Overnight action continued the see-sawing action between US yields and other asset classes that has defined the last few months. This time it was yields up and other assets down. DXY was down as EUR bounced:

The Australian dollar was pretty much flat:

Oil and gold were up with all of the usual soft DXY winners.

Metals:

Miners:

And EM stocks:

Junk is still fine:

Yields up:

Stocks down, especially tech:

Westpac has the wrap:

Event Wrap

US Empire (NY) Fed manufacturing survey slipped to 24.3 (vs. estimate 23.9, prior 26,3). There was a notablerise to a record high in prices paid, with hours worked and new orders continuing to firm, while employment slipped to 13.6 from 13.9 but remained expansionary. NAHB homebuilder confidence survey remained at 83 as expected, indicating that the sector continues to foresee a strong market with low inventory.

Fed Vice-chair Clarida reiterated that he wants markets to focus on the goal of returning the economy to full employment, that transitory inflation rises should not be overly concerning but will be monitored, and that it may be a long process to reopen the economy.

Bank of England’s Vlieghe, a dove and whose current term ends in August, referred to the UK economic recovery as a return to normal rather than a boom, that the economy still needs support due to the amount of spare capacity, and that NIRP will be added to the BoE’s monetary tool kit.

Event Outlook

Australia: The RBA will publish the Minutes of the May Board Meeting. The focus will be on commentary around QE and Yield Curve Control, given that the Board will decide whether to extend these policies at the July meeting.

Japan: GDP is expected to contract 1.1% in Q1, with the state of emergency constraining household activity over the quarter.

Euro Area: The second estimate of Q1 GDP will provide more information around the contributions to output (market f/c: -0.6%qtr, -1.8%yr). Meanwhile, the March trade balance is expected to print at EUR 19.1bn, after rising imports pared back the surplus in the February update.

UK: The March ILO unemployment rate is expected to hold at 4.9% with the extended furlough scheme continuing to hold down job losses.

US: April building permits are expected to rise 0.6%, while housing starts should ease off after a catch-up surge in March (market f/c: -2.0%). The FOMC’s Kaplan will participate in a Panel Discussion at the Atlanta Fed Conference.

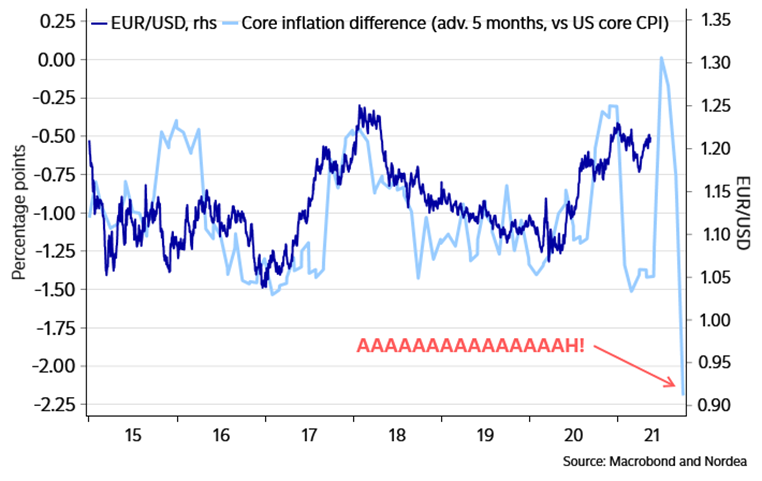

DXY is most often and most directly impacted by EUR. That makes the yield spread between the US and Europe one of the most important in the world for all other asset classes. The recent move downwards in DXY has coincided precisely with a swing in this spread but have a look at what is in the offing:

BofA wraps it up with a nice bow on top:

We continue to look for USD to modestly strengthen this year, and we forecast EUR/USD at 1.15 by year/end. Our USD views largely reflect our expectations for US growth outperformance—fuelled by the sizeableUS fiscal stimulus, the recovering consumer and the fast vaccination rate—and the eventual Fed policy normalization. We remain bearish on EUR for the rest of the year, but the short-term risks are for EUR upside due to the combination of the vaccination catch-up in Europe and the dovish Fed. We also focus on the ECB Strategy Review, which could surprise markets. Although near-term JPY strength is likely, we expect USD/JPY at 113 by year/end because of the recovery in Japan’s outward M&A and higher US rates. GBPcouldremain supported near term, possibly on the back of continued M&A flows into the UK, but Brexit makes us long-term bearish. We are bearish on CHF, particularly vs. USD, and constructive on the commodity block. We still favour relative value and tactical trades.

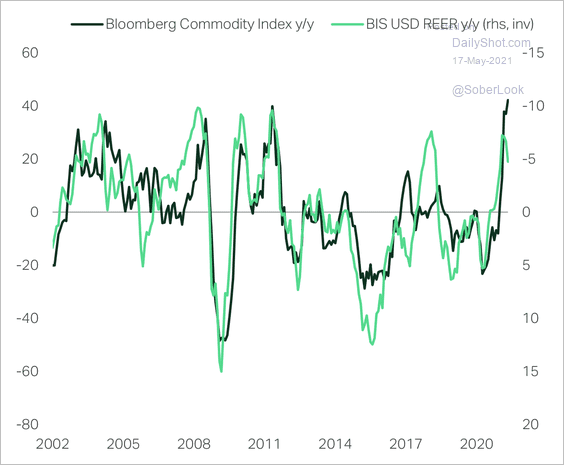

That last point is only short-term. When DXY rises, commodities do not rise as well:

Especially so when China is also slamming the credit brakes.

The base case remains an ongoing DXY bull market driven by US exceptionalism with short-term risk cases around the timing of the China slowdown versus the European rebound.

The Australian dollar is the mirror image of the same.