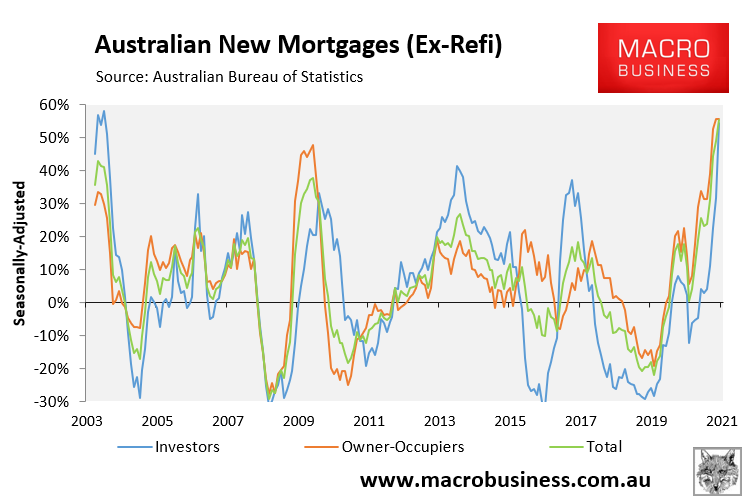

Yesterday, the Australian Bureau of Statistics (ABS) released data on new finance commitments, which showed booming growth in both owner-occupied and investor mortgages.

As shown in the next chart, owner-occupied mortgage commitments rose 55.6% in the year to March 2021, whereas investor mortgage commitments rose 54.3%:

Annual growth in both owner-occupied and investor mortgages is running at historical highs.

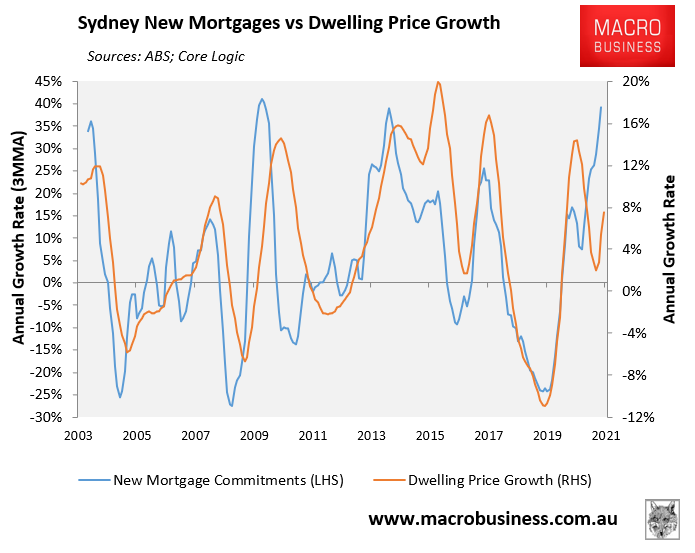

As regular readers know, the growth in new mortgage commitments has historically correlated very strongly with dwelling value growth. The reason is straightforward: the overwhelming majority of buyers borrow to purchase a home. Thus, when mortgage demand rises, so do property prices.

Below are a series of charts tracking the annual growth of new mortgage commitments by value against annual dwelling value growth across the five main capital city markets.

Sydney:

Sydney’s trend mortgage commitments grew by 39% in the year to March 2021, which is similar to prior peaks. Not surprisingly, Sydney dwelling values are also growing strongly, rising by 8.8% over the April quarter:

Sydney’s mortgage boom signals strong property price growth.

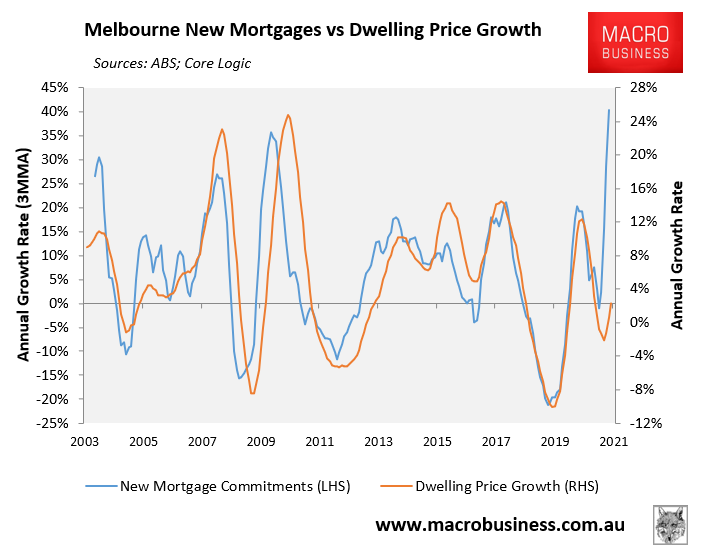

Melbourne:

Melbourne’s trend mortgage commitments rose 40% in the year to March, which is above prior peaks. Price growth was also strong at 5.8% over the April quarter:

Melbourne’s mortgage demand is now running above prior peaks.

