DXY was stable last night:

The Australian dollar was also stable:

Gold firmed, oil fell:

Base metals lifted again:

But miners mostly fell:

EM stocks were whacked:

Junk eased:

US yields are rebounding:

Which didn’t help stocks:

Westpac has the wrap:

Event Wrap

The Australian Federal Budget surprised with a spending package which is larger than was widely expected, and a budget improvement, beyond 2020/21, which is smaller than expected. The Budget deficit for the 2020/21 financial year of $161bn is considerably lower than the $197.7bn forecast by the Government in the December Mid-Year Economic and Fiscal Outlook (MYEFO). However, the deficits for the following years are, on average, higher than in MYEFO. The revised forecasts are: 2021/22, $106.6bn, 5.0% of GDP ($1.9bn less than in MYEFO); 2022/23, $99.3bn ($14.9bn higher than MYEFO); 2023/24, $79.5bn ($13.5bn larger than MYEFO); and 2024/25, $57bn, representing 2.4% of GDP.

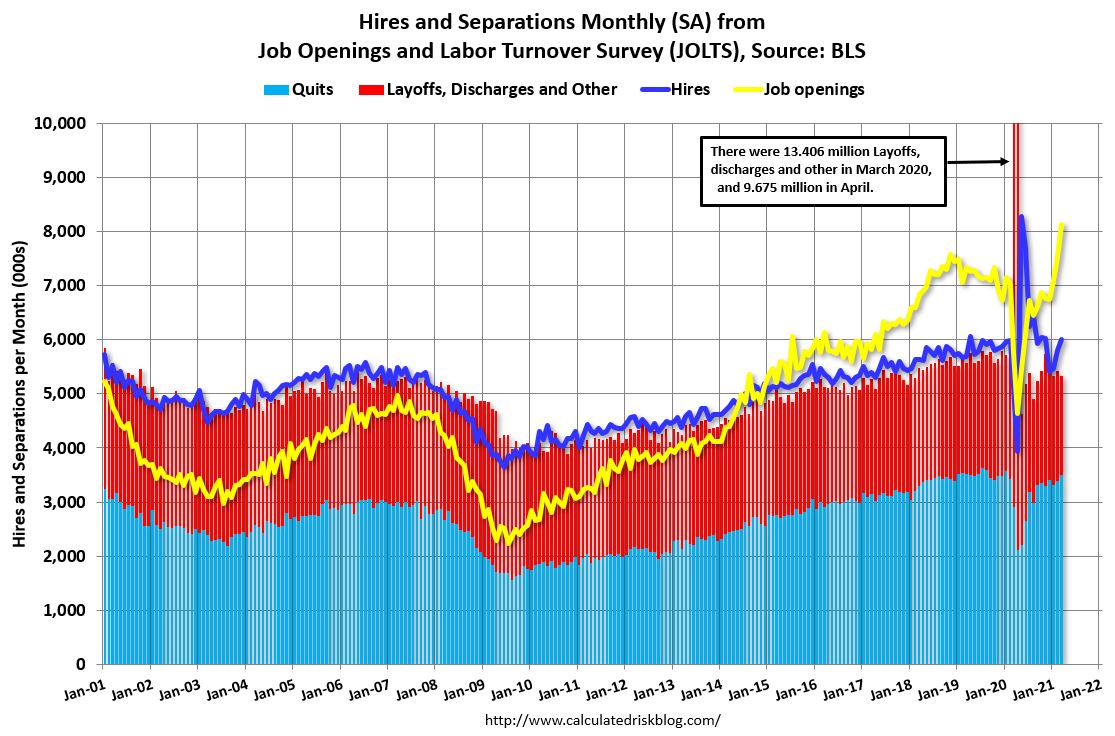

US NFIB small business optimism rose to 99.8 from 98.2 but missed the estimate of 100.8. The JOLTS job openings survey rose more than expected to 8.123m (est. 7.5m, prior 7.526m) – a record high – as the economy re-opens. The survey will add to the suspicion that April’s disappointing payrolls report was related to supply of labour.

The FOMC’s Brainard spoke of the positive improvements in the economy but also focused on the work to be done to achieve goals and the need for patience as risks remain. She said the April jobs report are a reminder that the recovery will be uneven and difficult to predict, and showed the “value of patience”. The jump in prices should be temporary, while inflation expectations remain very well anchored at 2%. Bostic reiterated policy is in a “pretty good place” and it is appropriate for it to remain in accommodative mode. The labour market is still about 8 million workers shy of its pre-pandemic level. He expects a temporary blip in prices which wouldn’t require a response from the Fed. But if prices rose too much, the Fed may have to act and tighten policy. Daly’s take on the disappointing April jobs data was that access to childcare and schools, along with uncertainties over job stability and predictability, have been factors slowing the return of workers. Additionally she said bottlenecks, a transition dynamic for a normal economy, are causing both labour shortages and price increases. She remains bullish on the economy and hopes that it will have climbed out of its hole by 2022. Mester noted the outlook is still bright despite the jobs miss.

Germany’s ZEW economic survey beat expectations, rising to a 2–year high of 84.4 (est. 72.0, prior 70.7), with current conditions rising to -40.0 (prior -48,8, est, -41.6). Eurozone expectations also rose, to a 20-year high of 84.0 (prior 66.3), indicating potential for a recovery in H2’21.

Event Outlook

Euro Area: March industrial production is expected to rise 0.8%, with manufacturing remaining the key source of strength for Europe.

UK: Q1 GDP is expected to contract 1.6% (-6.1%yr), but this will be followed by a robust rebound over the second half as restrictions relax.

US: The market expects that April CPI will rise 0.2%, which will push the year-ended pace to 3.6% on base effects. The April monthly budget statement deficit will remain wide as fresh waves of stimulus come online (market f/c: -100.0bn). Vice Chair Clarida will talk on the US economic outlook.

JOLTS were also very strong:

The debate in markets now is how much and how persistent will be inflation. The recent US labour market data, with strong job openings but weak job gains, led to the market betting on the Fed staying easier for longer. But for several days now we’ve had the opposite as the market swings back to the MB view that labour supply issues, if they materialise, will be inflationary and bring forward Fed tightening.

That said, I remain of the view that it’s too early to call. Employment reports are notoriously afflicted with Numberwang and one report does not a summer make.

It is odd that the rising yields have not yet resulted in a lift for DXY, as happened during the last bond back-up in March. Though they have stopped it from falling.

I guess we can put that down to the same confusion about where US labour is headed that I have for now.