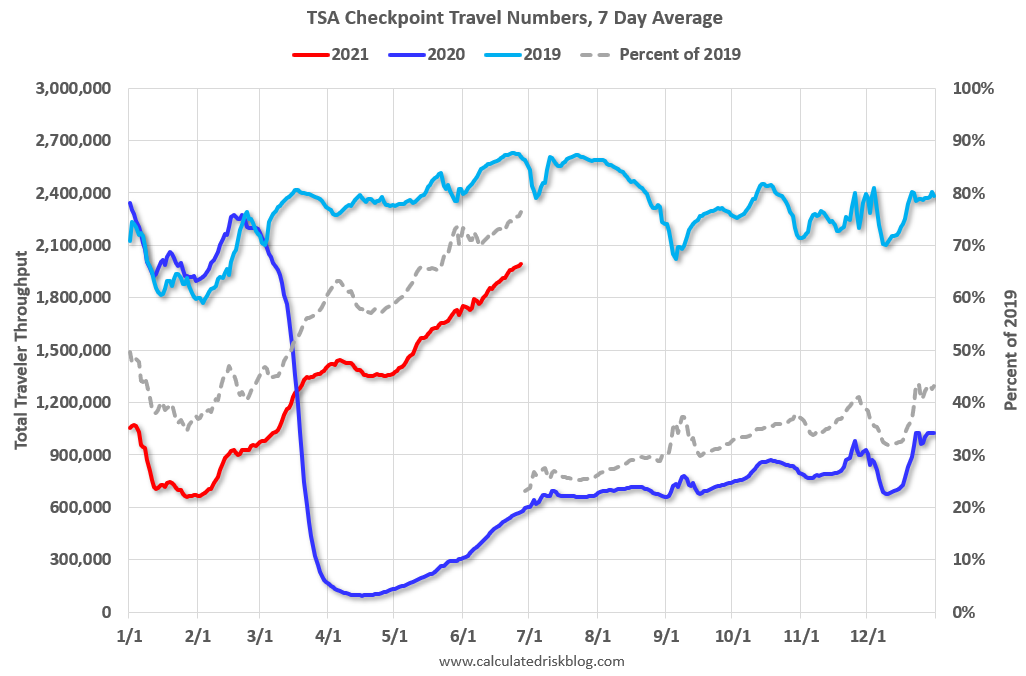

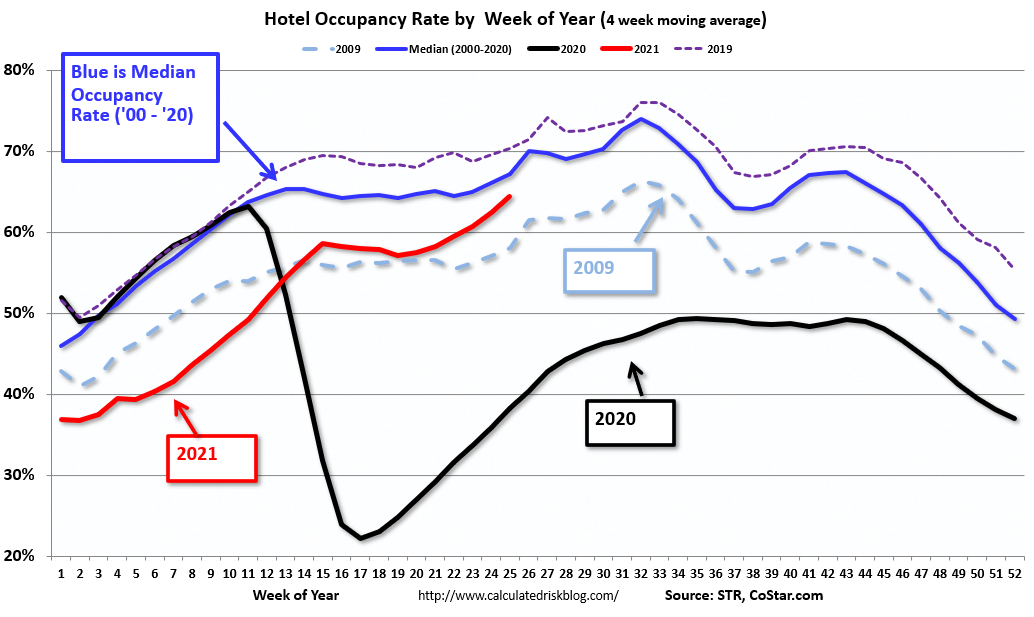

Schadenfreude is a bitch. As 12m Aussies cower under the doona, watching TV punctuated by The Idiot’s ‘travel Australia’ advertisements paid for those under house arrest, Americans are traveling in droves:

On the current trend, American travel will be back at full volume during Q3.

It won’t stop there, either. Massive savings are set to carpet bomb long-neglected services, via BofA:

Advertisement

There has been a very large surge in savings in the past 15 months. We think there are three ways to measure the surge. The first is to identify specific government outlays that were likely mainly saved such as stimulus checks to healthy households. This approach comes up with some small numbers—less than a trillion dollars in wind fall savings. We think this is the wrong approach: we need to look not only at direct deposits, but the indirect impact of stimulus dollars flooding the economy and at the fact that spending on services was constrained. Thus a second approach is to compare actual savings each month relative to the normal 8% or so rate before the crisis (Exhibit 1).

By this metric, as of May there is about $2.3tr in excess savings. What is striking about this chart is that not only have there been surges in saving with the introduction of new stimulus packages, but savings have remained unusually high between packages. For example, in May—even services opening up and with the March stimulus fading—the saving rate was 12.4%. Clearly spending will likely need to increase further just to stop the excess saving.

However, we favor a third measure—the excess funds piling up in bank accounts. This metric compares actual M2 (checking, savings, money market funds etc.) to the trend inM2 (Exhibit 2). As of May there was $3.5tr in excess M2 with the vast majority held by households. Why focus on this gauge? We think it shows how households are viewing the accumulated savings. They are simply leaving the money in the bank rather than redeploy the funds into a more illiquid form of savings. In our view they are“saving for a sunny day,”keeping money handy to spend as the economy reopens.

Consumer surveys put travel right at the top of the next wave of this spending given huge pent-up demand. I know I sure as shit want to get out of Hellbourne.

MB Fund still holds a large position in travel stocks. They’ve been decent so far but have ebbed and flowed with the virus. We’re sticking with them because we reckon one day pretty soon we’ll wake up and find that they’ve doubled overnight.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.