RBA Governor Phil Lowe last year endorsed Treasurer Josh Frydenberg’s proposal to axe responsible lending rules, telling the Standing Committee on Economics that Australian mortgage restrictions had become too strict and were constraining the economy:

“We can’t have a world in which, if a borrower can’t repay the loan, it’s always the bank’s fault. On a portfolio basis, we want banks to make some loans that actually go bad, because if a bank never makes a loan that goes bad it means it’s not extending enough credit”…

“The pendulum has probably swung a bit too far to blaming the bank if a loan goes bad”…

Lowe went on to say that the way the responsible lending legislation had been interpreted needed looking at:

“If we can’t do that properly, maybe we need to look at the legislation”.

Later in October, Lowe reiterated this view, stating that the removal of responsible lending rules “would support the supply of credit”.

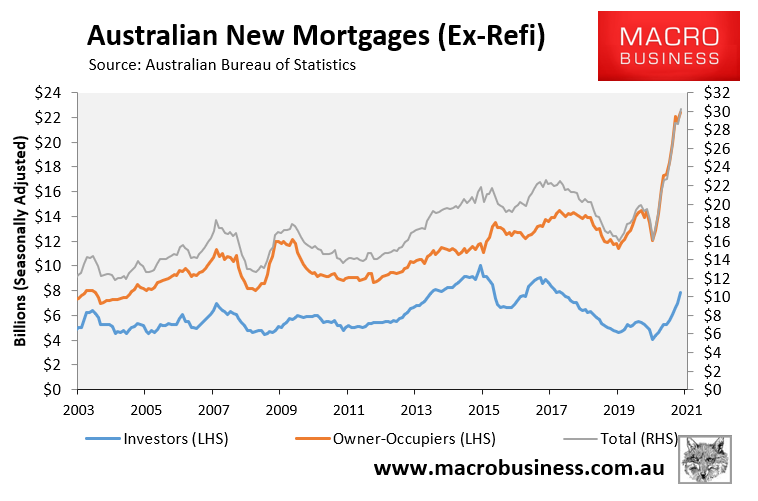

Since these infamous claims, the notion that the supply of credit is constrained has been completely obliterated by the ABS’ lending data, which has reported the biggest ever boom in mortgage commitments:

Australia’s biggest ever mortgage boom.

Mortgage brokers and banks are also run off their feet:

The nation’s banks are struggling to process an unprecedented number of new mortgages…

ANZ chief executive Shayne Elliott revealed his bank had wound back home loan marketing because demand was so strong while mortgage brokers said they were flat out…

Mr Elliott said his bank was struggling because of the “extraordinary” level of demand for housing over the past six months… “The volumes are unprecedented. We have not seen sustained high volumes like this ever before. When we built our machines, it was never imagined we would have to cope with these kinds of volumes every day of the week”…

“Brokers are flat out at the moment. Brokers have never been busier,” [Peter White, Finance Brokers Association of Australia managing director] said.

This doesn’t sound like an economy suffering from constrained credit, does it?

Of all Phil Lowe’s calls, his endorsement of Josh Frydenberg’s planned abolition of responsible lending rules must rank among the worst.