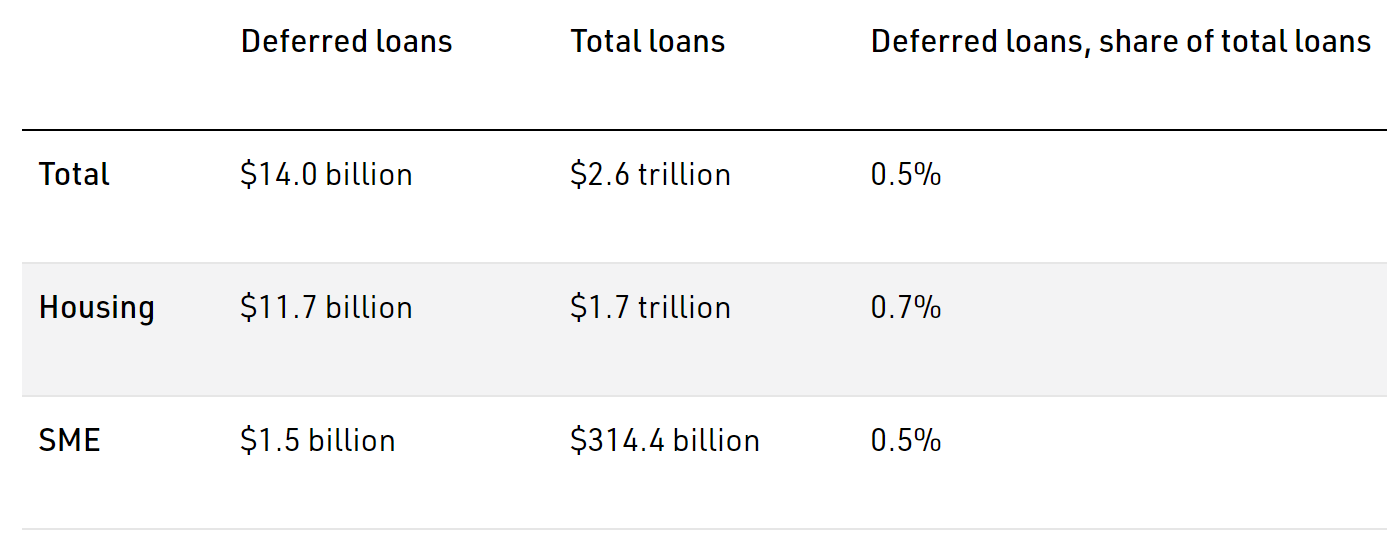

New data from the Australian Prudential Regulation Authority (APRA) shows there were only $14 billion worth of loans that were still on a deferred repayment plan at the end of February 2021. This comprises $11.7 billion worth of mortgage loans and $1.5 billion of loans to small and medium enterprises (SMEs):

The number and value of deferred loans has shrunk immensely since the peak of the pandemic.

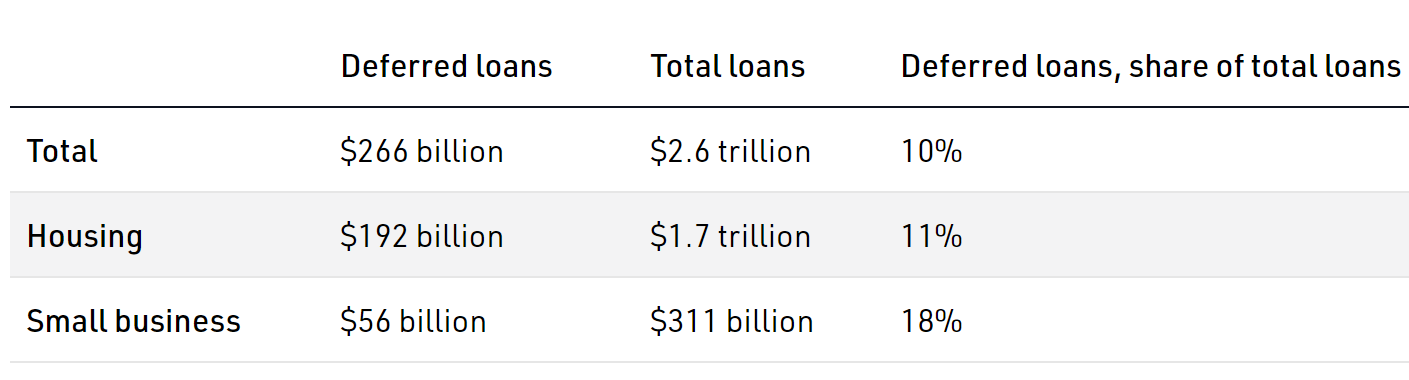

The contrast with the peak of the pandemic cannot be more stark. The table below shows the value and share of deferred mortgages at its peak in May 2020:

At the peak of the pandemic, 11% of mortgages were on a deferred payment plan.

In particular:

- The value of deferred loans has shrunk by 95% since the peak of the COVID-19 pandemic, when there were loans totalling $266 billion on ‘repayment holidays’.

- The value of mortgage deferrals are down 94% from peak when there were $192 billion loans on repayment holidays.

- The share of total loans on deferral has shrunk from 10% in May 2020 to only 0.5% in February 2021.

- The share of total mortgages on deferral has shrunk from 11% in May 2020 to 0.7% in February 2021.

- The total number of mortgages on deferral has fallen from a peak of 488,249 mortgages in May 2020 to only 28,320 mortgages in February 2021.

In short, the ‘mortgage cliff’ that was towering over the housing market last year has vanished into thin air.