Ah yes, the wonder that is crypto. Decentralsised, disintermediated, democractic. A revolution. Ahem…yeh right. Via FTAlphaville:

Sooooo remember Tether? The last time we wrote about the “dollar-backed” stablecoin around these parts was back in February, after the New York District Attorney’s office decided to suspend the company — and sister crypto exchange Bitfinex — and fined them $18.5m in a settlement because of their “illegal activities” in the state.

That was, you might recall, on the basis that the companies had deceived the market by overstating their reserves, and by covering up approximately $850m in losses.

You might have thought all this would have some kind of negative impact on Tether — which is pegged to the dollar — or even the wider crypto market, given how much crypto trading is done via Tether. But no, don’t be silly this is CREEPTO!! Since the settlement in February, when Tether was worth a piddling $35bn, it’s actually increased its circulation by more than $20bn to about $58bn.

But what does this number actually mean? Yes, it represents the total value of these tokens that are washing about the cryptosphere, but what stands behind them? Tether used to claim all its tokens were backed one to-one by US dollars held in cash reserves, but in an April 2019 affadavit, its general counsel Stuart Hoegner revealed that in fact only 74 per cent of Tethers were backed by “cash and cash equivalents”, with the rest in a “less liquid form”.

Under the terms of its February settlement with the NYAG, Tether agreed that it would provide quarterly breakdowns of the assets backing its tokens. So, on Thursday it appeared to say it had done that, as proudly announced by Chief Technical Officer Paolo Ardoino on Twitter (though rather than referring to the NYAG he says it is the “#crypto community” that asked for it 🤔):

That link in the tweet takes you here, to a PDF demonstrating its unrivalled transparency, which is a whole . . . one page long. It doesn’t appear to have been audited but who cares, it’s not like trusting intermediaries is a problem for this community is it?

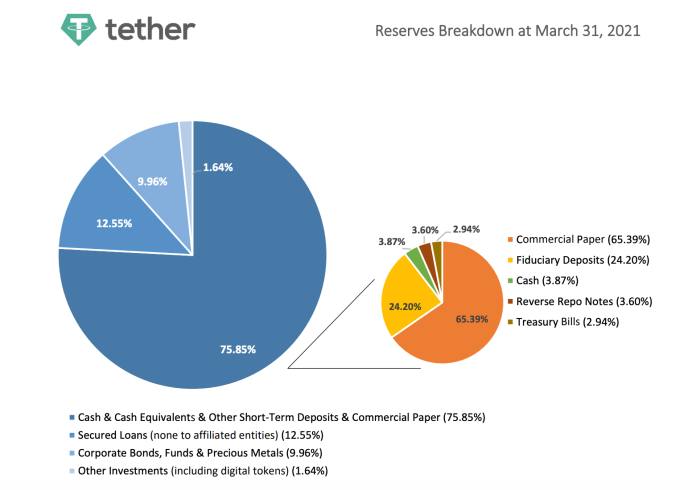

Here is the breakdown, as of March 31 2021 — it should be noted that this is the first time since launching in 2014 that Tether has actually released any kind of breakdown of its reserves, so to that extent yes, unrivalled indeed:

As you can see, the blue pie chart shows that 75.85 per cent of Tether’s reserves are, according to the company, backed by “Cash & Cash Equivalents & Other Short-Term Deposits & Commercial Paper”. The smaller, orangier pie chart breaks down that 75.85 per cent, and it turns out that the stablecoin that used to say it was 100 per cent backed by cash reserves is in fact . . . 2.9 per cent backed by cash reserves (3.87 per cent of the 75.85 per cent). Fancy that!

We asked the NYAG’s office whether this would satisfy their reporting requirements and they told us:

“We cannot confirm if this will suffice at this time.”

An interesting response. At this time.

The wildcat crypto bank

Before we move on to the rest of the breakdown, we asked some of our friends — well-known FUDsters, as our beloved crypto-enthusiast commenters will no doubt point out — what they made of the fact that only 2.9 per cent of Tether’s reserves were in cash?

Frances Coppola, financial commentator and operatic wonder, told us (emphasis ours here and throughout):

“Tether’s reserves analysis published today confirms what many people have said for a long time, namely that Tether has almost no cash dollars on its balance sheet. Actual “cash” is 3.87% of what Tether describes as “cash and cash equivalents, which in turn make up only 75% of its total assets. We know from the March attestation that nearly all of Tether’s liabilities consist of tokens it has issued. And we now know there are hardly any real dollars backing these tokens. We have come a long way since Tether claimed on its website that all USDT in existence were 100% backed by real US dollars.”

