By Gareth Aird, head of Australian economics at CBA

Key Points:

- The Australian labour market has tightened at a phenomenal pace and underutilisation in May was at its lowest since early 2013.

- The forward looking indicators of labour demand are very strong yet labour supply is constrained, which means the labour market will continue to tighten very quickly and wages growth will accelerate.

- The Commonwealth fiscal stance as well as the targeted level of net overseas immigration in 2022/23 will have a large bearing on nominal wage outcomes and therefore the path of interest rates.

- We expect the RBA to begin normalising monetary policy in late 2022 and see the cash rate target at 0.5% at end‑2022 and then peaking at 1.25% by Q3 2023.

Overview

For the past six months CBA’s economic forecasts for the Australian economy have been at odds with the RBA’s “2024 at the earliest” forward guidance on the cash rate. But we have refrained from calling a hike in the cash rate until now because we believed that markets were more focussed on the RBA’s policy decisions around yield curve control (YCC) and the bond buying program.

As far back as November 2020 we remarked that, “we think that the economy will be on a sufficiently entrenched path of improvement by the middle of next year (2021) that the RBA will need to either remove or increase the target yield on the 3 year Australian Commonwealth Government Bond (ACGB)”.

Our views on the economy and the RBA were very much non‑consensus at the time. But financial markets started to support our call on YCC in mid‑February when a kink developed in the three year part of the yield curve. The RBA was forced to defend its yield curve target by buying large quantities of the April 24 bond, while the yield on the November 24 bond climbed from 0.2% to 0.43% in just over a week.

Our central scenario in early 2021 was that the RBA would abandon YCC around the middle year. But in March 2021 the RBA stated that later in the year they would only consider whether to maintain the April 24 bond as the target bond or shift the focus of the yield target to the November 24 bond. That is, the Board would not consider removing the target completely or changing the target yield of 0.1%. As a result, we amended our call immediately to state that the RBA would keep the yield curve target pegged to the April 24 bond. At the time many high profile commentators were of the view that the yield curve target would be rolled out to the November 24 bond.

We still believe that abandoning yield curve control at the July board meeting is the most appropriate policy decision given the strength of the Australian economy. But the RBA has taken that option off the table.

Regular readers will know that CBA’s views on the outlook for inflation and wages have been consistent and unswerving over 2021 and they have differed significantly from the RBA’s view and at many times the consensus. We have naturally made upgrades to our forecast profile over the year given the strength of the economic data. But our message has been the same ‑ the labour market will tighten quickly and this means that wages and inflation will lift, particularly because the supply of labour is constrained and this has pushed the NAIRU higher.

In a recent paper we articulated the reasons why, “this time is different”. Our intention was to raise awareness amongst our readers about why the economic backdrop today is so much more conducive to higher wages and inflation than it was pre‑COVID. Our view that we are in a more inflationary environment ultimately has an impact on the outlook for monetary policy. But we refrained from calling a hike in the cash rate as we wanted readers to focus on the story rather than simply the RBA call.

Today we take our narrative on the economy one chapter further to formally include monetary policy tightening in the form of interest rate hikes into our forecast profile. This is not a change in view per se, but rather it is the natural extension to the themes we have discussed for some time on wages and inflation.

Our central scenario has the RBA delivering the first hike in the cash rate in November 2022. We have pencilled in an increase of 15bp which would take the cash rate to 0.25%. We expect that to be followed by an increase of 25bp in December 2022. We have three further 25bp hikes in Q1 23, Q2 23 and Q3 23 that would take the cash rate to 1.25%, the level at which we assess the cash rate to be neutral.

The risks are not all one way. There are scenarios that could see the RBA pull the rate hike trigger earlier than November 2022, particularly if they tweak their reaction function because it becomes irrefutable that wages growth is on a path to 3% per annum (the rate of growth they have targeted). Alternatively, the RBA could delay hiking the cash rate if growth in labour supply was to accelerate quickly when the international border is reopened.

