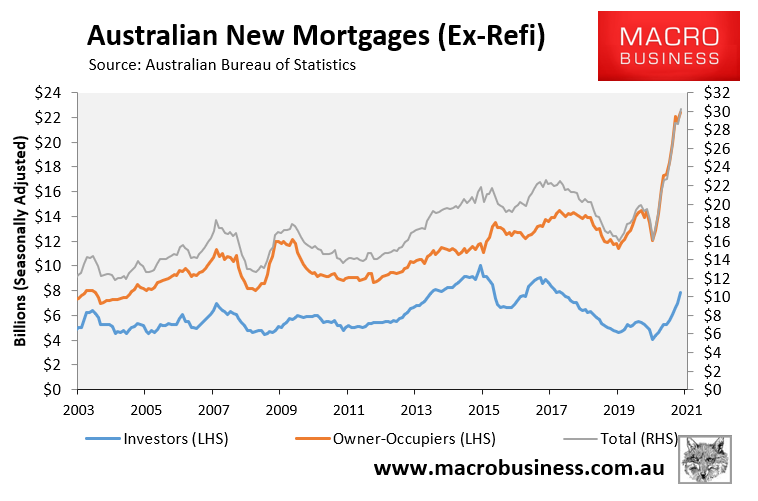

As we know, the Australian Bureau of Statistics’ (ABS) latest lending data reported the biggest ever boom in mortgage finance commitments, up a whopping 55% in the year to March 2021:

Australia’s biggest ever mortgage boom.

Amid the mortgage frenzy, there are increasing signs that lenders are dropping lending standards. The latest example came yesterday when NAB owned U-Bank announced that it is offering cheap 15% deposit home loans without borrowers needing lenders mortgage insurance:

UBank chief executive Philippa Watson said reducing the threshold would shave off roughly seven months of saving for home buyers…

“By only requiring a 15 per cent deposit and waiving the need for lender’s mortgage insurance, UBank can help shave nearly seven months off the process”…

Ms Watson said a reduced deposit could mean a homebuyer could be able to buy a property at a cheaper price than in six months, as prices continue to rise.

UBank will offer loans with a loan-to-value ratio between 80 and 85 per cent with a variable interest rate of 2.49 per cent, or a three-year fixed rate at 2.05 per cent.

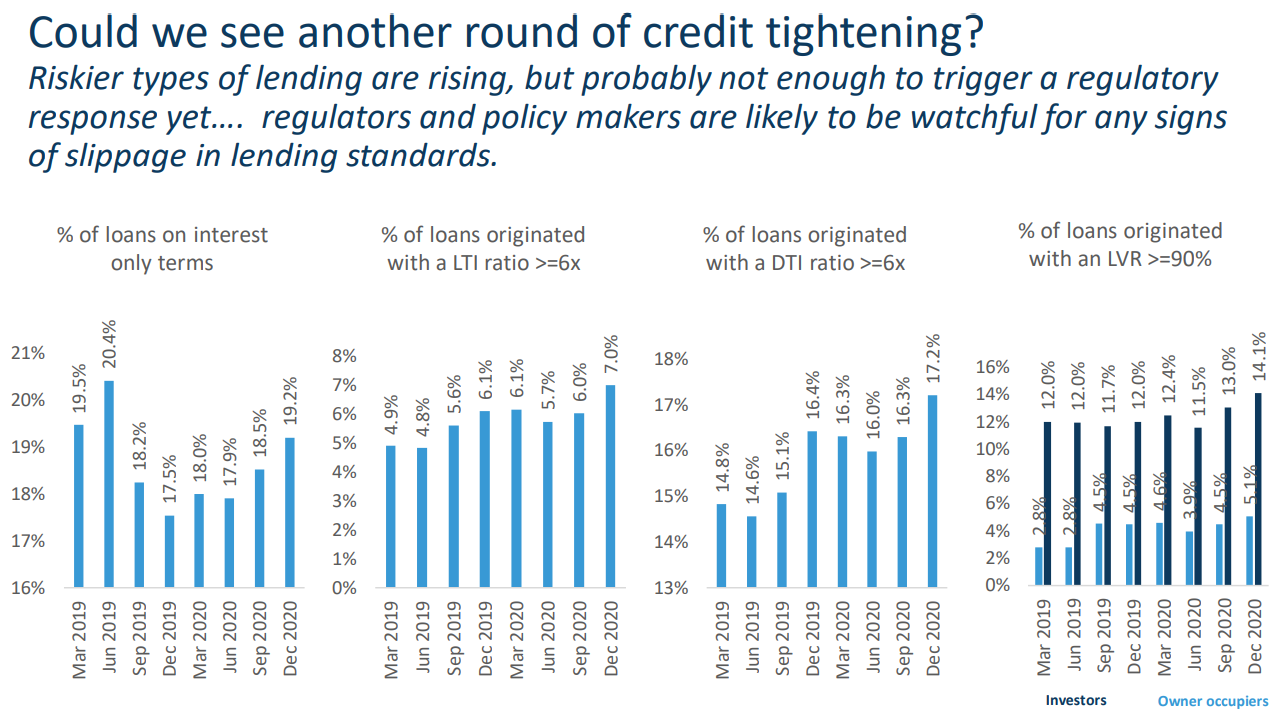

CoreLogic’s latest Monthly chart pack also showed a marked deterioration in lending standards in the final quarter of 2020 – something that has likely worsened since:

Mortgage lending standards clearly deteriorated at the end of 2020.

The federal government has also gotten in on the act, flagging that it will offer more low-deposit mortgages in tonight’s budget, namely:

- A government-guaranteed home loan scheme will be offered to more than 125,000 single parents, which will allow them to purchase a home with as little as 2%.

- An extra 20,000 places will be offered under the existing first home loan deposit scheme, which allows people to acquire a mortgage with only a 5% deposit, with risk underwritten by taxpayers.

It is amazing to think that we are only 25 months past the final report of the Hayne Banking Royal Commission, which documented widespread irresponsible lending.

The lessons of the royal commission have clearly been forgotten with sub-prime mortgage lending swinging back into vogue.