By Gareth Aird, head of Australian economics at CBA

Key Points

- The domestic economic landscape has changed significantly as a result of COVID‑19; it means that we are much more likely to see a lift in wages growth and consumer inflation over the next few years.

- The Commonwealth fiscal stance has shifted radically in favour of a sustained lift in expenditure and by extension big deficits which will boost demand in the economy.

- Growth in labour market supply has slowed dramatically because of the sudden drop in net overseas migration.

- Households are sitting on an incredible war chest of savings that have been accumulated over the past year.

- The RBA’s reaction function has changed which means they will be deliberately late to tighten monetary policy.

- We expect wages growth to accelerate to 2.7%/yr by end‑2022.

Overview

Economists are generally reluctant to utter the phrase ‘this time is different’ because too often it turns out to be the case that things weren’t dissimilar after all. However, when things change in ways which make the current or future environment noticeably different from the past it is the appropriate statement to make. I believe we are at that point now in Australia when thinking about the outlook for wages and inflation.

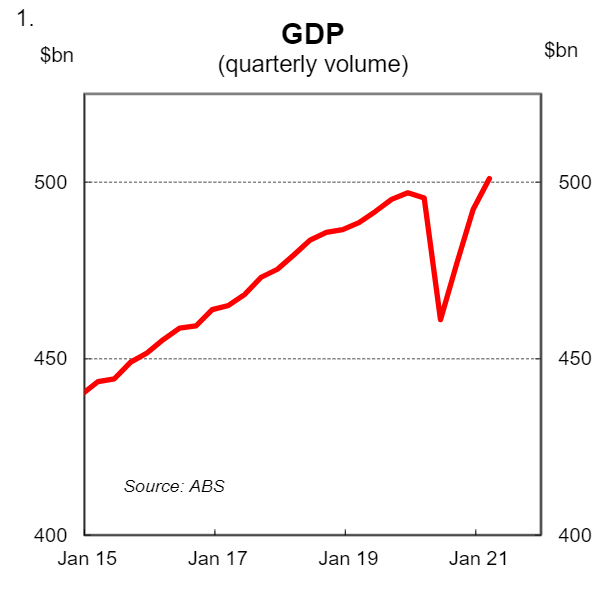

Regular readers will know that CBA was early to arrive at the conclusion that the Australian economic rebound would be strong and swift. We took that view because the policy response was very different to that of previous big negative economic shocks. More specifically, the fiscal and monetary policy stimulus injected into the economy was unprecedented in both size and scale. And crucially it was immediate. So taking the approach of ‘this time is different’ was very much the correct mindset to have when forecasting the COVID-19 economic rebound, which we now know was V-shaped (chart 1).

The notion that ‘this time is different’ is still very much applicable to the economic outlook over the next few years. A number of factors have shifted, in some cases radically, relative to pre-COVID which means we are far more likely to see wages growth and inflation lift. The RBA appears quite convinced that wages growth will remain weak and by extension inflation will remain low. But their conviction is largely based on low wage and inflation outcomes being the dominant theme prior to the pandemic when the economic backdrop was very different.

This note discusses four developments that have altered the economic landscape materially.

(i) The fiscal stance is very different

Updates on the Government’s fiscal position were keenly watched in 2020 because Australia was in the midst of a massive negative economic shock that required an extraordinary fiscal response. The October 2020 Budget in particular captured the expected impact of the shock and policy response to it on the Government’s fiscal position. But in many respects the May 2021 Budget will go down as the watershed moment rather than policy decisions that were essential to support the economy in 2020.

The 2021 Budget heralded a radical shift in ideology from a Coalition Government that had previously been fixated on achieving a balanced budget. Indeed the rhetoric around ‘debt and deficit’ and the need for fiscal restraint has been replaced by a stated objective to, “drive the unemployment rate down to where it was prior to the pandemic and then even lower”.