Yup. Indeed. It’s almost like Tether thinks it is some kind of bank, isn’t it?

Well, kind of. In the 2019 affadavit, Hoegner pointed out that commercial banks operate under a similar “fractional reserve” system, and that this was “hardly a novel concept”. But 2.9 per cent is really quite the fraction isn’t it? And the difference here, of course, is that commercial banks are subject to stringent regulations and thorough independent audits, neither of which apply to Tether.

When we asked Tether about this a couple of months ago, Hoegner told us that “Tether does not purport to be a bank, call itself a bank, or carry on a banking business”, and that “Tether Limited is registered as a money services business” and was regulated as such.

So it doesn’t purport to be a bank, but it points out that it operates a fractional reserve system like banks. Doesn’t that crypto-cake taste so damn good when you can have it and eat it all at the same time?

Martin Walker, director of banking and finance at the Centre For Evidence-Based Management, told us:

“It is pretty clear looking at the makeup of the reserves — a tiny proportion of the reserves are cash on account at banks — that Tether is operating like a bank but with none of the normal disclosure.

They are creating a dollar substitute and basically running a banking and payments business but without the oversight that anyone else doing a similar kind of business would have.

How the peg in value between Tether and the USD at exchanges is preserved is beyond any reasonable economic explanation. The resilience of the Tether dollar peg shows there is something rotten in the state of the whole crypto market.”

And Nicholas Weaver, a lecturer in computer science at the University of California, Berkeley, said:

“It’s clearly a wildcat bank. The cryptocurrency community seems intent on speed-running half a millennia of economic failure, and this is just simply one of the cases.”

Unknown credit risks

So what about the rest of the reserves? As you can see in the pie charts, the rest of the “cash and cash equivalents” are broken down as follows: commercial paper (65.39 per cent); fiduciary deposits (24.20 per cent); reverse repo notes (3.60 per cent); and Treasury bills (2.94 per cent).

Commercial paper, therefore, represents about half of Tether’s collateral. So which companies’ debt is it that Tether holds via this commercial paper, we hear you ask (we presume it is of the highest quality)?

Well they don’t tell us! On this Coppola said:

“The reserve analysis also shows that Tether’s assets are made up mainly of various forms of long and short-term corporate debt. We do not know if this debt is secured or unsecured, nor what the assets backing it are (if there are any). And we have no idea who the borrowers are, except that long-term loans are not made to Tether’s “affiliates”. The reserves are thus exposed to unknown levels of credit and liquidity risk.

I would have expected to see far higher levels of genuine cash equivalents such as T-bills and insured deposit accounts in a reserve report for a financial institution that claims to guarantee redemption at par. There is a very real possibility that in the event of a run on USDT, Tether would be unable to realise sufficient real USD to meet redemption requests. The 1:1 peg to the USD is therefore not remotely credible.”

If the numbers that Tether reports are accurate — which because they are unaudited we cannot be sure of — then it looks like just over 20 per cent of its reserves are made up of liquid, quality assets. That’s the 2.9 per cent of cash plus the fiduciary deposits, which make up about 18 per cent of the total reserves.

And the rest? Well as Walker says:

“It’s extremely difficult to make judgments about the liquidity or credit worthiness of the other assets making up the reserves because they simply haven’t disclosed sufficient information.”

We would be somewhat surprised if the NYAG is satisfied by this level of disclosure. Tether have given us some numbers, yes, but they are not audited, and they do not give us nearly enough information to be able to judge what would happen if a large number of people tried to redeem their Tethers for dollars at the same time.

STABLE Act

Over the coming months, Tether might find itself facing tougher scrutiny. In December, members of the US Congress presented a legislative proposal for the so-called “STABLE Act”, which would require stablecoins like Tether to obtain full banking licenses.

“The idea here is to build on the lessons that came out of the 2008 financial crisis, about how to regulate shadow banking and shadow finance,” Rohan Grey, assistant law professor at the Willamette University College of Law, who has been working on the new legislation with Congress, told us.

Grey continued:

“The idea that (stablecoins are) part of the business of banking, and should be regulated as such, is something that is increasingly being acknowledged across the spectrum.

The growing world of stablecoins arguably underpins the entire crypto community right now. If that collapses, the whole space could collapse.”

In short, BTC is a three times removed, parasitic financial instrument, that arbitrages the falling value of its own underlying collateral (fiat currency).

In the terms of recent financial disasters, it is a hyper-leveraged synthetic CDO that has considerably less reference to underlying collateral than did credit derivatives based upon sub-prime mortgage bonds. While also claiming AAA (gold) status.

Advertisement

It is nothing more than a giant shadow banking scam and should be shut down immediately.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.