DXY was down again last night after its brief flirtation with unexpectedly hawkish Federal Reserve minutes. EUR is strong:

The Australian dollar jumped though remains heavily contrained against all DM crosses:

It is losing altitude versus EMs now as well:

Probably the major trigger for the night was slumping oil as the Iran deal looks likely to be done:

Which dragged on all commodities despite a falling DXY:

And big miners:

EM stocks are still stalled:

Junk is fine:

US yields fell with oil:

Which unleashed tech once more:

Westpac has the wrap:

Event Wrap

US Leading Index for April rose by 1.6% to a record high (estimate +1.3%), with gains assisted by jobless claims, though the workweek was a negative contributor. Weekly initial jobless claims fell to 444k (estimate 450k, prior 478k), although continuing claims rose to 3.75m (est. 3.63m). The Philadelphia Fed survey for May fell more than expected, but remained above the pre-Covid range. The index fell from 50.2 to 31.5 (est. 41.0), with employment (to 19.3 from 30.8) falling the most along with the 6-month outlook (to 52.7 from 66.6). Prices paid rose to 76.8 (prior 69.1) and prices received to 41.0 (from 34.5).

FOMC hawk Kaplan again said that discussion of scaling back Fed tapering and “taking the foot gently off the accelerator” would be wise, and that other Fed members were open to debating tapering in coming meetings. He said the April jobs report exposed labour supply issues and suggested that unemployment benefits are making workers hesitant to return to work.

Bank of Canada Gov. Macklem delivered a relatively positive Financial Stability Report but highlighted abnormally low interest rates, household leverage and housing credit as areas of concern.

Eurozone construction in March showed a marked rebound of +2.7%m/m after the 2.0%m/m fall in February.

Event Outlook

Australia: On balance we expect April preliminary retail sales to be up 0.8%, with annual growth set to spike to an extraordinary 24%yr on base effects from last year’s lockdown. Consumer sentiment hit an 11yr high in April as the further relaxation of COVID restrictions and a strong housing upturn more than offset concerns about the expiring JobKeeper scheme and setbacks to vaccine rollouts. However, this may not see much of a boost to retail as reopening rebounds are driving a big switch back into spending to service sectors, outside the scope of the retail survey.

Europe: May Markit manufacturing and services PMIs are due for the Euro Area and the UK.

Euro Area: May consumer confidence will find support in the improvement of the vaccine rollout (market f/c: -6.5).

UK: Ahead of the May release, GfK consumer sentiment has been approaching pre-pandemic levels and will continue to rise as restrictions relax (market f/c: -12). April retail sales are expected to rise 4.5% and will continue to strengthen as we move into H2.

US: May Markit manufacturing (market f/c: 60.1) and services PMIs (market f/c: 64.4) are due, and will both be spurred by the reopening, stimulus and buoyant consumer spending. Existing home sales are set to rise 0.8% in April; in recent months, elevated prices and a lack of supply have constrained turnover.

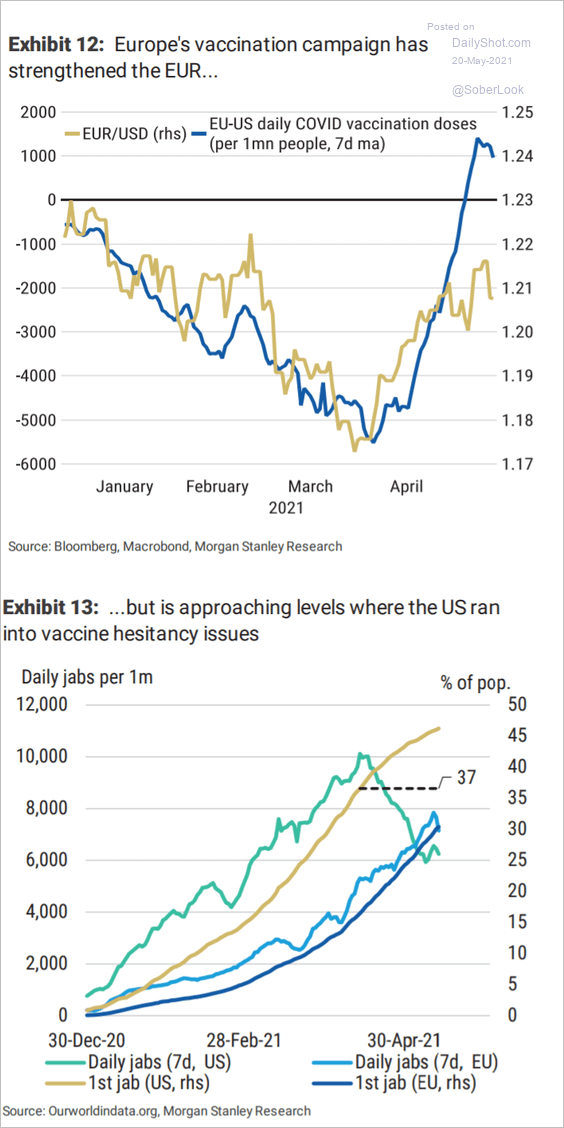

Oil and the USD are typically inversely correlated but one gets the feeling that right now a falling feather could take DXY lower. The major reason is EUR which is benefiting from getting its vaccine act together:

European yields have been rising accordingly.

For the time being, this forex pattern is more typical of a normal cyclical recovery in which strong US growth led by low interest rates and a rising European export recovery triggers capital outflows to the latter. As said for the past few months, this is a risk case for a stronger for longer AUD if it transpires ahead of looming Chinese weakness. For now, that is playing out.

So long as that narrative persists we can see more of the same. How far the AUD gets is open for debate. It must be observed that it remains very weak in the circumstances with record-high terms of trade all but ignored.

One reason is certainly the heroic efforts of the RBA. One wonders if China’s trade war isn’t now playing a major role as well. The AUD underperformance among the commodity exporters basket is stark.

I still expect record commodity prices to deflate moving through H2 and into 2022 as China slows, irrespective of movements in DXY, so will use any bouts of AUD strength to shift assets offshore.