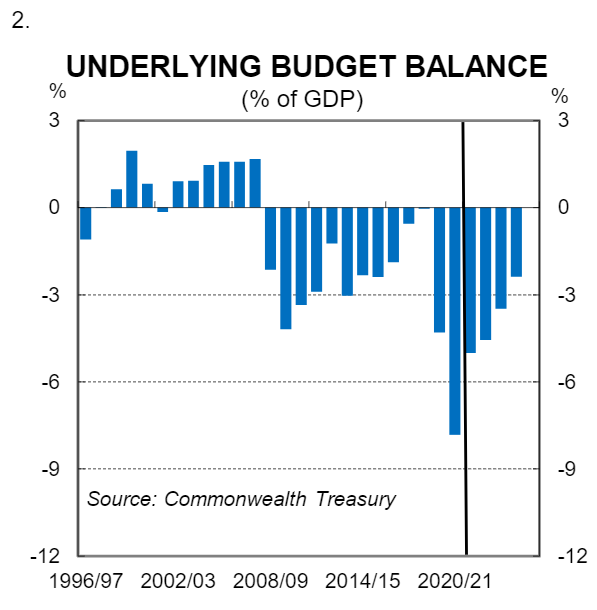

In summary the Government will now play a much more active role in demand management in the economy compared to pre-COVID. This means a lot more spending and big deficits (chart 2).

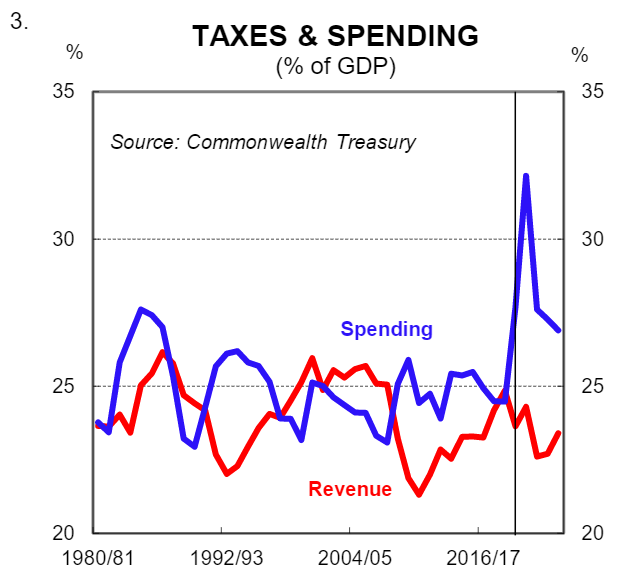

Expenditure is forecast to average 27.0% as a share of GDP between 2021/22 and 2024/25. By comparison expenditure averaged 24.8% as a share of GDP in the four years prior to the pandemic. An increase in expenditure of 2% per year on average as a share of GDP is massive (chart 3).

The Government’s aim is to use the fiscal levers to run the economy hot which will push the unemployment rate down. This will ultimately help the RBA to achieve its objective of full employment and to meet its inflation target. It means that both fiscal and monetary policy will be pulling in the same direction which has not always been the case (fiscal policy and monetary policy were working in opposite directions over the seven year period prior to the pandemic).

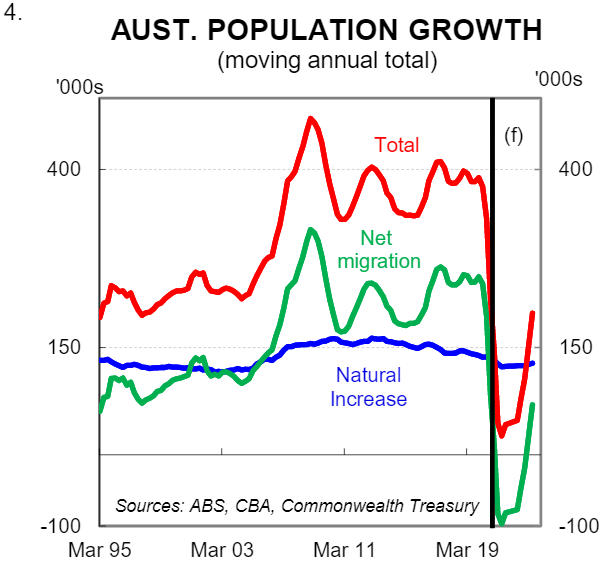

(ii) Labour market supply has slowed dramatically and the NAIRU is higher

Labour market supply is constrained because the international borders are closed. This means that as the labour market tightens, labour shortages will manifest themselves because employees are not able to hire from abroad as was previously the case. As a result, employees in many industries have had a lift in their bargaining power that is independent of the level of slack in the local labour market. Essentially talent is scarce because firms can’t hire from a global pool of labour. This raises the non-accelerating inflation rate of unemployment (or NAIRU) as we have previously covered.

