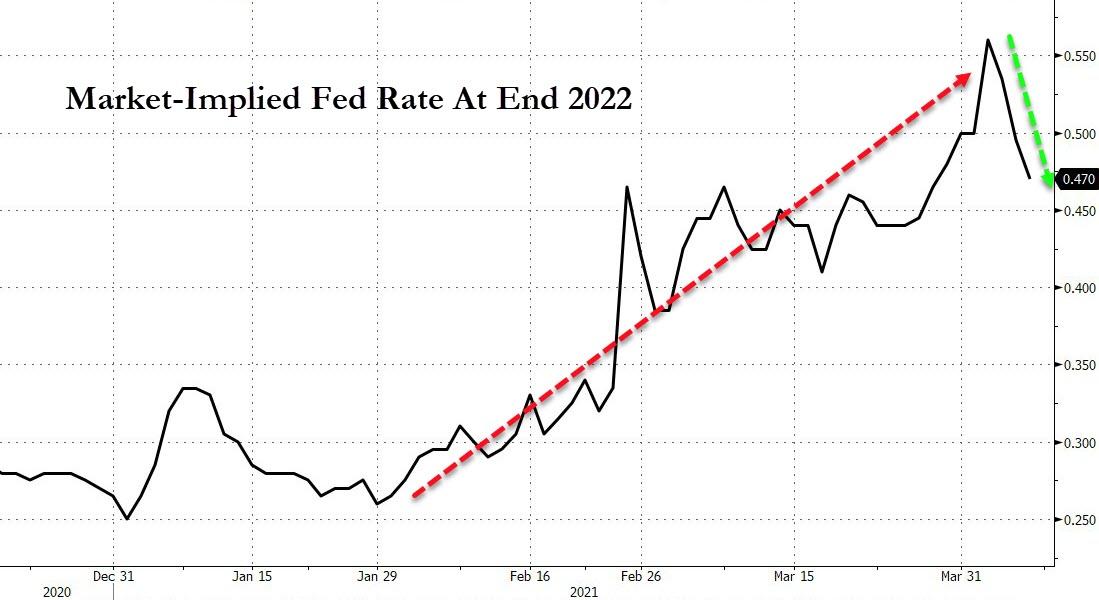

Markets clearly think it’s coming very fast. Fed fund futures are pricing two cash rate hikes for 2022, let alone tapering of asset purchases, which will have to come first:

Fight the Fed!

That is far too aggressive to my mind. US inflation is going to fall away next year as commodities deflate while China slows, even if US core inflation remains warm thanks to strengthening wages.