We believe that the RBA cannot achieve their objectives of full employment and inflation “sustainably in the target” without the assistance of the Commonwealth Government. More specifically, fiscal settings need to remain stimulatory and net overseas immigration cannot catapult back to strong pre‑COVID levels if wages growth is to remain at 3% per annum or above.

As such, there are two key assumptions that underpin our RBA call: (i) fiscal policy remains expansionary over the next few years; and (ii) net overseas immigration increases from mid‑2022, but at a slower rate than pre‑COVID.

Whilst there is a high degree of uncertainty over our second assumption, we think that policymakers are more cognisant of the link between immigration and wages due to the pandemic. As a result, we anticipate immigration targets will be recalibrated so that the desired tightening in the labour market is not derailed by the reopening of the international border. A more nuanced approach to population policy will enable higher wage outcomes to materialise in a sustainable way and will allow monetary policy to be normalised.

Ultimately elected policymakers will play the more dominant role in determining wages and inflation outcomes in Australia than the monetary authorities. This means that those interested in the outlook for interest rates should pay close attention to government decisions on fiscal policy and immigration, as of course we will.

In this note we discuss the outlook for the labour market, wages and inflation and how that pertains to monetary policy. Our full updated economic forecasts will be published in Friday’s weekly Perspective.

How quickly will the labour market continue to tighten?

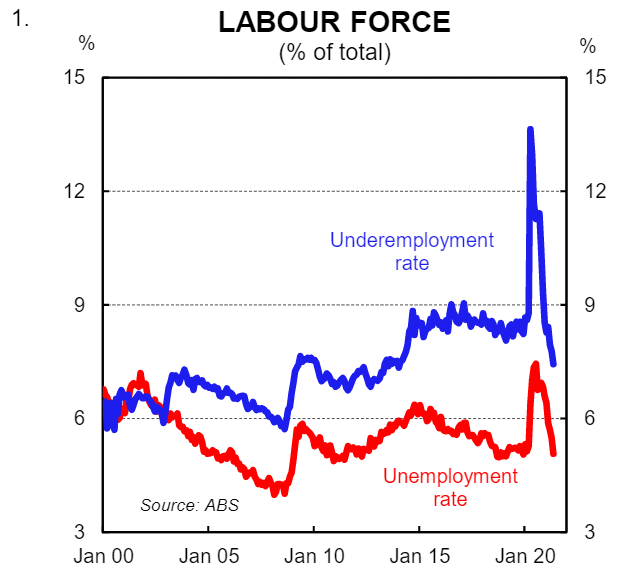

The speed at which the labour market has tightened has been phenomenal. In April 2021weforecast that the unemployment rate would end the year at 5.0%(the same as the RBA’s updated forecast in the May2021Statement on Monetary Policy). But the May labour force survey blew that forecast out of the water because the unemployment rate printed at 5.1% (chart 1).

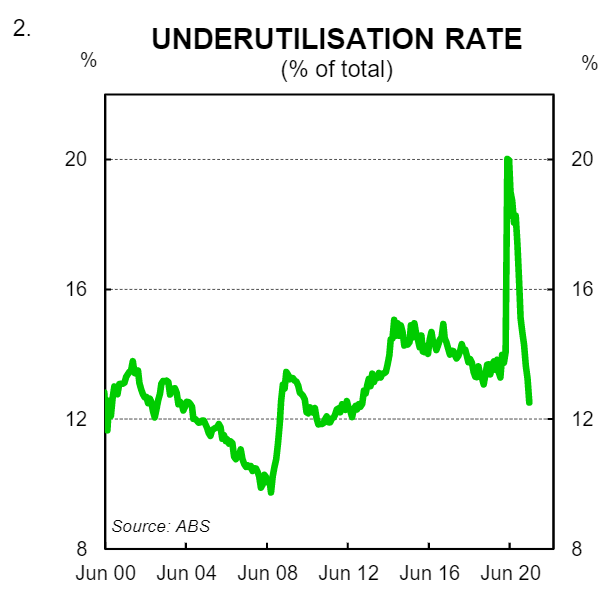

It’s not just about the unemployment rate. The underemployment rate has also fallen sharply and sits at its lowest level since January 2014. The underutilisation rate, which is the broadest measure of labour market slack,declined toits lowest level sinceFebruary2013in May (chart 2).

