Forex is still range trading as we await tomorrow’s inflation numbers. But bond markets have already made their call. Yields have broken down as markets sell the inflation fact and buy into the MB script. DXY was firm as EUR eased:

Australian dollar fell against everything:

Gold may be rolling. Oil ain’t!

Base metals have lost momentum:

Big miners as well:

And EM stocks:

Junk remains serene!

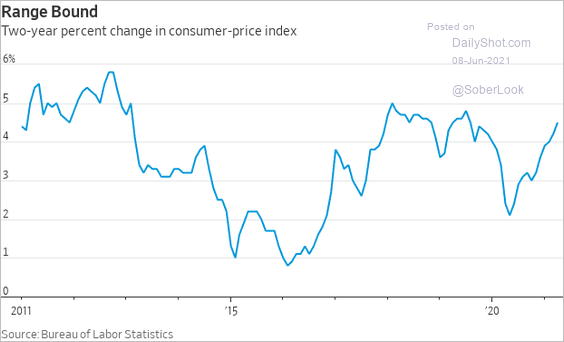

It’s goodbye to inflation and all that:

Which could not rouse stocks, oddly. Not a great sign for risk and raises the specter of a growth shock:

Westpac has the data wrap:

Event Wrap

US final April wholesale inventories were left unchanged from the initial release at +0.8%m/m.

Bank of Canada maintained the 0.25% policy setting and maintained its QE programme at $3bn per week, matching expectations. Developments have evolved broadly as was expected in April. The rise in core inflation was attributed to temporary factors and base-year effects, CPI seen rising 3% through the summer but easing later in the year. BoC continued to judge that the economy has “considerable excess capacity and the recovery continues to require extraordinary monetary policy support”, and repeated that: “We remain committed to holding the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved. In the Bank’s April projection, this happens sometime in the second half of 2022.”

Germany’s April trade surplus was slightly lower than expected at +EUR15.5bn (est. +EUR16.3bn).

Bank of England Chief Economist Haldane raised his concerns over the risks of higher inflation resulting from current monetary policy settings, and also suggested that the UK economy could move from recovery to boom as support measures gain traction.

Event Outlook

Australia: MI inflation expectations edged up in May, but still remain below pre-covid levels ahead of the June update.

New Zealand: We’re forecasting a 0.1% rise in May retail card spending. Looking through the swings in spending associated with changes in the Alert Level, the trend in spending has been flattening off. A key reason for this is the slowdown in population growth since the borders were closed. There has also been a change in the composition of spending. Since the outbreak of Covid, spending on durable items like household furnishings has been strong. That’s helped to offset the drag from reduced spending in the hospitality sector.

Euro Area: At its upcoming policy meeting, the ECB’s Governing Council will be cautious not to impede the recovery before it is in full swing. The Bank is likely to keep Pandemic Emergency Purchase Program (PEPP) buying elevated over the next quarter, possibly at the “significantly higher” pace of around EUR 18bn/week. Any talk of tapering is set to be delayed until later in the year, when the rebound has materialised.

US: We (and the market) are looking for a 0.4% rise in the May CPI, a release that will be closely watched by markets. However, in coming months, we expect these price pressures to dissipate. Initial jobless claims should continue their downtrend in the week ended 5 June, with the market anticipating a further fall to 370k.

So, with US yields crashing suddenly, where’d all of that inflation go? The first reason is that there actually isn’t any inflation if you look through the pandemic distortions:

The rest of it is all inventory supercycle and commodity bubble. Both of which are temporary and going to fall away dramatically soon.

In fact, yesterday’s China PPI, which came in at an astonishing 9% inflation, is probably going to print a similar number again next May, but in the negative as iron ore and steel prices crash.

As this transpires I expect AUD to weaken.