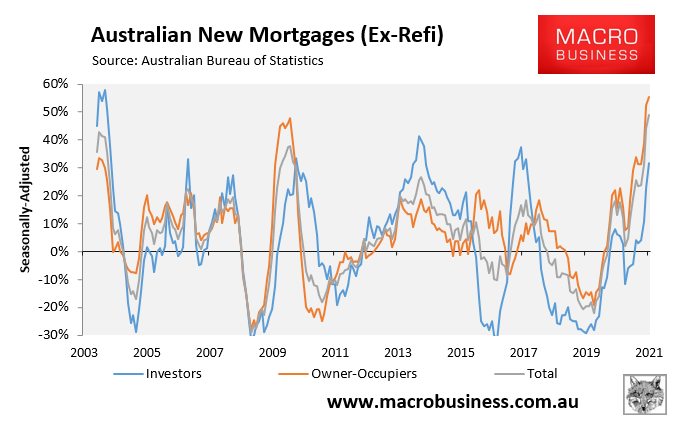

As regular readers know, I consider the growth rate in new mortgage commitments to be the number one short-term indicator for Australian property prices.

This is due to the incredibly strong historical correlation between new mortgage commitments and dwelling value growth.

On Thursday, the Australian Bureau of Statistics (ABS) released data on new mortgage commitments for the month of February, which reported the strongest annual rate of growth in the series’ history, driven by owner-occupiers:

The strongest mortgage growth on record was reported in February by the ABS.

In the year to February 2021, the value of new mortgages issued grew by 49%, exceeding the previous peaks of 41% (September 2003) and 37% (August 2009).

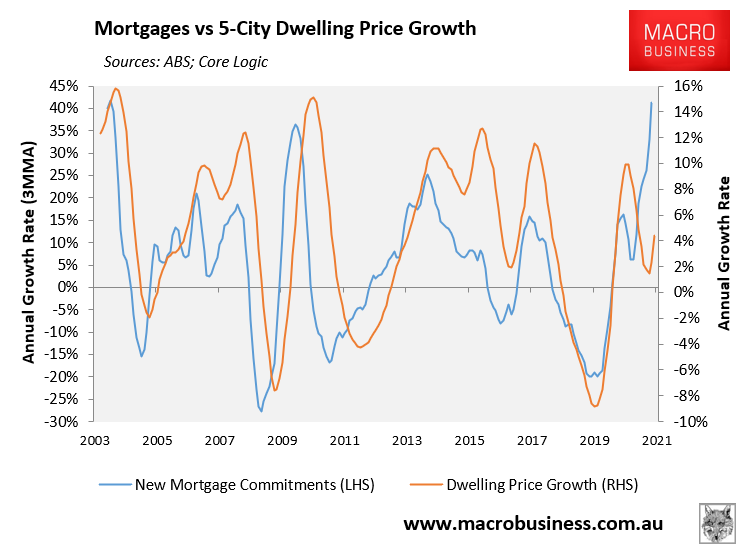

As illustrated in the next chart, this boom in mortgage growth is pointing to strong property price appreciation across the combined five major capital city markets:

Based on historical correlations, the boom in mortgage commitments is pointing to further strong property price growth.

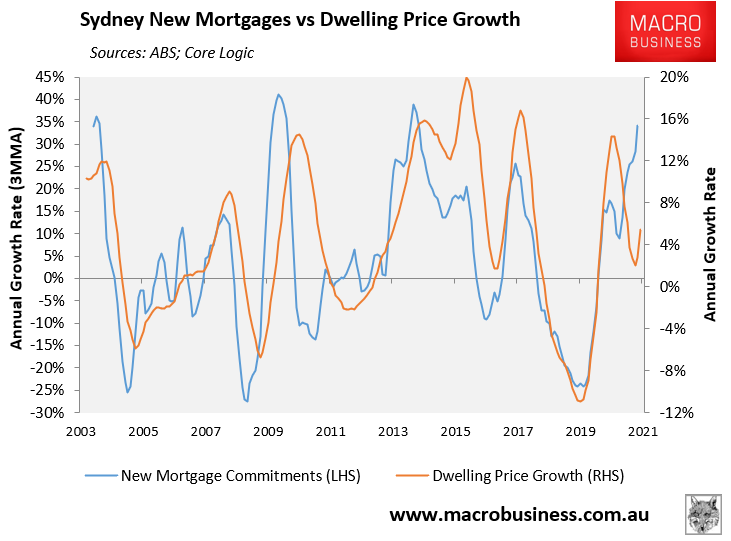

The story is similar across each of the five capital city markets, which are all experiencing booming conditions.

The next chart shows Sydney, where mortgage demand is approaching prior peaks:

Sydney’s mortgage demand is approaching prior peaks, signaling strong property price growth.

