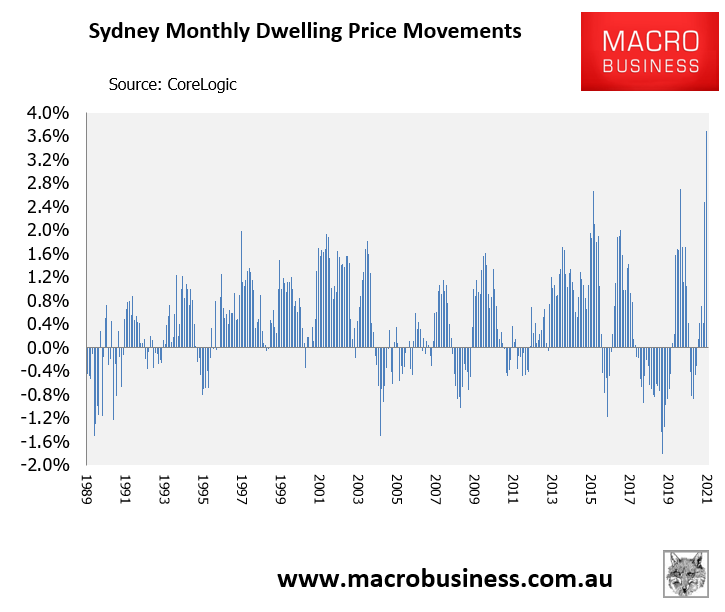

CoreLogic’s March dwelling value results recorded a whopping 3.7% monthly rise in Sydney home values, which was the strongest monthly result since August 1988:

Sydney recorded the strongest monthly growth in nearly 33 years in March 2021.

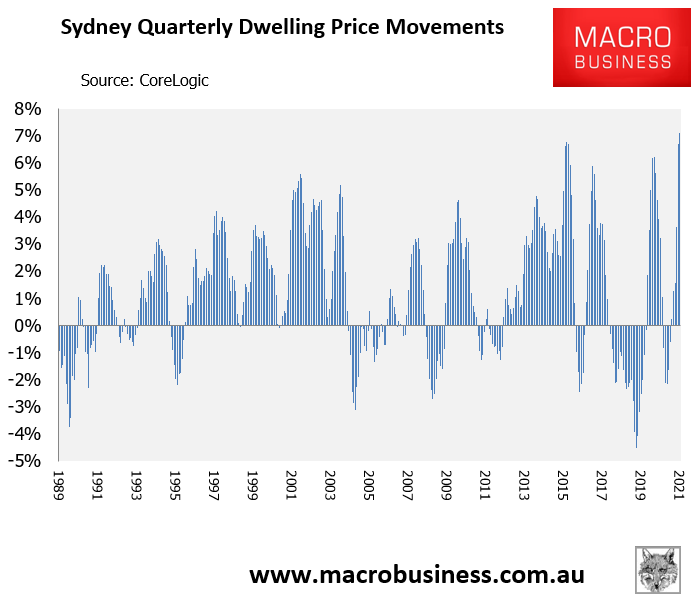

As of yesterday (i.e. 6 April 2021), Sydney’s quarterly dwelling value growth was tracking at an insane 7.1%, which is the strongest quarterly growth since October 1988:

Sydney’s quarterly dwelling value growth (7.1%) is the strongest in more than 32 years.

Thus, the last time Sydney’s property market was this strong was in Australia’s bicentenary year, when Kylie Minogue’s debut hit Loco-Motion was topping the global charts.

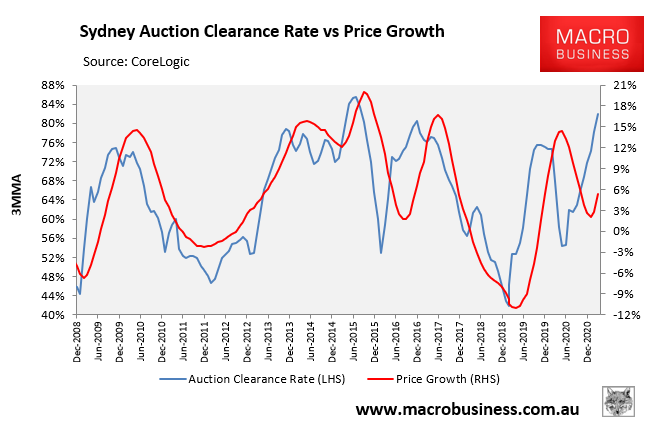

The strength of Sydney’s property market is reflected in the city’s auction clearance rate, which has remained above 80% for eight consecutive weeks:

Sydney’s auction market has gathered steam, with clearances well above 80%.

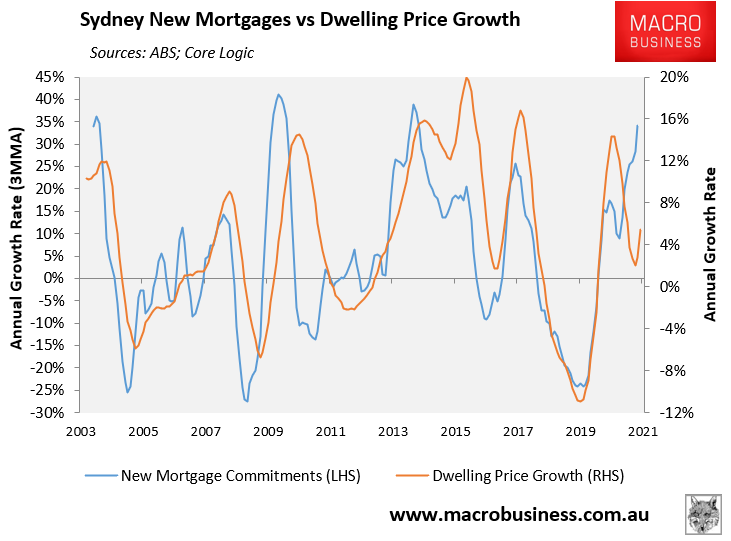

New mortgage finance commitments are also running hot, reflecting the strong demand for Sydney property:

Sydney’s mortgage demand has gone vertical.

We’ll know that prices are about to slow when Sydney’s auction clearance rate and mortgage growth starts to turn down.