It’s beginning to play out as expected. Chinese headline growth for April was absolutely fine with year-to-date numbers still wildly distorted but falling back to earth roughly in line with expectations. Industrial production was 9.8%, retail sales 17.7% and fixed asset investment at 19.9% from last year’s depressed levels:

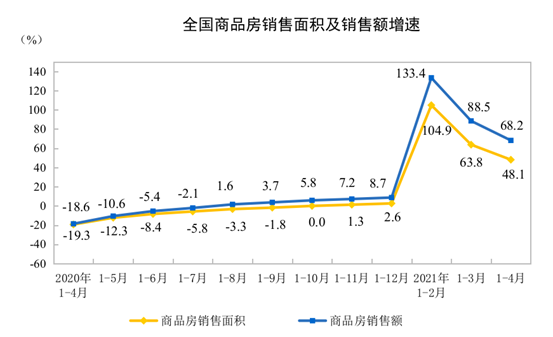

At first glance, even construction sectors look good with real estate sales still wildly inflated from base effects:

Advertisement

But that’s where the good news ends. Floor area construction starts are down roughly 10% for the fourth month in a row from 2019 levels, let alone last year’s juiced numbers: