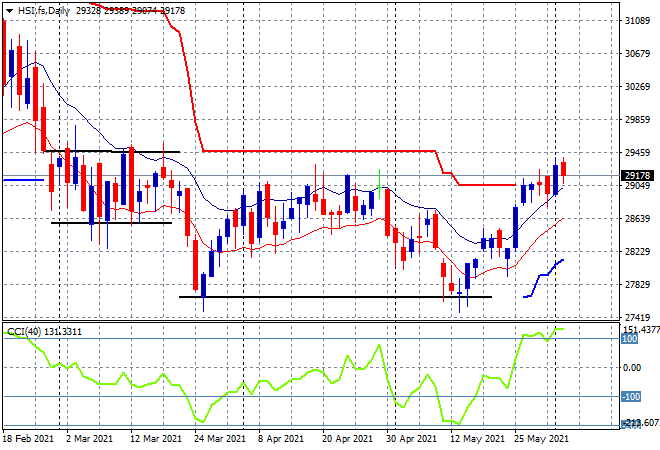

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite pulled back sharply, down nearly 1% to close at 3595 points while the Hang Seng Index whipsawed again, down nearly 0.6% at 29294 points. The daily chart was showing a clear bullish engulfing candle that confirmed the previous week of daily sessions bouncing higher off the March lows and while resistance at the 29000 point level has been cleared and daily momentum looks good, the high moving average needs to be supported here in the short term to call this a proper double bottom pattern:

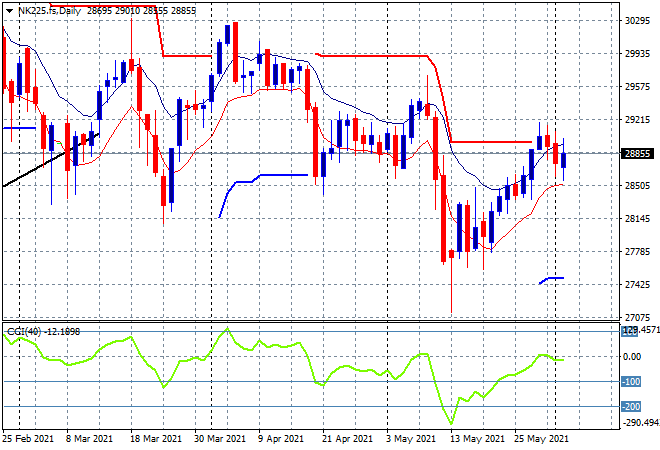

Japanese stocks moved out of hesitation mode again with the Nikkei 225 lifting 0.4% to close at 28944 points. Daily futures are looking a bit better too but there is still considerable resistance at the trailing ATR daily and psycholigcal 29000 point level to clear here, with session highs stalling out at the 29300 point level. Watch for the low moving average to come under pressure here:

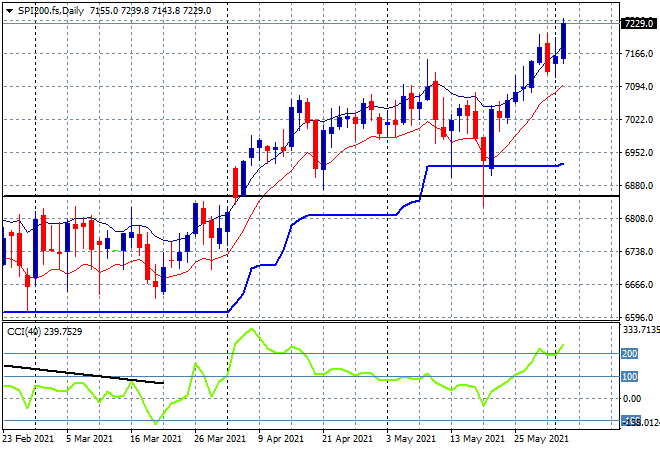

The ASX200 zoomed back to life on the latest GDP print, lifting over 1% to hold yet again well above the 7100 point level, closing at 7217 points. SPI futures are up around 15 points or so with this market given the green light by the RBA to head here, although momentum remains considerably overbought on the daily chart and ripe for another mild pullback on any overall risk aversion:

