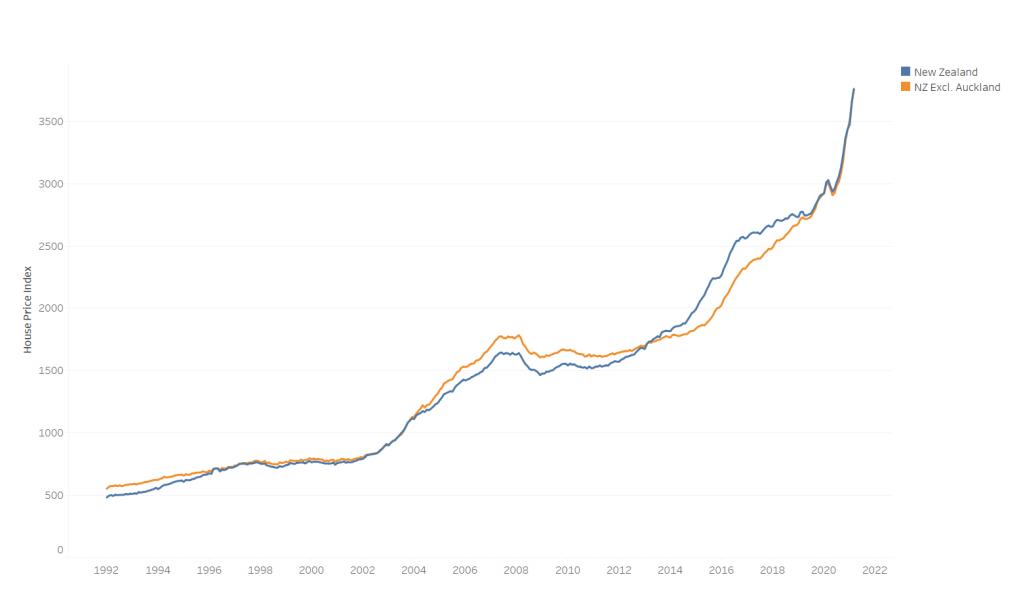

New evidence has emerged showing that the Reserve Bank of New Zealand (RBNZ) played a direct role in inflating New Zealand’s property market, which has experienced its strongest price growth in decades.

New Zealand property prices have gone vertical.

In April 2020, the RBNZ removed loan-to-value (LVR) mortgage restrictions to stimulate the economy amid COVID-19 lockdowns, which in the words of the RBNZ was followed with “a rapid acceleration in the housing market, with new records being set for the national median price, and new mortgage lending continuing at a strong pace”.