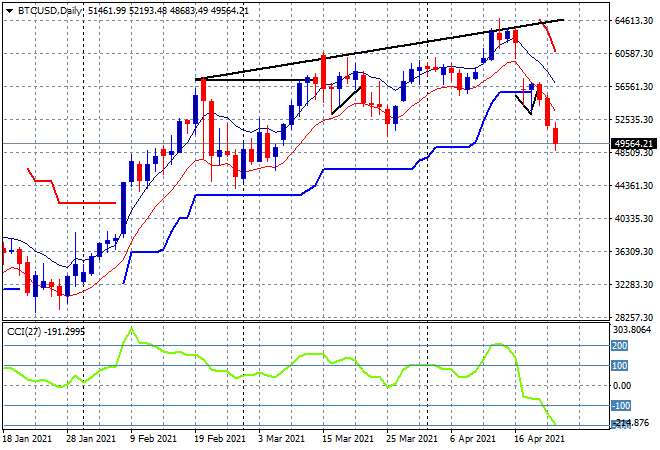

Asia stocks are all over the place, finishing the week on a very mixed note given the wobbly lead from Wall Street all week. USD is weakening again against all the majors after a small rebound overnight but Bitcoin is back below the $50K level for the first time since early March having given up any attempt at support this week following the Turkish ban:

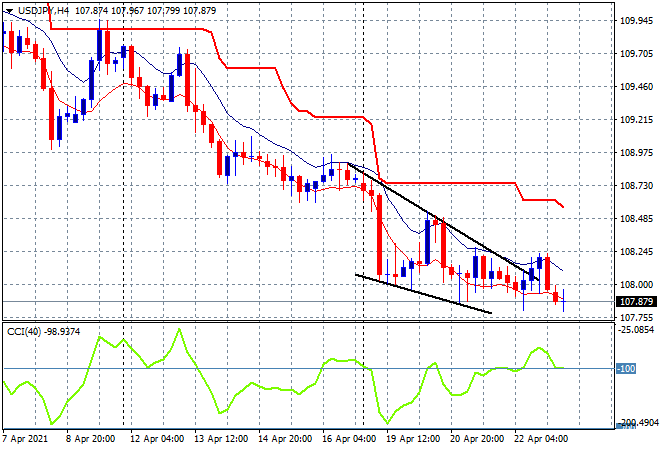

Chinese markets are trying to rebound with the Shanghai Composite edging slightly higher at 3465 points while the Hang Seng Index is doing a lot better, up 0.9% to 29019 points. Japanese markets are in retreat again however, with the Nikkei 225 set to close 0.7% lower at 28991 points while the USDJPY pair continues to drop, staying below the 108 handle proper for a new weekly low:

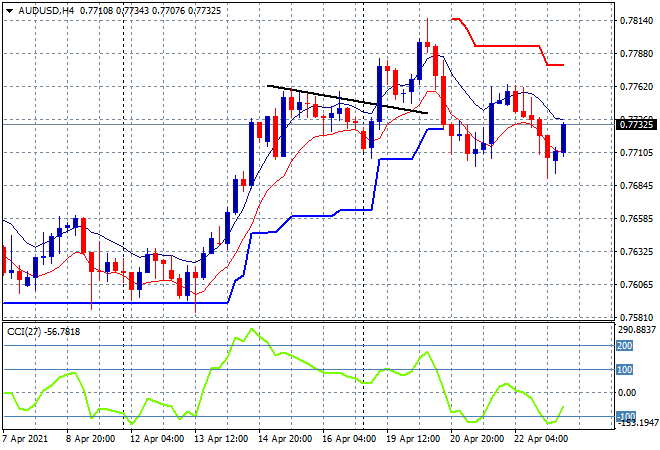

The ASX200 had a mild selloff but has recovered most of it, down only 0.2% going into the close to stay just above the 7000 point barrier, while the Australian dollar is finding more life and stabilising somewhat, bouncing off the 77 handle that has been strong support all week:

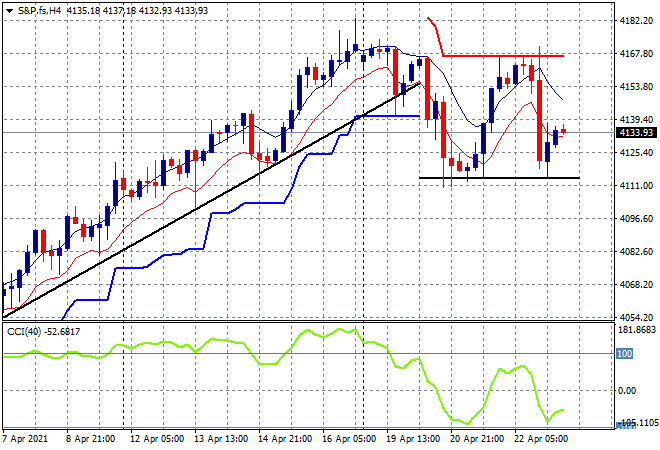

Eurostoxx and S&P futures are barely moving higher, with the four hourly chart of the S&P500 showing a very mild bounce off trailing ATR support at 4130 points so it looks like another consolidation period tonight:

The economic calendar finishes the week with a slew of manufacturing and services flash PMI surveys across Europe and the US plus some new home sales data.