More wild action on markets overnight as the COVID recovery lurches through another bubble and bust. This time in commodities. DXY was firm:

The Australian dollar remained weak, rallying out of new lows versus USD and slumping against EUR and JPY:

Oil fell hard, gold lifted a bit:

Base metals tanked:

As did big miners:

EMs stocks still look fooked:

Junk did a bit better:

As US yields eased:

Which cut stocks a break though tech underperformed again:

Westpac has the wrap:

Event Wrap

US PPI in April rose 0.6%m/m and 6.2%y/y (est. +0.3%m/m and 5.8%y/y), with the ex-food & energy measure up 0.7%m/m and 4.1%y/y (est. +0.4%m/m and +3.8%y/y). The BLS noted a record jump in the steel index (+18.4%), as well as notable gains in transport and warehousing on the services side. Weekly initial jobless claims rose 473k (est. 490k, prior 507k from initial 498k), continuing claims at 4.655m (est. 2.650m).

The FOMC’s Barkin said that the US recovery was outpacing the rest of the world, with “skyrocketing” consumer confidence and a “booming” housing sector. Countering these positives, Barkin mentioned the need to improve employment and long-term disinflationary forces that are curbing inflationary expectations. Waller said several more months of data will be needed before policymakers will be able to judge the economy’s progress on the employment and inflation goals. He wants to see at least the May and June jobs reports before thinking of tapering QE, expecting the Fed to maintain its accommodative stance for “some time.” He expects prices to rise over 2% this year and next but to return to goal in 2023.

Bank of Canada Governor Macklem said that its benchmark rate would not be changed until there was a complete economic recovery (“we’re about about 700,000 jobs below where we really should be”), even though it tapered its bond purchase programme at its April meeting.

Event Outlook

New Zealand: The April manufacturing PMI is likely to follow the global trend of robust manufacturing.

US: The headline April import price index will be supported by rising fuel costs and supply chain issues (market f/c: 0.6%). April retail sales have been surging on the reopening, the labour market recovery, and the stimulus (market f/c: 1.0%). Likewise, April industrial production is expected to advance 1.0%, with the manufacturing surveys reporting strong growth in output and new orders. Business inventories are likely to remain choppy throughout the year due to restocking and elevated turnover, and should rise 0.3% in March. May University of Michigan consumer sentiment is still below pre-COVID levels, but is beginning to accelerate (market f/c: 90.2). Finally, the FOMC’s Kaplan will take part in a moderated virtual discussion hosted by the University of Texas.

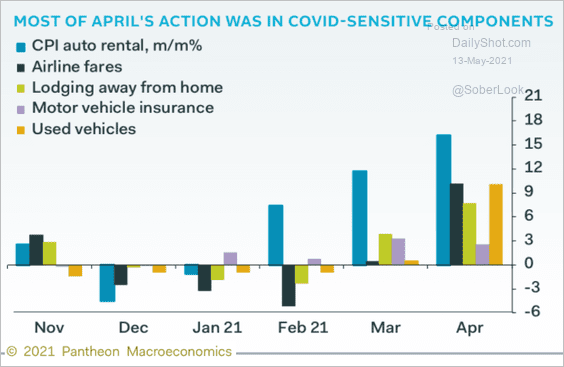

US inflation is temporary. The hottest segments are all COVID-related:

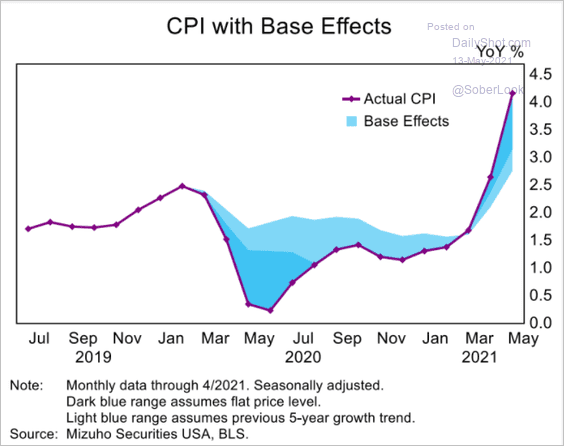

It is heavily influenced by base effects:

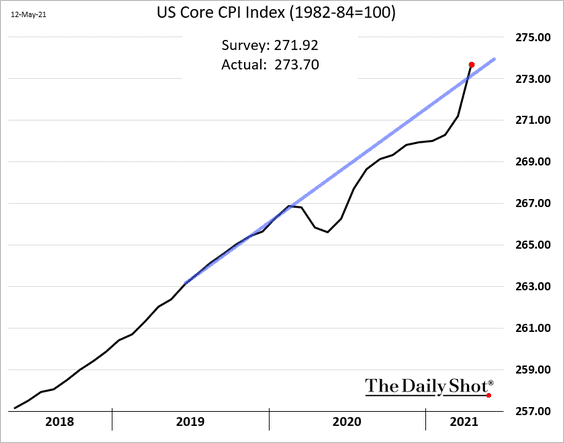

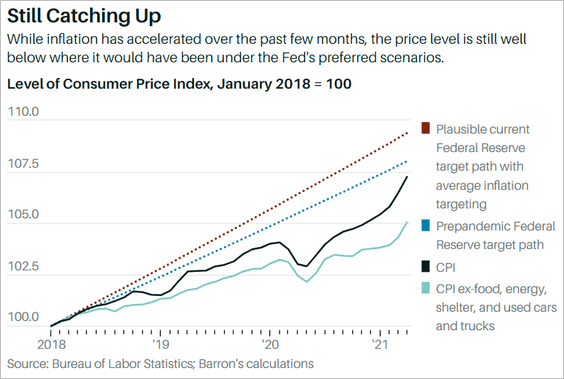

Or, put another way, price catch up:

The spike has another few months to run so sit back and enjoy the inflation panic merchants in action:

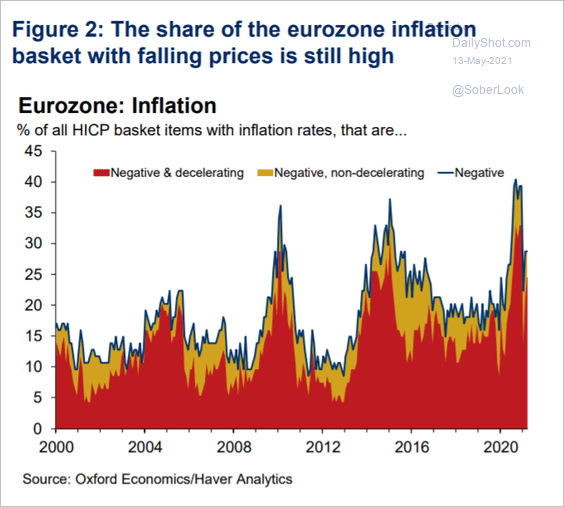

That said, the US does have better inflation prospects over the cycle years thanks to fiscally-led growth. Which compares very favorably to Europe’s endless lowflation, even during today’s price catch up:

This means a strong DXY for the cycle ahead.

Add the coming sharp China slowdown beginning in H2, and the commodities crash that will come with it, and we have the perfect scenario in which the Australian dollar can go from hero to zero.