Clearly the closure of the international border has accelerated the tightening in the labour market. On our calculations the number of non-resident workers has declined by 286k or 55% over the year to the Q1 21. This helps to explain why job vacancies are so high despite employment, as measured by the monthly labour force survey, sitting comfortably above its pre-COVID high. But the international border closure is only part of the story. Unprecedented fiscal and monetary policy stimulus has also turbo charged the economy and job creation.

The Government’s Internet Vacancy Index revealed that job advertisements rose by 1.9% in May to sit a whopping 46.0% above their pre-COVID-19 level. Vacancies sit at their highest level in over 12years.The surge in vacancies is broad-based across a whole range of industries, states and skill levels.

Given the starting point for the labour market and the forward looking measures of labour demand we now forecast the unemployment rate to be 4.5% at end-2021 and 4.0% by end-2022.

What does it mean for wages?

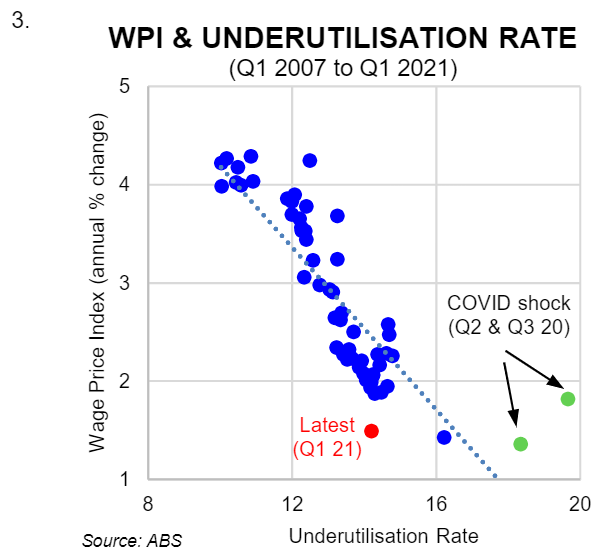

The relationship between the unemployment rate and wages growth has not been strong in recent years. But that is because the spread between the underemployment rate and unemployment rate is not constant and had widened pre-COVID. Put another way, changes in the unemployment rate alone are not a sufficient proxy for changes in labour market slack if the spread between the unemployment and underemployment rates is moving. As such, the underutilisation rate is a much better guide for labour market slack.

There is a strong historical relationship between underutilisation and wages growth (chart 3). The relationship is intuitive –higher wages growth occurs with a tighter labour market. And the best measure of the tightness in the labour market is the underutilisation rate.

We expect the underutilisation rate to decline to 11¼% by end-2021 and to 10% by end-2022. This will put a lot of upward pressure on wages growth and the bargaining power between employers and employees will shift in favour of workers.

In a speech on 17 June RBA Governor Lowe stated that, “most businesses feel they are operating in a very competitive marketplace and that they have little ability to raise prices. As a result, there is understandably a laser-like focus on costs: if profits can’t be increased by expanding or by raising prices, then it has to be achieved by lowering costs”.

