The bond backup is back and risk assets don’t like it with all kinds of action around the Australian dollar last night. DXY took off:

The Australian dollar was pounded against all DMs:

Gold was smacked. Oil held:

Base metals flamed out:

Big miners rolled over:

EM stocks look like a suicidal cliff jumped:

Junk was hit:

As US yields took off:

And stocks were smashed, led by tech:

Westpac has the wrap:

Event Wrap

US CPI in April rose by a surprisingly large 0.8%m/m (est. +0.2%m/m) to 4.2%y/y (est. +3.6%y/y) – the largest monthly gain since 2009. Core measures also surprised, ex-food and energy up 0.9%m/m (est. +0.3%m/m) to 3.0%y/y (est. 2.3%y/y) – the largest monthly gain since 1981. Among the components, the largest surprise was the record 10.0%m/m rise in used vehicle prices, but gains were broad-based.

FOMC Vice-chair Clarida spoke shortly after the CPI data, and reiterated the official stance: “These one-time increases in prices are likely to have only transitory effects on underlying inflation, and I expect inflation to return to — or perhaps run somewhat above — our 2% longer-run goal in 2022 and 2023”, adding “this outcome would be entirely consistent with the new framework the Fed adopted in August 2020.”He noted more concern over the labour market which “appears to be more uncertain than the outlook for activity.”

Eurozone industrial production in March was weaker than expected, rising a mere 0.1%m/m (est. +0.8%m/m, prior revised to -1.2%m/m from -1.0%m/m).

The EU increased its regional growth projections for 2021 to 4.2% (from 3.8%), and for 2022 to 4.4% (from 3.7%), assuming successful pandemic vaccination programmes.

UK GDP in Q1 fell 1.5%q/q, slightly better than expected (est. -1.6%), with low private consumption and business investment offset by governmentt spending and lower imports.

Monthly production data for March was better than expected, with industrial production rising 1.8%m/m (est. +1.0%m/m) and GDP rising 2.1%m/m (est. +1.5%m/m).Event Outlook

Australia: The May update of MI inflation expectations will be released. Expectations jolted lower in April and are firmly below pre-COVID levels.

New Zealand: We expect the April food price index will rise 0.8% on higher fruit and vegetable prices. The April REINZ report will be the first comprehensive read on the strength of the housing market since the Government’s announcement in late March, which significantly tightened up the tax treatment of property investors. Indicators so far suggest that house sales were still perky through April, although auction clearance rates fell. The key new information will be whether prices have continued to be bid up at the white-hot pace seen in recent months.

US: The April PPI should lift 0.3% on rising commodity input prices. Initial jobless claims have printed fresh pandemic lows in recent weeks – the market is looking for another fall to 490k in the week ended May 8. The FOMC’s Waller and Bullard will speak.

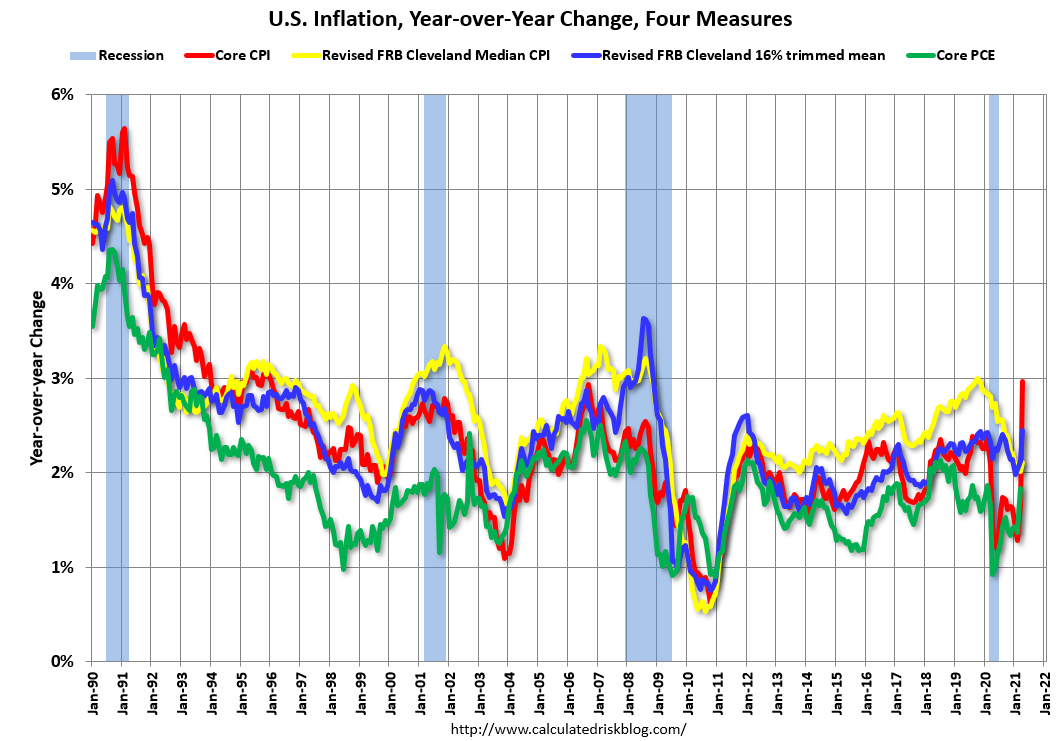

The key release was US CPI which blasted off (no surprise at all to MB readers). Core CPI roared to 3%, trimmed mean to 2.4%, and the key measure, Core PCE, to 1.8%:

This is a mix base effect and supply-side bottleneck inflation. It is temporary. A more serious inflationary challenge will emerge from the fiscally-primed US labour market over 2022.

But, even that is going to face a very large challenge. A deflationary tsunami is mounting in slowing Chinese credit and it will break upon the world before long.

Soon enough, deflating commodity prices and a falling Australian dollar will join tumbling EMs and a rising DXY to burst this inflation pimple.