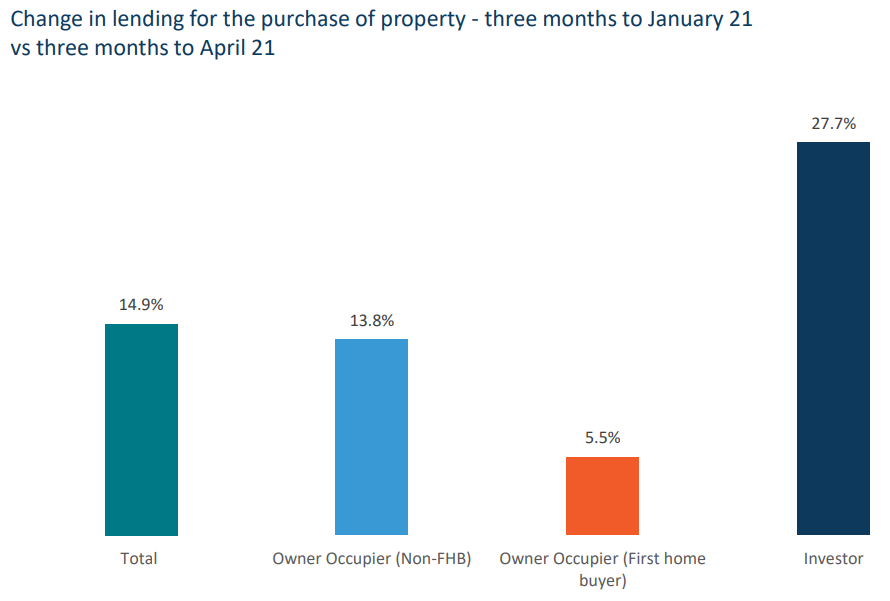

CoreLogic has released new data showing the increasing risk profile of Australian mortgage lending as investors have flooded back into the market.

Investors are storming back into the property market.

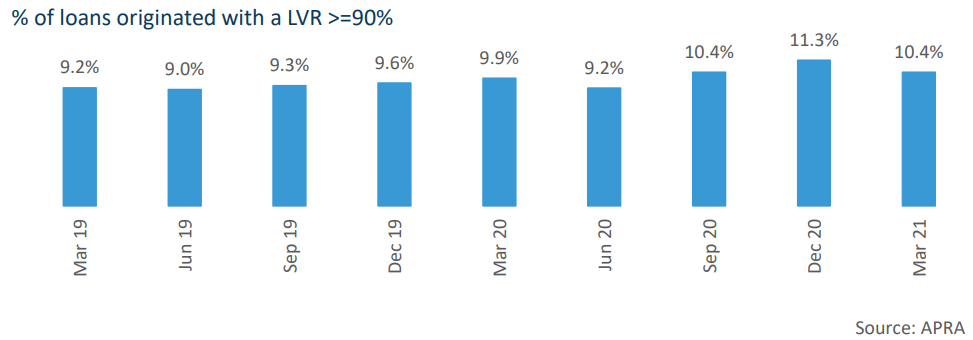

While the percentage of high loan-to-value ratio (LVR) lending fell over the March quarter to 10.4% from 11.3% – likely reflecting the reduction in first home buyers active in the market:

The percentage of high LVR mortgage lending fell in the March quarter.

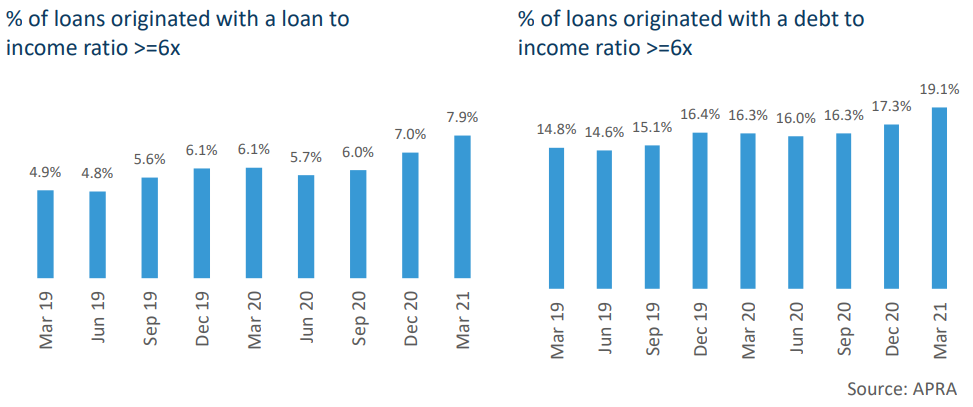

The percentage of mortgages written at high loan/debt to income ratios has risen sharply over recent quarters:

High debt-to-income borrowing on the rise.

Nevertheless, Core Logic does not believe that these figures warrant regulatory action in the market:

Part of the lift [in high loan to income lending] may be attributable to higher income borrowers being active in the market, with higher income households generally accounting for a large share of total household debt. This is also reflected in the faster capital growth rates currently observed at the higher end of the housing market, where high-end property buyers may be more active.

The increase in indicators for loans regarded as higher risk remains relatively low. This suggests that any short-term, formal policy changes to mortgage lending is unlikely. In the latest Quarterly Economic Review from CoreLogic, we noted there are also ‘softer’ signs of strong lending standards being enforced, with industry addresses and statements signalling the importance of monitoring and maintaining prudent lending standards. With property prices rising rapidly, any changes to credit availability would likely be communicated and deployed carefully.

My view is that we are unlikely to see regulatory action to curb the housing market until after next year’s federal election.

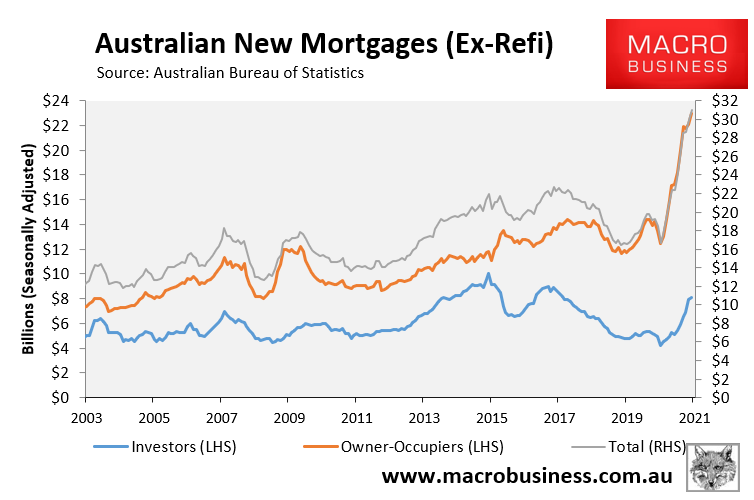

Despite the surge in interest from investors, their participation in the market remains well below prior peaks. This means that the housing market is still being driven by owner-occupiers:

Owner-occupiers still driving the mortgage market.

Whacking owner-occupiers with regulatory action is far more difficult politically than whacking investors.

Moreover, APRA chairman Wayne Buyers is politically indebted to Josh Frydenberg after he reappointed Byers despite APRA being shown as incompetent by the Hayne banking royal commission.

Thus, Wayne Byers will be loathe to take macro-prudential action that would upset the housing boom and put the Morrison Government’s reelection chances at risk.