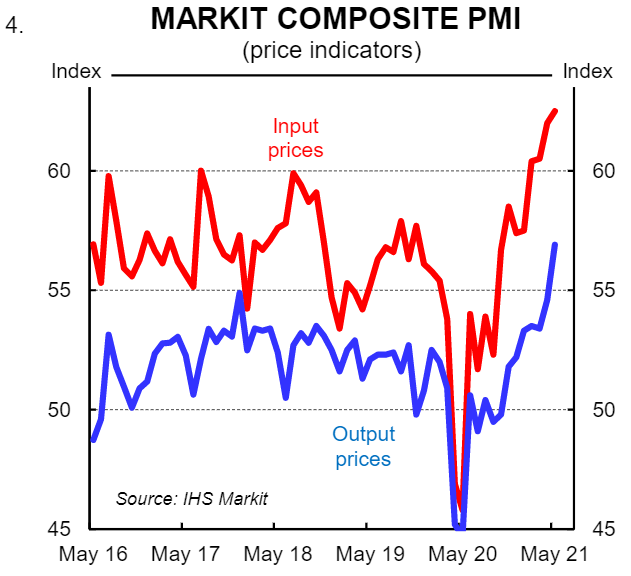

That may be true in terms of how businesses ‘feel’. But a number of private surveys indicate that businesses are acting differently. The old adage that actions speaks louder than words rings true.

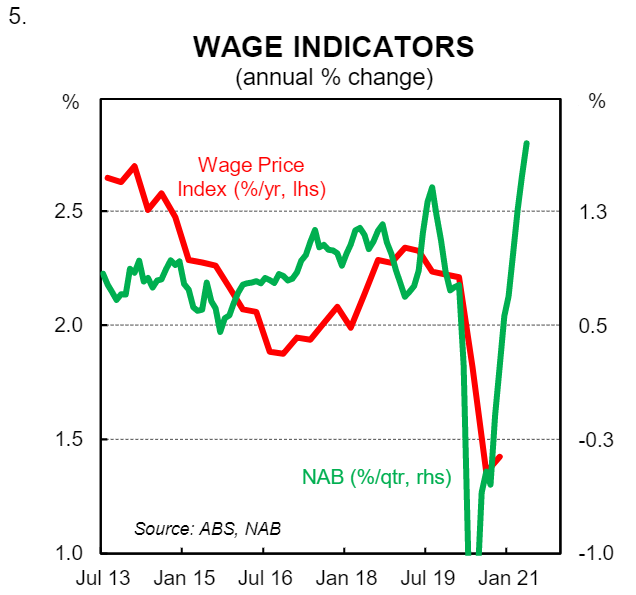

The Markit PMIs, for example, indicate that both input and output costs are rising (chart 4). And the NAB Business survey suggests that labour costs are lifting very quickly (chart5). The results of both surveys are not surprising to us because they are consistent with the conversations we’ve been having with our clients.

The laws of supply and demand still work. If firms are struggling to recruit they will be forced to pay higher wages. And many firms will pass on the lift in input prices in an environment of rising aggregate demand to protect their margins. This is how the wages and inflation nexus works.

We forecast wages growth to accelerate to 2.4%/yr by end 2021 and 2.9%/yr by end-2022. There will be a lag between falling underutilisation and wage outcomes in 2021 given the pace at which the labour market is tightening. But we expect the historically strong relationship between wages growth and underutilisation to reassert itself over 2022.