The Government expects the international borders to remain largely closed until mid-2022 which will weigh heavily on net overseas immigration (chart 4). As a result, growth in labour supply will be very low at a time when economic momentum is strong and job vacancies are at very elevated levels.

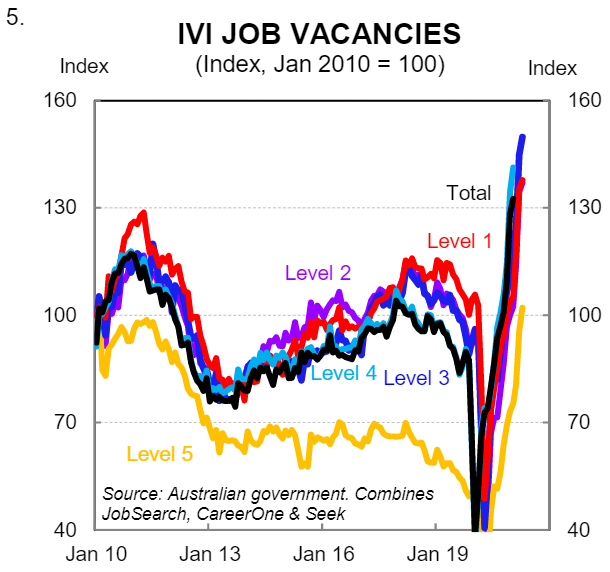

The evidence indicates that the sharp drop in net overseas migration has already had a profound impact on the labour supply and demand equation. Labour shortages have emerged across a whole range of industries, states and skill levels (chart 5). This will see turnover in the labour market increase as workers change jobs for higher pay. It will also make it easier for employees to negotiate higher pay with their current employer. These dynamics are very different to pre-COVID-19 when growth in labour market supply was strong due to the high level of net overseas immigration.

(iii) Households have accumulated a war chest of savings

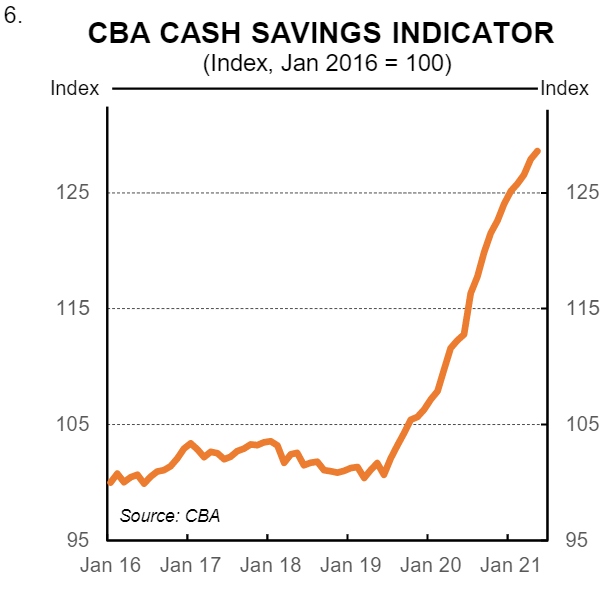

One of the remarkable stories over the COVID-19 period has been around the big lift in household income and the surge in the stock of savings. We have been able to track these dynamics in real time by looking at payments going into CBA bank accounts and changes in the level of household deposits (chart 6).