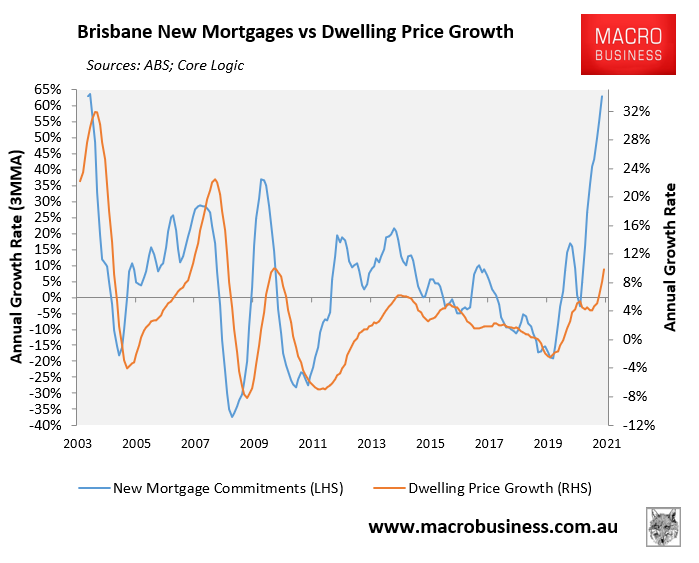

Brisbane:

The growth in Brisbane mortgage commitments is running close to the 2003 peak at 63%. Brisbane dwelling values are also booming, up 5.6% over the April quarter and 8.3% year-on-year:

Brisbane’s mortgage demand is running near an all-time high.

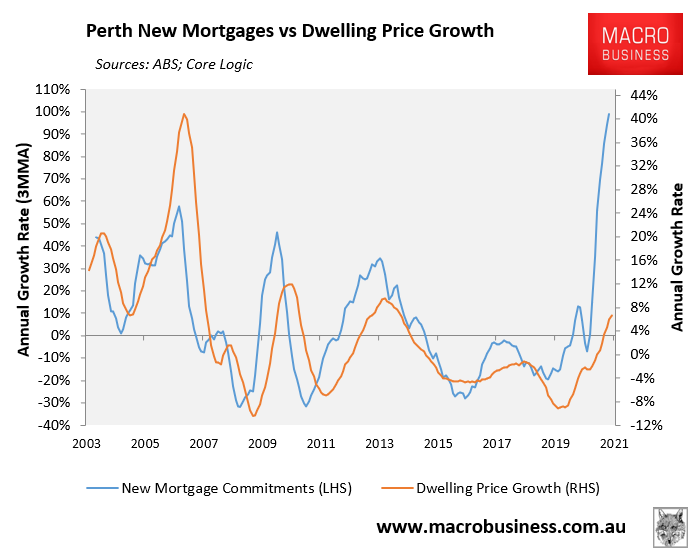

Perth:

Perth’s mortgage commitments are experiencing their biggest ever boom, up 99% in trend terms in the year to March. Dwelling values are also rising fast, up 4.2% over the April quarter:

Perth mortgage demand has never been stronger.

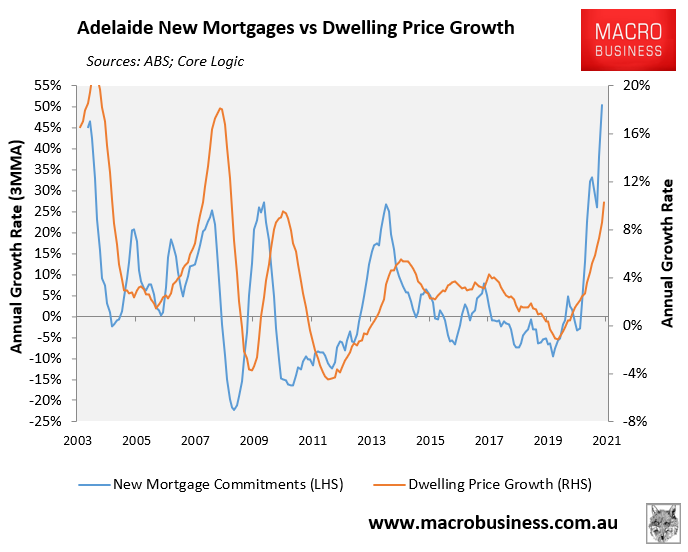

Adelaide:

Adelaide’s mortgage demand is blowing the roof off, up 50% year-on-year in March in trend terms. Dwelling value growth is also strong at 4.3% over the April quarter and 10.3% year-on-year:

Adelaide’s mortgage demand is blowing the roof off.

In summary, the coast-to-coast boom in Australian property values is reflected in mortgage growth, which is running at or above historical highs across every major market.

Once mortgage demand starts to wane, so will property price growth.