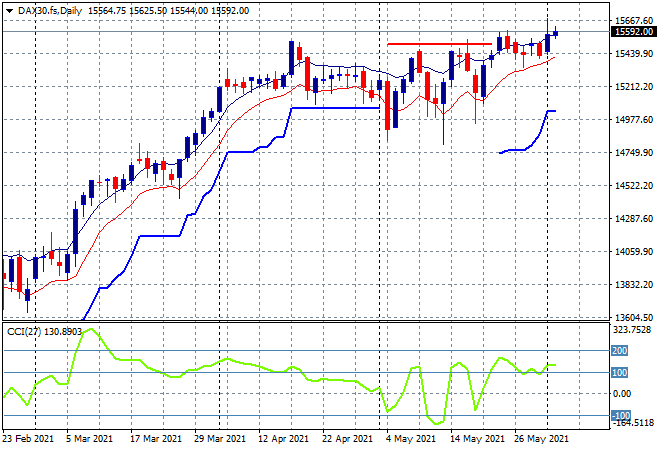

European markets were upbeat to start with but that German retail sales print thwarted larger returns with the German DAX climbing 0.2% higher to 15602 points. Sentiment is getting much more bullish now but the question is can it hold with reluctance still building intra-session:

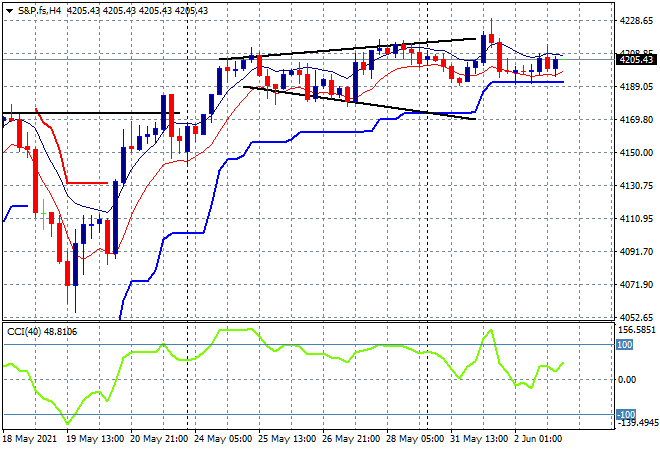

Wall Street remains relatively flat and waiting for the release of the month tomorrow night with the NASDAQ and S&P500 both only putting 0.15% with the latter finishing at 4208 points, still not getting excited above the 4200 point barrier. Price action on the daily chart is still showing an inability to decisively clear that 4200 level with momentum still nowhere near overbought readings:

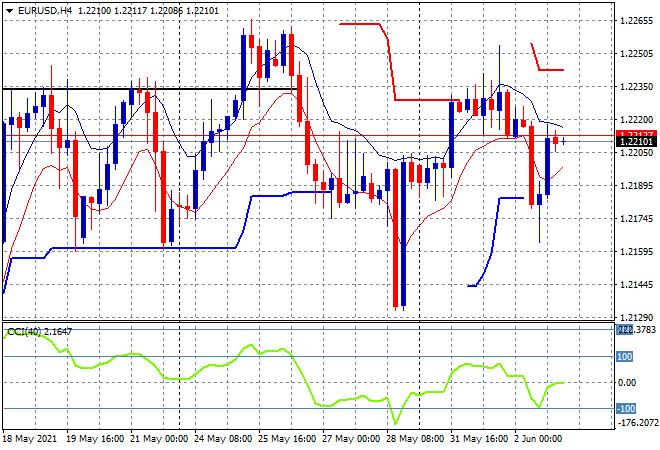

Currency markets again did another round trip but upped the volatility, this time around the German retail sales numbers with Euro initially falling straight through the 1.22 handle before recovering on the Fed Biege book release to be just above that level this morning. This does not bode well for reduced volatility at the end of the week, so it might pay to stay away until then:

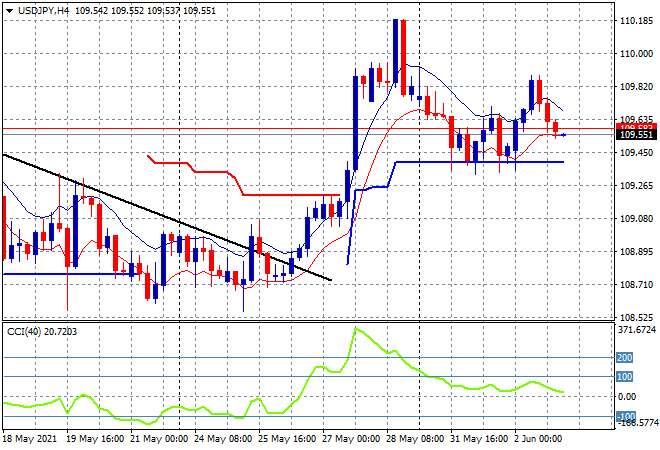

The USDJPY pair had a little breakout early in the session overnight, but this was taken back and then some as we go into the Tokyo open this morning, holding just above the mid 109 level. While low volatility did presage such a move, momentum never got anywhere near overbought to make this breakout stick, so keep watching below trailing ATR support here at the 109.30 level:

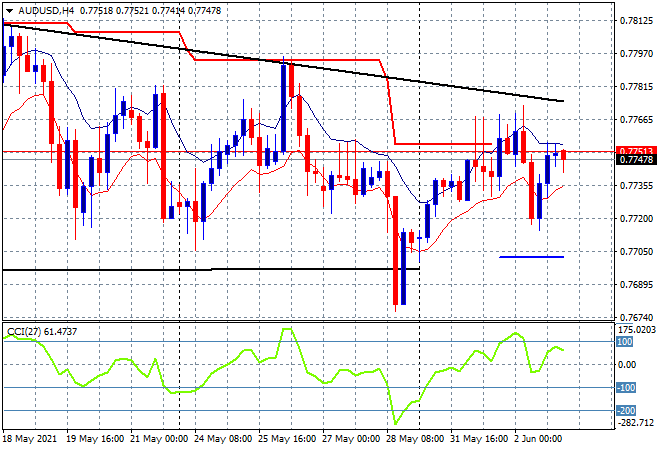

The Australian dollar is completely unable to get out of its funk and suffered a similar fate to Euro overnight with a dip and then a fill to be back at the mid 77 level this morning. As I said yesterday, price action on the four hourly chart was pointing to a rollover here and without a major spike in commodity prices, I’m watching for another break below the low moving average:

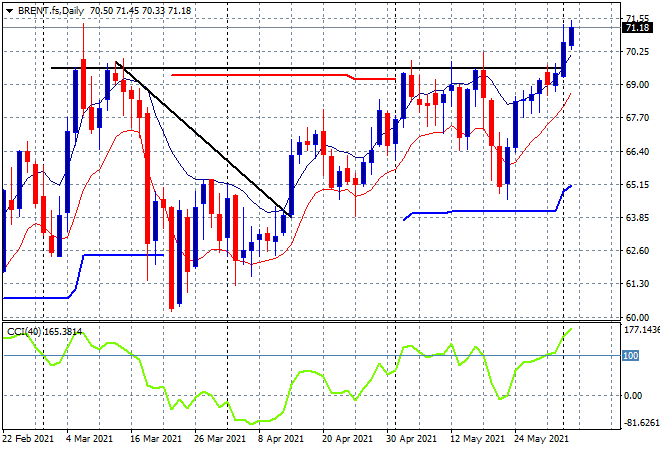

Oil has confirmed its recent breakout with another positive session above the previous resistance level that has held for months, with Brent crude pushing straight through the $71USD per barrel level to make another monthly high. As I said previously, traders will pile in now for a potential run up to the 2018 high at $83 or so:

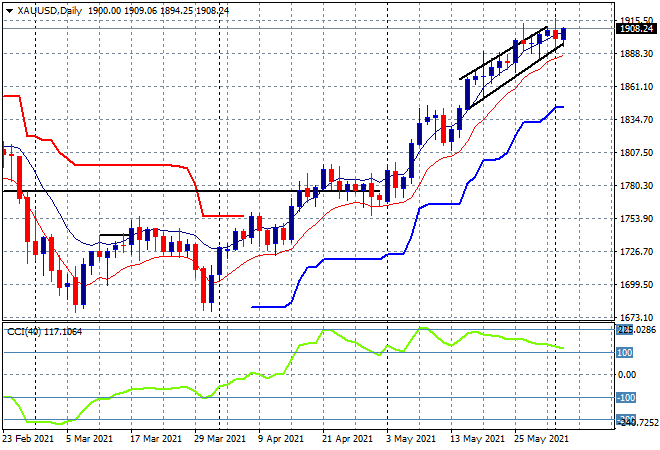

Gold was slowing down after trying to extend above the $1900USD per ounce level but unlike other majors is better supported although daily momentum continues to slightly decelerate. The next level to reach are the November 2020 highs at the $1960 level, with a clear uncle point at the low moving average to continue to add to positions, but watch for any pullback on profit taking:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!