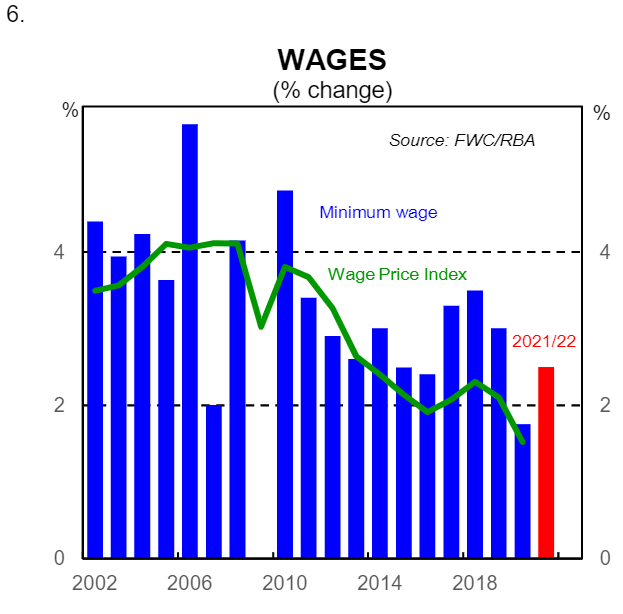

Higher wages outcomes will beget more entrenched expectations of higher wages. In that context the recent move by the Fair Work Commission to lift the minimum award wage increase from 1.75% in 2020/21 to 2.5% in 2021/22 is a welcome development (chart 6). The decision by the NSW Government in the 2021 Budget to increase public servant salaries by 2.5% each year (from 1.5%)will also have a similar impact on both wages momentum and expectations.

There is also a risk that the upcoming 0.5% increase in the general superannuation guarantee, which takes the rate from 9.5% to 10.0% from 1 July 2021, weighs on the WPI in Q3 21 if firms reduce the take home pay of workers to fund the increase. Whilst we expect some firms will do that, we think that the bulk of businesses will fully fund the increase, particularly in light of the tightness in the labour market and the need to retain staff.

What does it mean for inflation?

A lift in wages growth will pull consumer inflation ‘sustainably’ higher. We have forecast the trimmed mean to be1.8%/yr by end-2021 and 2.2%/yr by end-2022. Headline inflation is expected to be 1.8%/yr by end-2021 and 2.3%/yr by end-2022. The gap between headline and underlying inflation is small as compared with previous years given the price of tobacco will not boost headline inflation over the next two years as it has done over the recent past.

Our forecasts for the wage price index and CPI imply that real wages growth will average 0.5% per year over the next two years. But that is a little bit deceiving. We believe that the CPI is undershooting actual inflation at the moment because it is based on capital city indexes which measure price changes across each capital city in Australia individually. It does not include price changes in regional Australia. In ‘normal’ times this does not matter much. But we suspect that price rises in regional Australia have been stronger than in the capital cities at an aggregate level due to the relative strength of spending, employment and housing (particularly rents).

When does the RBA hike?

Picking the exact meeting that the RBA first hikes the cash rate is in many respects false precision. But our central scenario has the RBA delivering a first hike in the cash rate in November 2022.

By late 2022 there is likely to be a euphoric mood amongst consumers and businesses as COVID-related disruptions to day today life are a thing of the past. The resumption of international services trade will be the icing on the economic cake and we expect the Australian economy to be running at maximum capacity provided the Government has not shifted strategy to tighten fiscal policy.

In summary, our forecasts for wages growth and inflation meet the conditions for a rate hike in late-2022. And given wages growth and consumer inflation are lagging indicators we do not believe the RBA will delay tightening monetary policy once actual outcomes confirm that inflation is ‘sustainably within the target’.

How far and fast does the RBA go and where do they stop?

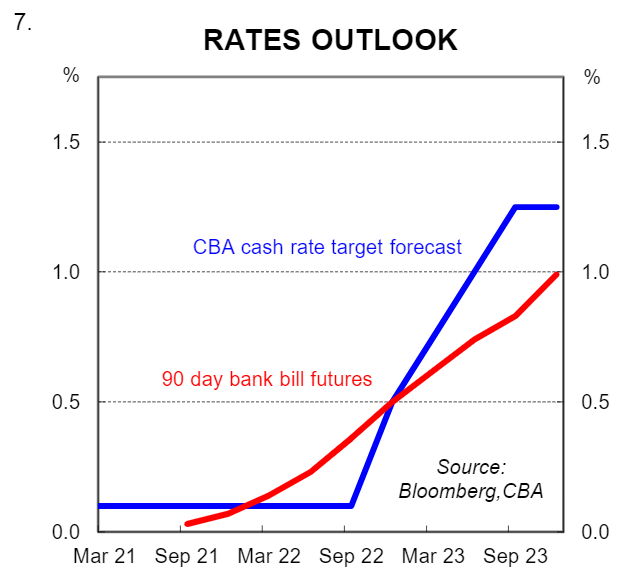

We have pencilled in a first increase of 15bp in November 2022, which would take the cash rate to 0.25%. We expect that to be followed by an increase of 25bp in December 2022. We have three further 25bp hikes in Q1 23, Q2 23 and Q3 23 that take the cash rate to 1.25%(chart 7).

Typically when a central bank seeks to normalise monetary policy the first stopping point is “neutral” or the neutral interest rate. In the RBA’s case, the neutral rate is the cash rate consistent with full employment, trend growth and neither upward nor downward pressures applied on the price level through monetary policy. It can be thought of as the cash rate that exerts neither contractionary nor expansionary forces on the economy.

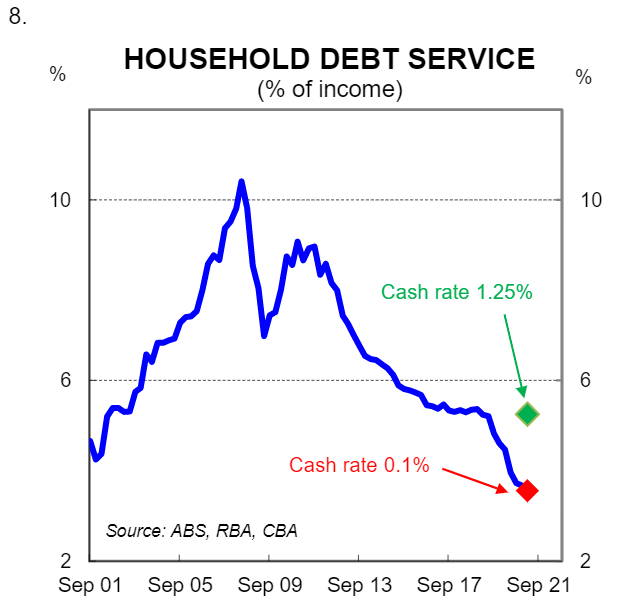

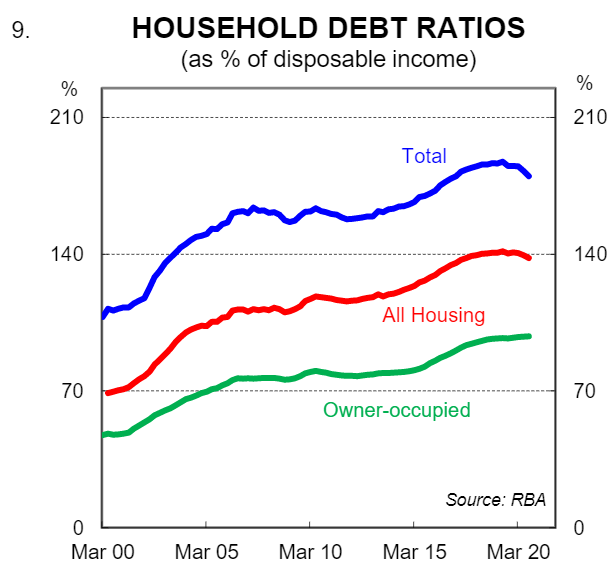

There are a variety of ways to estimate neutral. But the approach we prefer is to calculate the cash rate that would lift the interest paid on household debt as a share of household income to ~5¼% (the level which it averaged over the five years before the pandemic). We calculate that cash rate to be 1.25% (chart 8). Whilst that rate seems very low, it needs to be considered in the context of the level of household debt in Australia which is very high (chart 9).

Rate rises will have a large impact on the interest cost of servicing debt and our expectation is that the RBA does not need to hike too far to put the cash rate at neutral. Of course if the economy has over heated and the RBA needs to exert a contractionary force on the economy they will take the cash rate above neutral, but that is not our base case.

