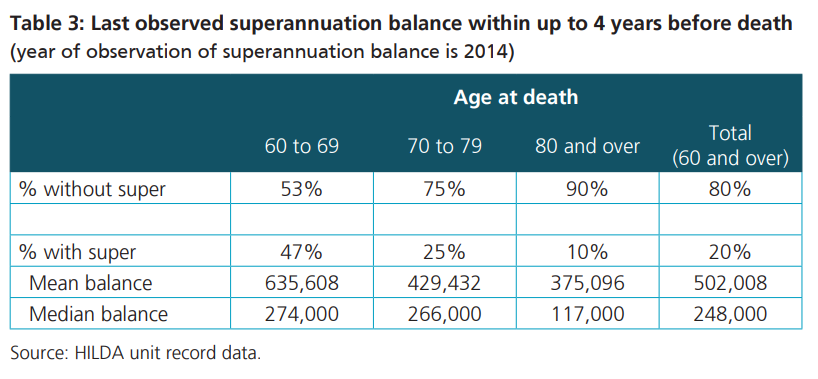

The Association of Superannuation Funds of Australia (ASFA) released research yesterday claiming that 80% of people aged 60 and over died with no superannuation savings between 2014 to 2018, with 90% of these people having no super in the four-years prior to their death:

80% of people died without superannuation savings, according to ASFA.

Predictably, ASFA has used these findings to strengthen its call to lift the superannuation guarantee (SG) to 12%, from 9.5% currently:

Given that a large proportion of current retirees have very modest superannuation balances, the case is strengthened for increasing the Superannuation Guarantee (SG) to 12 per cent (as currently legislated) so that retirees can live in retirement with dignity.

ASFA has clearly generated this report for shock value. But there is nothing to be alarmed about in these findings.

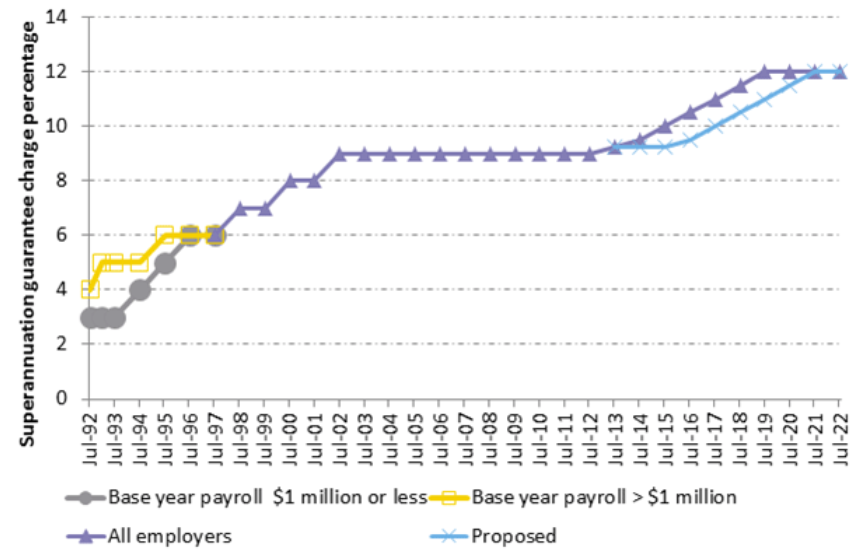

Australia’s compulsory SG has only been in operation for 29 years and began at a low rate (see next chart). Therefore, those that died without super did not participate in the system for the bulk of their working lives.

Australia’s compulsory superannuation system has only been in operation since 1992.

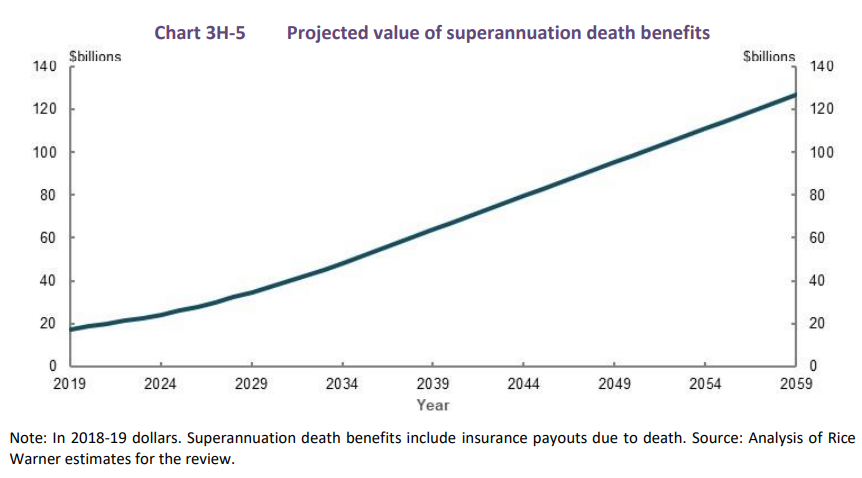

The Australian Treasury’s Retirement Income Review, which handed down its report late last year, also concluded that “most people die with the majority of wealth they had when they retired” and noted that “as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances”.

