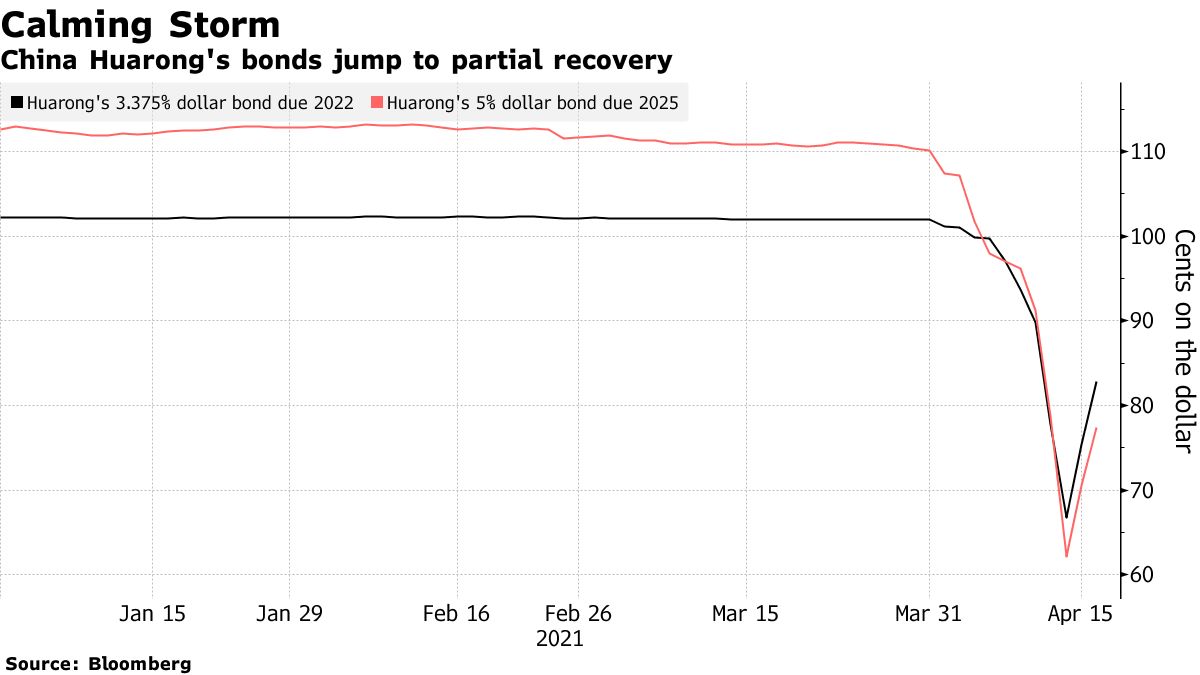

The little China financial crisis we have been tracking shows signs of a little easing as we enter a new week:

- Huarong bonds recovered some ground Friday after the financial regulator declared liquidity plentiful.

- While well short of any guarantee, some analysts expected that this is a turning point for the beleaguered debt manager.

My own view is that that rather misses the point. Huarong is as much a symptom as it is the cause of where the Chinese economy is headed. We need to watch the wider Chinese junk bond market to understand that:

Advertisement