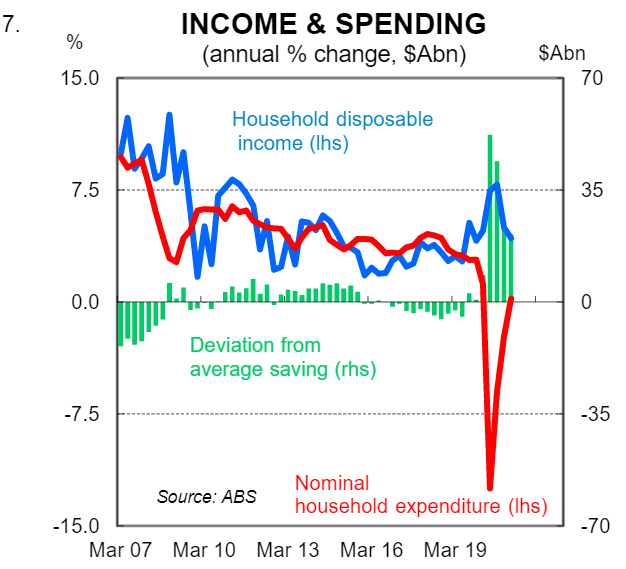

The stock of savings has continued to swell in 2021. Based on the Q1 21 national accounts we estimate that $A140bn was saved over the past year (over and above what is normally saved given the household sector is a net saver–chart 7). This means that the Australian household sector is sitting on accumulated additional savings of around 7% of GDP. These savings exclude the early withdrawal of superannuation and are calculated as the difference between income and expenditure less ‘normal savings’.

The unprecedented accumulation of savings is an upside risk to consumption and inflation over the next two years. Households did not ‘choose’ to save this money over the past year and therefore it is reasonable to assume that a decent chunk of savings are spent. A partial drawdown of savings will see the demand for certain goods and services lift more quickly than usual. As this happens we will see some demand pull inflation. That is, some businesses will lift the prices of the goods and services they are selling in response to higher demand. There is evidence that inflation is already moving higher. The Market PMIs, for example, indicate that growth in output prices has stepped up (chart 8).

(iv) The RBA’s reaction function has changed

In October last year RBA Governor Philip Lowe delivered a landmark speech that indicated the RBA had shifted its reaction function. More specifically, the Governor stated that the RBA had changed tact to put a greater weight on actual, not forecast, inflation in their decision-making.

The Governor said that, “the Board will not be increasing the cash rate until actual inflation is sustainably within the target range. It is not enough for inflation to be forecast to be in the target range”.

This shift in reaction function means that the RBA intends to be deliberately behind the curve with regards to monetary policy tightening, particularly as it pertains to the cash rate.

In essence the RBA will rely on lagging indicators in the form of wages data and the CPI to determine when they will raise the cash rate. This means two things:

(i) we are more likely to see higher wages and inflation outcomes because the RBA will not pre-emptively lift the cash rate in a bid to fend off higher wages and inflation; and

(ii) there is a risk that the RBA is too late in tightening policy and may need to go harder and faster if inflation and inflation expectations have lifted beyond the desired level. At this stage we consider that risk to be low. But it could materialise, particularly if fiscal policy was to remain very expansionary while the economy was running at full capacity.

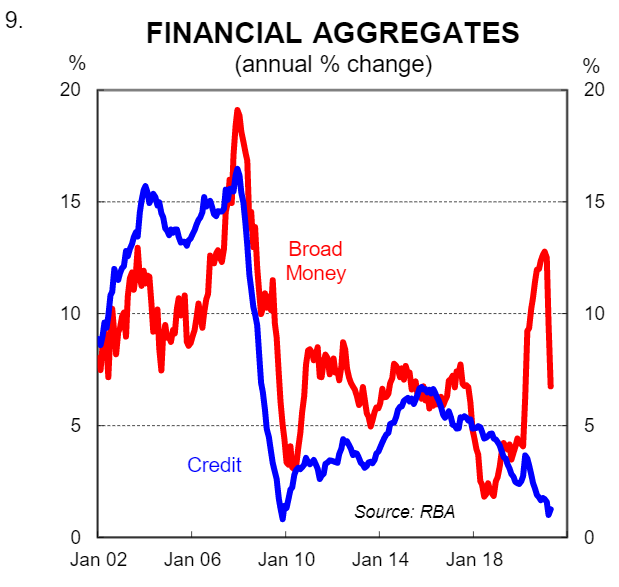

Finally it’s worth keeping in mind that the RBA’s quantitative easing program has led to a rapid acceleration in the money supply (chart 9). The relationship between consumer inflation and the money supply is somewhat vexed. But a large expansion of the money supply simply increases the risk of higher inflation over time.