It is amusing to watch bottom-up analysts try to make sense of, and defend, Australia’s buy now, pay later bubble stocks.

I know nothing of these stocks. But I can identify a top-down market trend when I see one. APT was never about much more than a monetary bubble produced by COVID-19. Just as was the case for all profitless tech:

I love COVID-19!

It was some whacko combination of a surge in growth stocks that did benefit from accelerated trends to online business and enjoyed an earnings boom during the pandemic. A surge in retail trading which drew in a new generation of technoweaners. And a surge of cheques from the worldwide treasuries hitting desks that had little else to do but punt it.

Advertisement

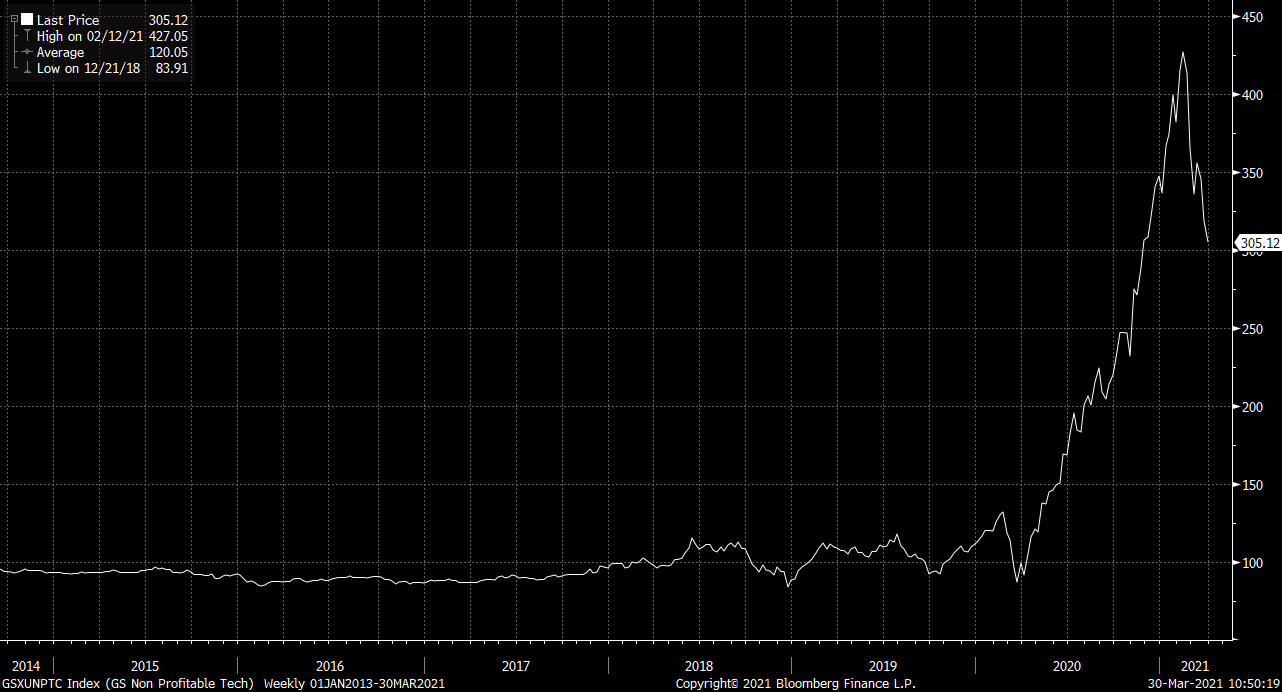

This was what drove Australia’s BNPL boom, not the development of the businesses themselves. Check out the correction between APT and the ARKK, the leading tech bubble ETF:

Buy now, regret later

Following the rout of the past few months, the last week of trading has witnessed a little bounce in these stocks and ETFs. Again, in my view, it has very little to with the individual names and a whole lot to do with macro-driven stock factor rotations.

Advertisement

I put it to you, most significantly, this chart:

What popped the profitless tech bubble was rising US yields, in part driven by oil. When yields rise, growth stocks shift out of fashion as investors look for more immediate returns. This applies doubly to anything that makes no money whatsoever.

But, as you can see, oil has stopped rising. Indeed, the rally is all but over (in my view). That has helped forestall the rise in US yields.

Advertisement

So, we might ask, is it time to buy back into growth and, in particular, the more speculative end of that market where BNPL lurks?

That depends a lot more on your macro narrative than it does the individual stocks, which are clearly bubble-priced.

If you think that the market is going to be dominated by “bad news is good news” then the answer is maybe “buy the tech wreck” because that will mean ongoing disinflation, more monetary tailwinds and reverse rotation from value.

If you think that the prevailing market narrative is more likely to be “good news is bad news” then the answer is “not yet” because rising yields will continue to deflate the no earnings bubble before it takes down all stocks.

If you think that the forthcoming dominant narrative is “good news is good news” then the answer is “no” because rising yields are a good sign for profits and growth will continue to deflate as value rotation roars on.

Advertisement

So, which is it? Goldman is in the “bad news is good news” camp:

Market inflation expectations have continued to drift higher amidst a growing debate about the risks of overheating and high inflation. We offer our perspective in a series of four questions.

How high is the risk of overfilling the output gap? Our analysis of the impact of reopening, fiscal support, pent-up savings, and easy financial conditions implies that GDP will overshoot potential by about 1% next year and the unemployment rate will eventually fall to the low 3s. But the uncertainty is greater than usual. The key upside risk is that greater fiscal support and spending of pent-up savings than we expect could add 1-2% to the level of GDP and push unemployment below 3%, and we would see greater inflation risk in that case.

How high is the risk of a larger inflation overshoot? We expect core PCE inflationto rise to 2.1-2.2% by 2023-2024, above the peak seen last cycle but in line with the Fed’s goal under its new framework. A more substantial overshoot of another ¼-½pp is possible, as local-level data show that moderately above target inflation has actually been fairly common in extremely tight labor markets. But the much larger overshoots that some commentators have suggested are less realistic, in our view, because only 40% of the core PCE index shows consistent cyclicality and the large health care category is likely to remain depressed by policy pressures in coming years.

BofA is in the “good news is bad news” camp:

Advertisement

Et Q2 Brutus? kicks off with 2nd highest PE since 1901 (Chart 2),melt-up sentiment, strongest macro since WW2 (Chart5 – 6), epic Keynesian stimulus (Chart8), record small biz unfilled jobs (Chart7), US/UK/Oz/NZ house prices +10-20%, US$ share of global FXreserves (59%) lowest since 1995, bond tapering beginning (Canada), BRICs tightening; Q2 bull risk = low US inflation + EU vaccine reopening; Q2 bear risk = >2% bond yields + more deleveraging events; either way secular bull markets now inflation & volatility.

The third position of “good news is good news” is held by yours truly. We see:

An ongoing global profits boom as reopening transpires.

Goldilocks inflation not least because US exceptionalism and Chinese slowing will together deliver serious commodity deflation to offset other inflation drivers including monetary and fiscal stimulus.

Ongoing value rotation preventing any kind of market rout.

Advertisement

It is closer to the “bad news is good news” scenario because it is unconvinced by the sustainability of inflation despite the Biden Administration’s best efforts. But, it is still not very favourable for growth stocks because it includes no further Fed easing.

So, there is no market scenario yet that suggests buying profitless tech. For that, we really need to see another disinflation accident. Moreover, until then we’ll see more big margin calls like Archegos.

Hence I see today’s rebounds in BNPL as bear market rallies. This is not to say that some will not be worth something eventually.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.