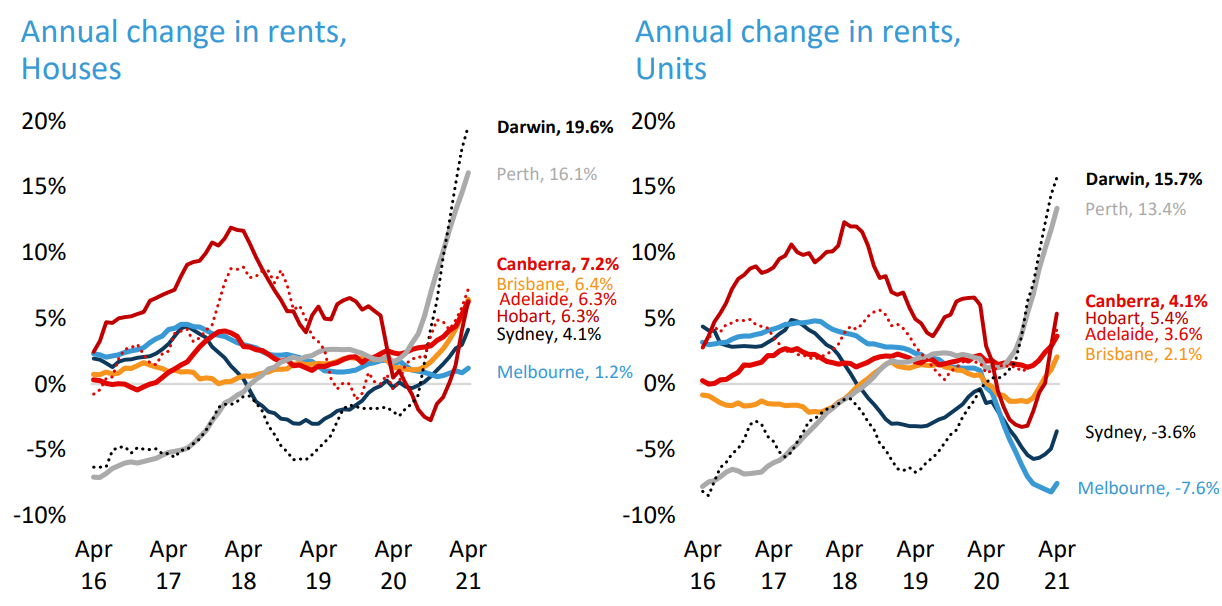

CoreLogic’s April housing market update shows that Australia’s rental market remains two-speed, with the smaller capital city markets recording strong rental growth, while Sydney and Melbourne flounder.

As shown in the next chart, Darwin and Perth’s rental markets are booming, catching up on years of falls leading up to COVID. Across both houses and apartments rents have risen at a record annual pace of between 13% and 20%.

Rental growth remains two-speed, generally strong outside of Melbourne and Sydney.