The Grattan Institute has released a useful blog post explaining why we shouldn’t concern ourselves with the increase in federal government debt:

A report released this week by the independent Parliamentary Budget Office (PBO) affirms that there is no need to be concerned about whether our debt levels are sustainable over the medium-term. The PBO does not project any realistic scenario where the overall level of debt fails to stabilise as a share of the economy, and the interest cost of debt – an important measure of debt sustainability – remains at a manageable level in every scenario…

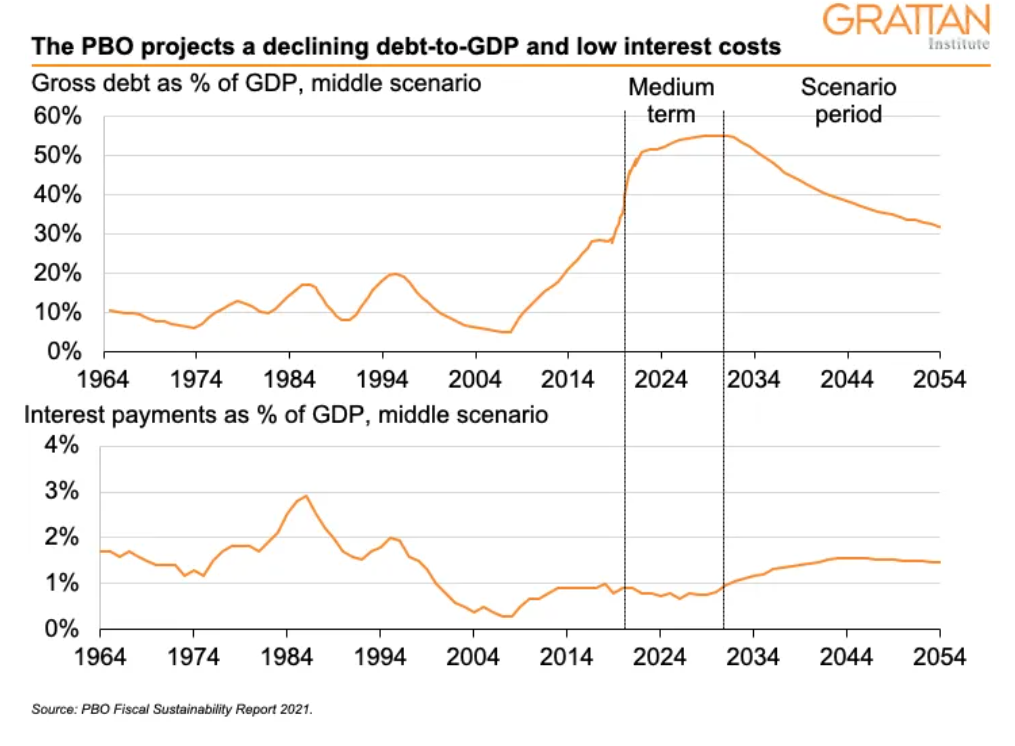

In its medium scenario (see figure), the interest rate on 10-year bonds is assumed to reach its long-run rate of just over 5 per cent in around two decades (the same assumption underpinning the 2020-21 Budget). The budget (including interest costs) is assumed to be in a structural deficit. And nominal GDP growth is assumed at around 5 per cent, based on assumptions about population growth from the Australian Bureau of Statistics and participation and productivity assumptions rom the last Intergenerational Report. Subsequent scenarios vary one, two, or all three of these assumptions above and below the medium level.

The current interest rate is at a historic low, well below the nominal growth rate. And even the long-run interest rate – which is two decades away in the medium scenario – is similar to the nominal growth rate. When growth outstrips interest rates, the amount of debt relative to the economy can fall even if the government continues to run deficits. In fact, if inflation picks up while interest rates are still low, there may even be a period where the real interest costs are negative – that is the government is effectively being paid to borrow.

The upshot is that, under the range of economic conditions the PBO considers in its projections, debt as a share of GDP can remain stable and in some scenarios may even fall without a surplus…

Australia’s debt levels are low by international standards, and they will not undermine the sustainability of the government’s finances – or the confidence of consumers and businesses – for as long as interest costs remain manageable and the level of debt remains stable…

All of this means that the government does not need to cut overall spending to ‘get its house in order’, especially if that spending would have supported economic growth. Well-targeted stimulus in the immediate-term and productivity-enhancing reforms over the short- and medium-term can boost growth and improve the government’s debt position at the same time…

The strategy the Treasurer has outlined today appears sensible – the benefits of getting unemployment down and wages growing are big, and, as the PBO report confirms, the downside risks to long-term fiscal sustainability are small.

Instead of worrying over budget deficits, the federal government’s role should be to ensure optimal economic activity and employment.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.