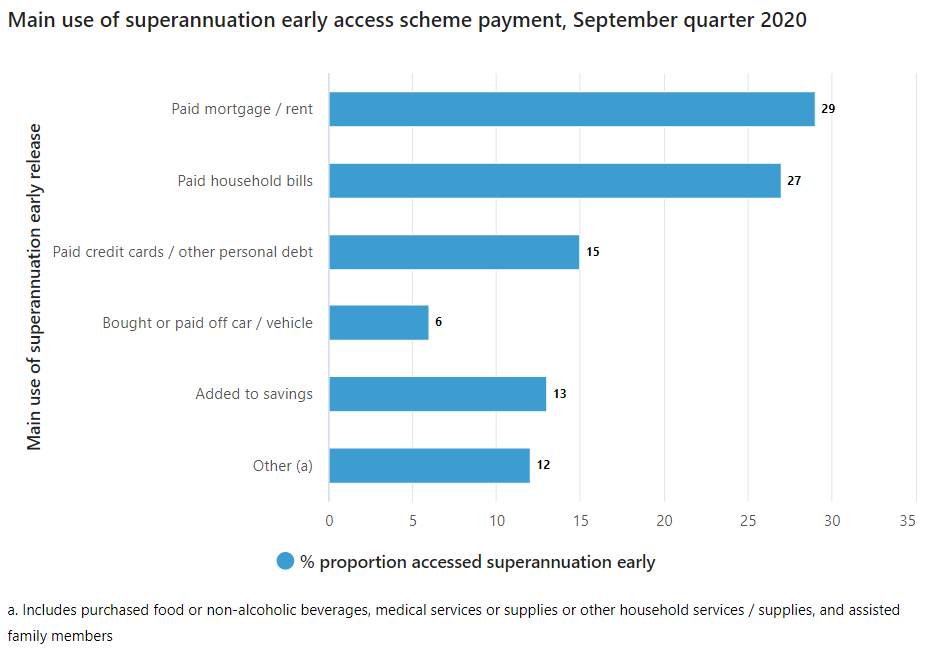

The Morrison Government’s early release of superannuation policy allowed people in financial hardship to withdraw up to $20,000 of their superannuation savings last calendar year.

Sceptics of this scheme claimed the majority of these withdrawals were wasted on things like gambling, alcohol and takeaway food rather than essential household spending.

Today, the Australian Bureau of Statistics (ABS) has released its Household financial resources survey for the September quarter of 2020, which reveals that the majority of early super withdrawals were used for legitimate purposes: