Why macroprudential mortgage curbs are harder this time around

Advertisement

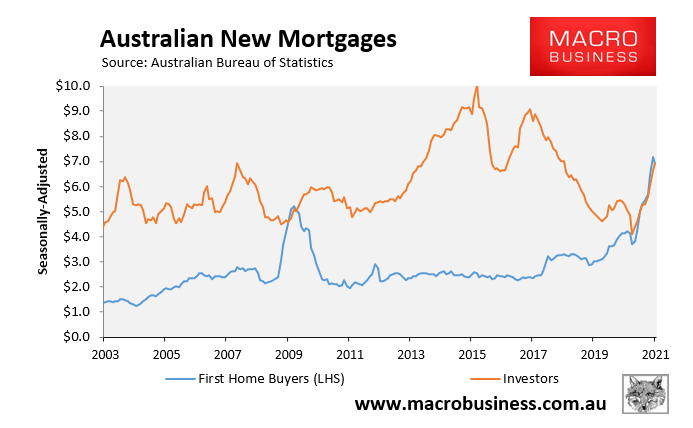

Several commentators have questioned the efficacy of Australian financial regulators imposing macroprudential mortgage curbs, arguing that it would disproportionately harm first home buyers (FHBs) who tend to take out larger mortgages with smaller deposits:

- Alison Pennington, senior economist at the Australia Institute’s Centre For Future Work, claims macro-prudential tightening “would have unequal and unfair consequences on people trying to get into the market if they increase the size of deposit to the size of the loan”.

- Brendan Coates from the Grattan Institute warns these macro-prudential tools “are not costless” because “first-home buyers typically are disproportionately affected”. This is why “APRA is reluctant to use them unless they are worried about financial stability”.

- Meanwhile, Westpac’s Matthew Hasan argues macro-prudential curbs may not be needed at all because the current boom is not been driven by investor loans and interest-only loans, which are at “feeble levels”. Rather, it is being driven by home-owners and fuelled by ultra-low interest rates.

My view is that the Australia’s financial regulators will be reluctant to act because the mortgage/property boom is currently being driven by owner-occupiers (especially first home buyers), which makes macro-prudential intervention inherently more difficult than clamping down on speculative investors.

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement