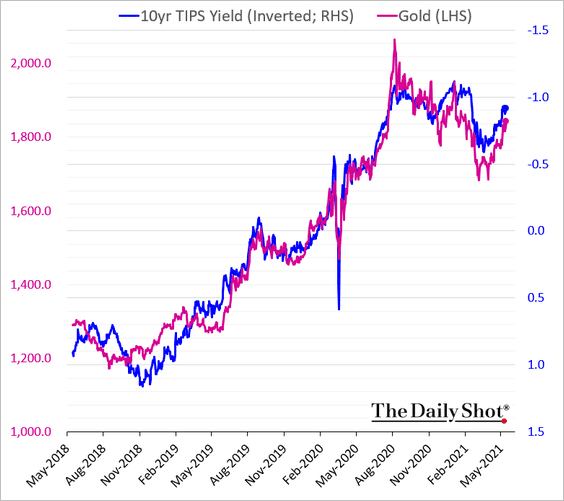

Gold has rebounded strongly in recent weeks as the generalised inflation panic has built up a head of steam. It has been particularly helped by the peculiar combination of high US inflation and a weakening DXY, trigger by the recent US jobs report which hinted at stagflation.

This has led to a slump in real interest rates and driven gold back up:

Goldman has more on the dynamic:

Advertisement