Nordea with the note:

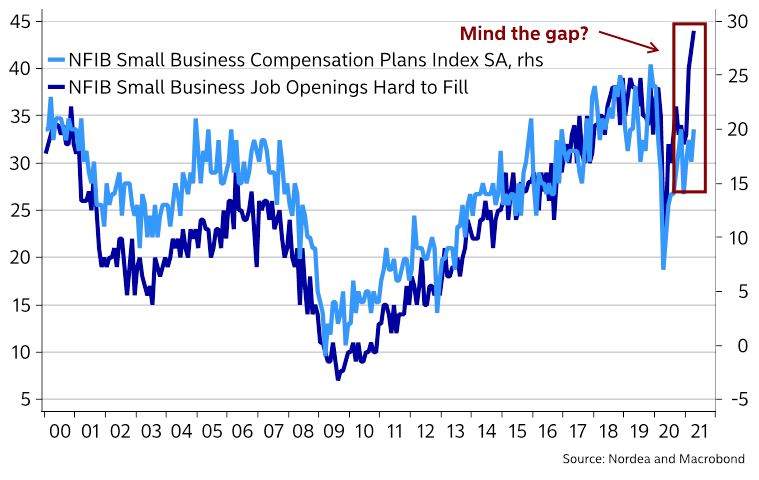

Only Elon Musk disappointed more than the job report over the weekend (watch the price action in Dog(e)coin, in case you are curious), but some odds effects may be in play currently. Jobs openings are plentiful, but they are just hard to fill due to 1) mobility issues, 2) Covid-fears and 3) direct transfers and benefits providing a better alternative. Maybe the fast-food chains need to increase the sign-on bonuses even more than what we have already seen? Wage growth is coming oddly fast given the unemployment level. Time to resurrect the good old Phillips curve.