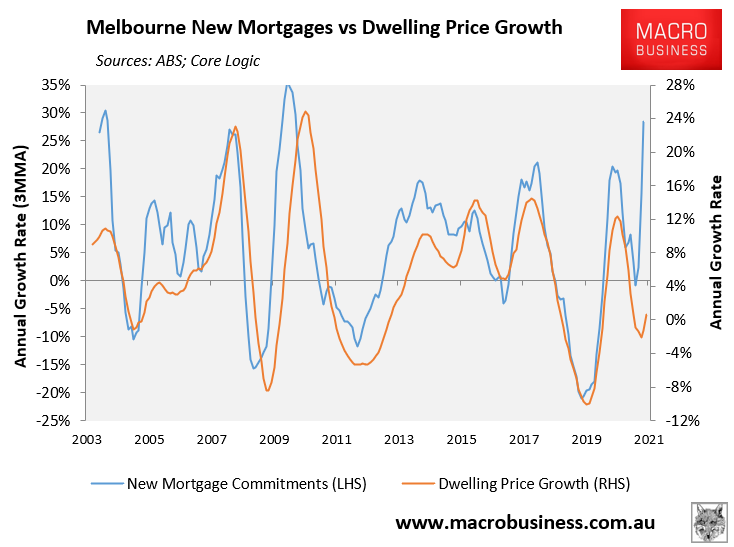

Melbourne is experiencing the strongest mortgage demand since 2009, pointing straight up for property prices:

The growth in Melbourne’s mortgage demand is the strongest since 2009.

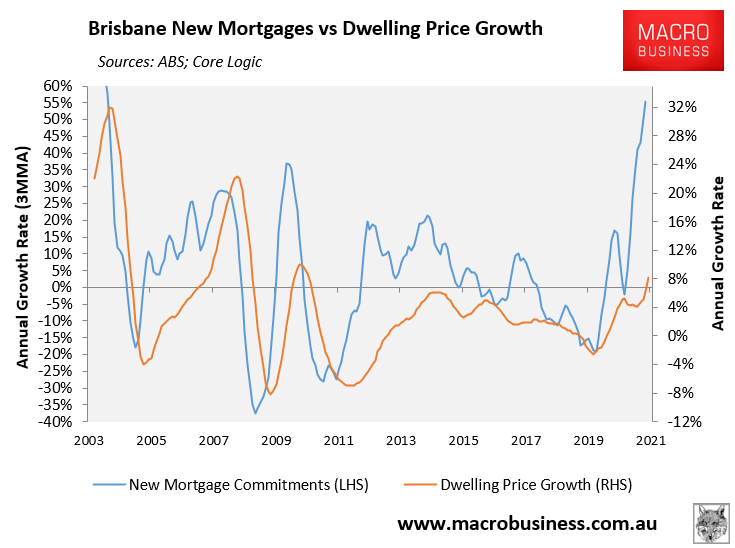

The growth in Brisbane’s mortgage demand is the strongest since 2003, pointing to a possible 20% lift in dwelling values:

The last time Brisbane mortgage demand was this hot was in 2003.

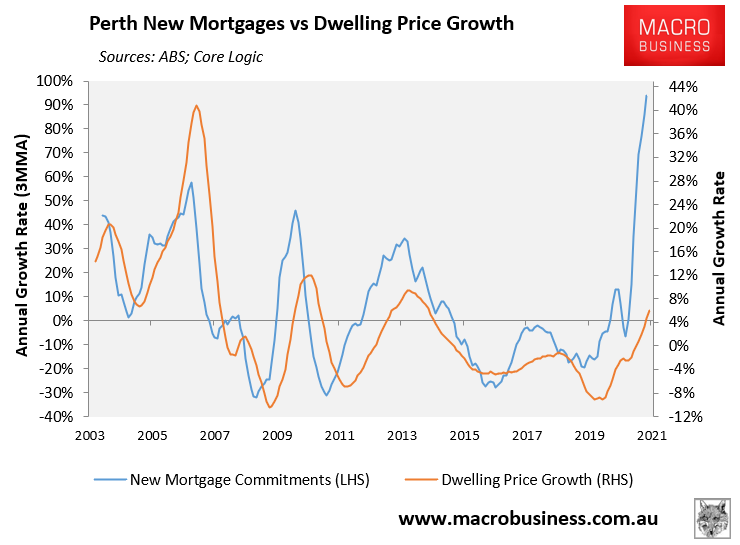

Perth’s mortgage demand is even hotter, breaking all prior records, and pointing skywards for property prices:

Perth’s mortgage demand has never been hotter.

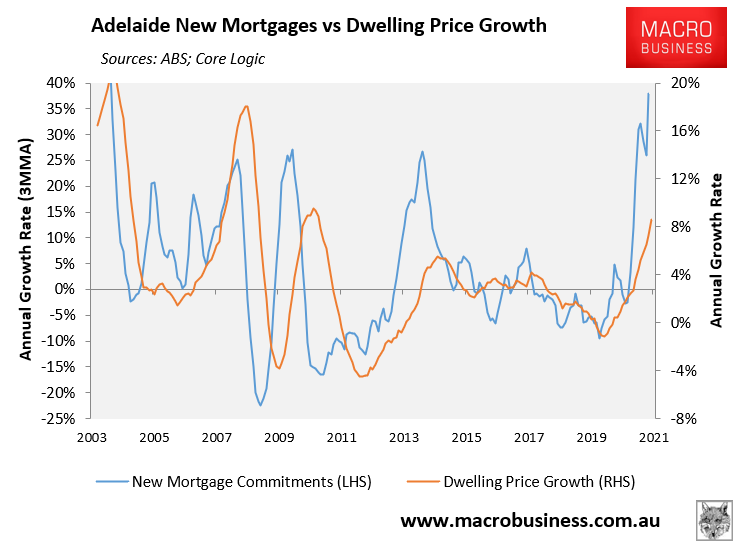

Finally, Adelaide’s mortgage demand is the hottest since 2003, with prices following:

The last time Adelaide’s mortgage demand was this hot was in 2003.

In short, a synchronised mortgage and property price boom is currently taking place across Australia.

We will know that the boom in property values is beginning to wane once the growth in new mortgage commitments starts to fall.

Until then, onwards and upwards.