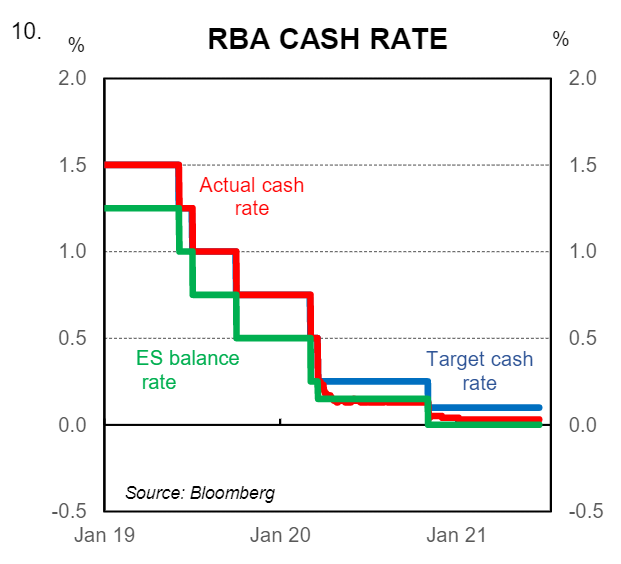

It is also important to note that changes to the RBA’s liquidity management framework over the past year mean that the exchange settlement (ES) balance rate is important when assessing the stance of monetary policy. The huge amount of liquidity poured into the financial system to lower interest rates and support the economy through the pandemic means that exchange settlement balances will remain elevated for many years. One result of the elevated exchange balances is that the interest rate paid on ES balances is now the main anchor for interest rates in the economy rather than the target cash rate (chart 10).

At this stage we expect that the RBA will initially maintain the current spread of 10bp between the target cash rate and the ES balance rate. A note on this topic will be published on Friday.

What does it means for bond yields?

At times through early 2021 it may have felt to our readers like our positive narrative on the Australian economy didn’t quite marry up with the house view on the yield curve and in particular longer dated swap and government bond yields. More specifically, our rates strategists did not expect the sell off in bonds over mid-February and March to last whilst the Australian economics team has continued to make the case that economic outcomes would surprise to the upside.

Our calls on the economy and the curve are reconciled not by different views of the world within the team, but rather technical factors which have suppressed bond yields. As such, our rate strategists have to date correctly held their nerve in not forecasting higher bond yields in the near term despite being blasted with a daily message of optimism on the domestic economy from me and my team!

Notwithstanding, our call for the RBA to commence a tightening cycle from November 2022 will have implications for the house view on the yield curve and our fixed income strategists will publish updated forecasts in due course. On this part, we already expect/forecast a jump in the 3-5Y tenors and see this area as the greatest risk for higher yields.

The July Board meeting–recap of CBA view

The RBA Board will make a decision on YCC at the July Board meeting and the bond buying program (QE).

The YCC decision will be around whether or not to extend the yield target from the April 24 bond to the next bond, which matures in November 24. We expect the RBA to keep the 0.1% target pegged to the April 24 bond.

The QE decision will be around what form additional bond purchases will take (the RBA has ruled out the cessation of bond purchases).

We expect the QE decision to constitute a taper (i.e. we do not expect a package that would result in the RBA continuing to buy bonds at the current pace of $A5bn a week). We favour the RBA announcing a package of $A50bn of bond buying over a six month period. The risk lies with a larger package or a pace of bond buying that is more than the pace implied by $A50bn over six months which is ~$A2.5bn per week.

Final thoughts

The recipe for generating higher nominal wages growth and inflation is quite simple – have fiscal and monetary policy working in tandem to stimulate economic activity and job creation whilst growth in the labour market is somewhat contained. This does not mean that the international borders need to remain closed or that firms cannot hire from a global pool of labour. But it does mean that the targeted level of immigration in the economy will need to be recalibrated when the international borders are reopened if wages growth is to make a more permanent lift to around 3% per annum.

Ultimately the outcomes we get will reflect the priorities of policymakers. If full employment and a meaningful and sustainable lift in nominal wages growth is the combined priority of both the RBA and the Commonwealth Government then we believe it will be achieved by late 2022 and sustained through 2023 as monetary policy is normalised.