Forex last night was a reflection of weakening US data, fading inflation and diving commodities. DXY was firm as was EUR:

Australian dollar was hit on all major DM crosses:

Oil is to the moon on strong US inventory draws. Gold is caput:

Base metals were hammered:

Big miners too:

EMs stocks were hit:

Junk eased:

US yields were bid:

But stocks came off anyway:

Westpac has the data wrap:

Event Wrap

US retail sales in May were weaker than expected, falling 1.3%m/m (est. -0.7%m/m), although April was revised higher to +0.9%m/m from flat. The core measure – control sales – fell 0.7%m/m (est. -0.5%m/m), with April revised from -1.5%m/m to -0.4%m/m.

Industrial production in May rose 0.8%m/m (est. +0.7%m/m), but April was revised lower to +0.1%m/m from +0.7%m/m. Capacity utilisation rose to 75.2% (est. 75.1%) from a downwardly revised 74.6% in April (initial 74.9%).

PPI inflation in May rose 0.8% (est. +0.5%m/m), with most gains from goods (+1.5%m/m). The +6.6%y/y headline rise is the largest since Nov. 2010. The ex-food and energy measure rose 0.7%m/m (est. +0.5%m/m).

The NY/Empire Fed manufacturing activity survey fell to 17.4 (est. 22.7, prior 24.3), with components mixed. NAHB homebuilder confidence fell to a still strong 81 (vs. est. unchanged at 83), citing concerns of “higher costs and declining availability for softwood lumber and other building materials”.

Eurozone trade surplus was narrower in April at EUR9.4bn (est. EUR15.0bn), but from an upwardly revised EUR18.3bn (initially EUR13.0bn).

UK employment was firm. April unemployment fell to 4.7% (from 4.8%), as was expected, and although the 3m/3m employment change of 113k was below estimates of 135k, May jobless claims fell -92.6K from a revised -55.8k (initially -15.1k) in April.

Event Outlook

Australia: The May Westpac-MI Leading Index is likely to see a further slowdown with several components recording pull-backs in the month, with the latest Vic lockdown delivering a shock to consumer sentiment and a notable pull back in dwelling approvals (-8.6% vs 18.9% last month). Against this, the Index growth rate will continue to get some offsetting support from a rising sharemarket and buoyant commodity prices (up 5.8% in AUD terms).

New Zealand: We expect the annual current account deficit to widen to 2.1% of GDP in the March quarter, after having narrowed to a 19-year low of 0.8% late last year. The main factor is the lack of the usual lift in overseas visitor spending at this time of year. This will see the deficit widen further over the rest of 2021, with the border not fully opening until next year.

China: May retail sales (market f/c: 26.3%yr ytd), industrial production (market f/c: 18.0%yr ytd), and fixed asset investment (market f/c: 17.0%yr ytd) should reveal strong consumer spending, whilst production and incomes are buoyed by domestic and external demand.

US: May housing starts are expected to advance 5.2%, while building permits should ease off 0.2%; going forward, elevated lumber costs pose a risk to the outlook for homebuilding activity. The May import price index is set to rise 0.7% on strength in energy import prices. The June FOMC meeting will be interesting for a number of reasons. First up, after the meeting, the Committee’s revised forecasts will be provided, guiding on their central expectations for the coming three years. Second, Chair Powell’s press conference will give a good guide on the degree of confidence the Committee has in their central projection for both inflation and the labour market — the FOMC’s two core concerns. Third, for these two aspects of the economy, an assessment of the risks will be provided. This will help guide on how great an impact key risks are likely to have on the outlook for policy, should they eventuate.

As Goldman Sachs so nicely described a few weeks ago when arguing that China no longer mattered to commodity prices, the headwaters of metals demand are today in DM stimulus. Well, that stimulus is fading fast as the US fiscal cliff looms.

Of course, the argument is rubbish. All that matters to commodity prices is Chinese demand and it is about to fall considerably as credit is radically tightens. What matters now is how fast the US slows alongside China. If the two converge then the commodity price bubble burst we are seeing begin will quickly morph into an outright growth scare that drags in EM debt and equities.

The jury is still out on that. For now, let us recognise that easing US demand will aid in the unwind of the global inventory supercycle and its supply-side price frictions. In turn, falling inflation (and demand) will pop the Wall Street commodities bubble. Today we see big falls in lumber, softs, increasingly base metals most notably copper and other markets.

This is just the beginning in my view. Bulks are next as China joins the US slowdown, particularly in its construction sectors.

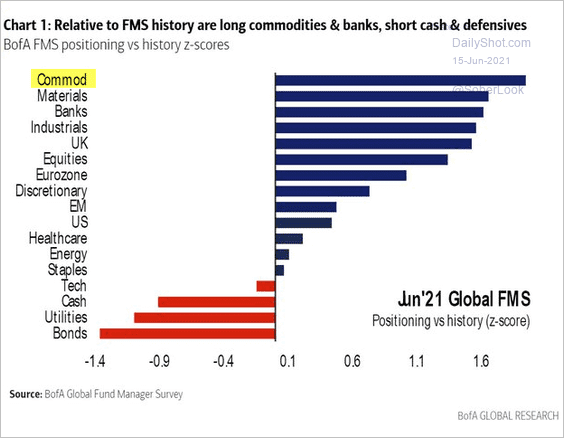

Two factoids stood out last night in the BofA monthly fundie survey that matter to this. First, three-quarters of fundies agree that inflation is temporary:

Yet nearly all of them are overweight inflation trades, especially dirt:

In short, the coming reversal on the inflation and commodities trade looms as violent with the crown jamming the exit all at once.

Which makes me more bearish Australian dollar.