The Review projected that if current spending/savings patterns persist, then superannuation death benefits would “increase from around $17 billion in 2019 to just under $130 billion in 2059”:

Superannuation death benefits are projected to soar over coming decades.

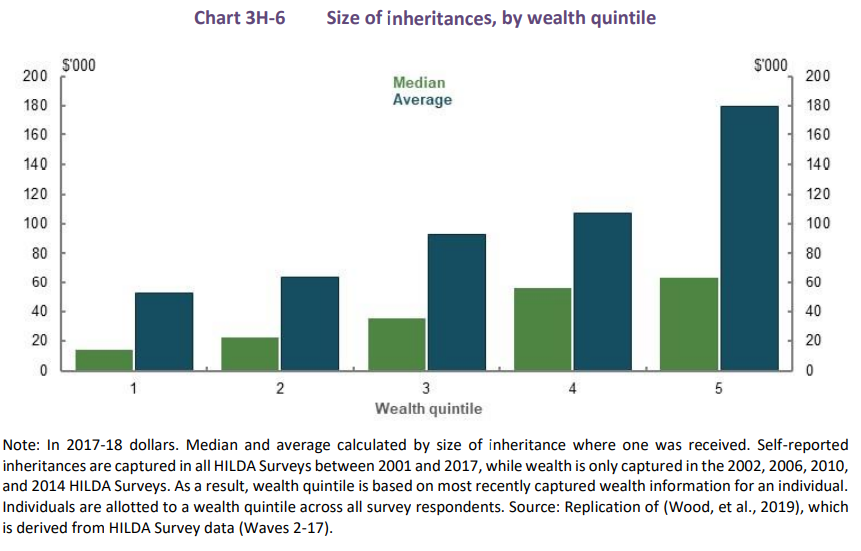

Moreover, because higher income earners accumulate the biggest superannuation nest eggs, the passing of fund balances onto their heirs will inevitably “increase intragenerational inequity”:

Australia’s superannuation system entrenches inequality.

Ultimately, the above data shows one of the inherent flaws in Australia’s superannuation system: longevity risk. Because nobody knows how long they will live, they risk saving either too much or too little.

Moreover, because superannuation savings depend on how long somebody works and how much they earn, the system is automatically biased towards higher income earners with unbroken work patterns (mostly men). This inequity is made worse by superannuation’s tax settings, which give the biggest concessions to higher income earners.

The Aged Pension holds none of these pitfalls. It is universally available until somebody dies, thereby eliminating longevity risk. Further, because the Aged Pension is means tested, it necessarily benefits lower income earners more than higher income earners, improving equity.

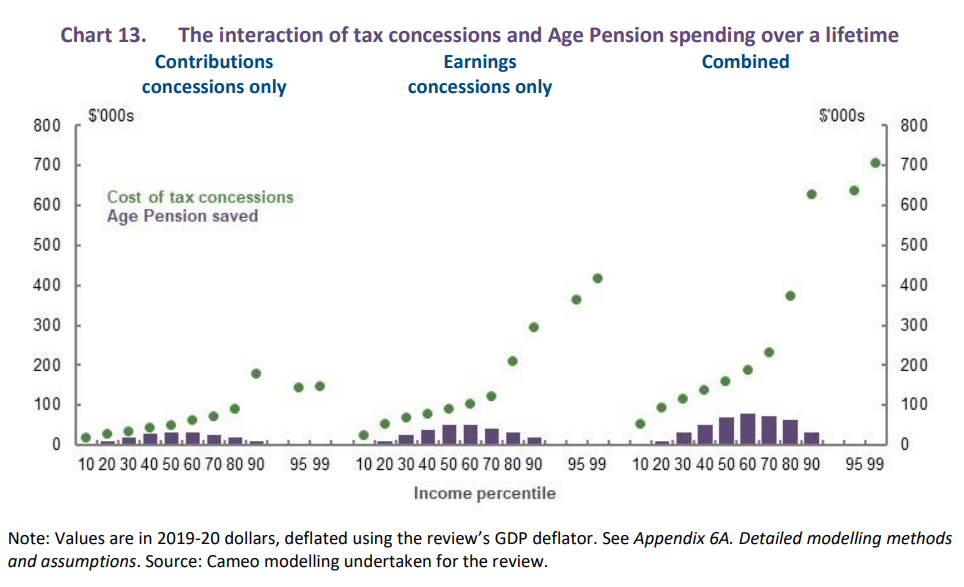

Lifting the SG to 12%, as advocated by ASFA, will not fix the underlying flaws in the system. Rather, it will magnify existing inequalities and damage the long-term sustainability of the federal budget, as illustrated clearly by the Retirement Income Review:

The budgetary cost of superannuation concessions is enormous and will only worsen if the SG is raised to 12%.

It would be far more equitable and efficient to scrap lifting the SG and instead reforming the concession system to make it more progressive. This way, lower income earners could accumulate bigger retirement balances (with higher income earners accumulating smaller balances) without lowering wage growth or further draining the federal budget.

Sadly, industry groups like ASFA continue to talk their book in lobbying to raise the SG to 12%, since it offers fund managers the opportunity to skim bigger fees. Always follow the money.