By Gareth Aird, head of Australian economics at CBA:

Key Points

- We expect the headline CPI to increase by 1.1% in Q1 20 (+1.6%/yr).

- The trimmed mean CPI on our forecasts will print at +0.6% (1.3%/yr).

- The inflation debate is expected to heat up over 2021 as the labour market continues to tighten and wages growth is forecast to gradually lift.

Overview

The Australian economic recovery has been swift and the labour market has tightened a lot. There is more to come. Our forecast is for the unemployment rate to continue to fall to 5.0% by end‑2021. Financial markets are now very much focussed on what a tightening labour market means for wages and inflation.

The CPI is a lagging indicator. In general consumer prices will take some time to respond to changes in supply and demand in the economy. But there can be exceptions. Indeed we saw that last year. The big negative economic shock that resulted in a collapse in GDP over Q2 20 was accompanied by a big fall in the CPI. To recall, the CPI fell by 1.9%. Policy played a role, particularly around the provision of free child care.

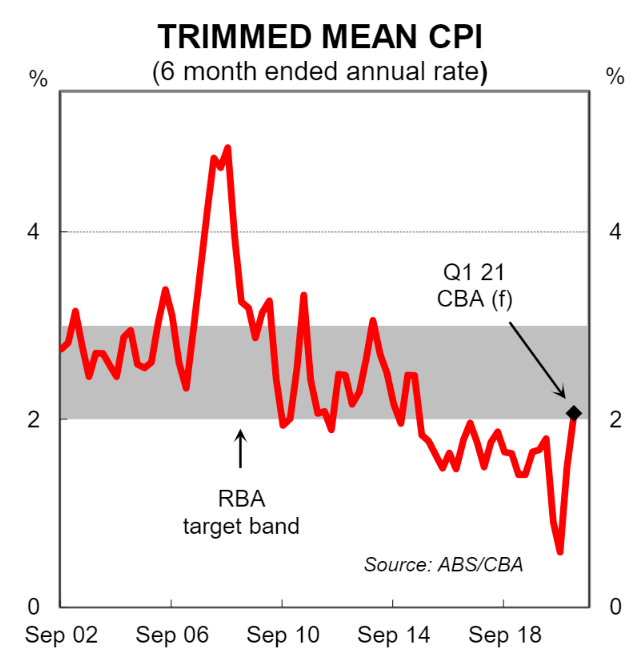

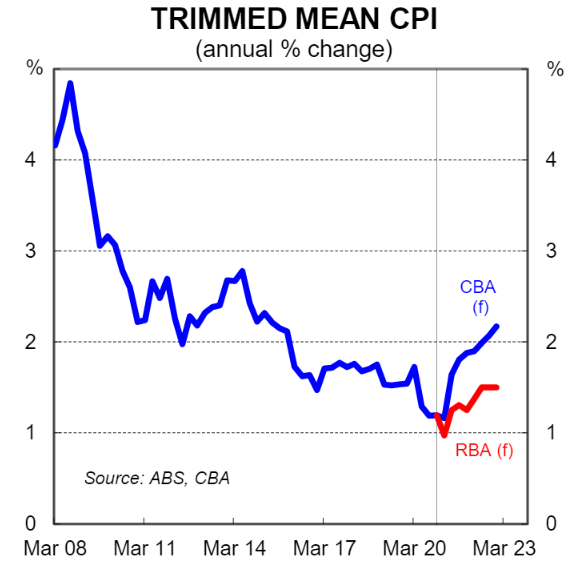

Underlying inflation also slowed quite quickly. The trimmed mean, the RBA’s preferred measure of inflation, was flat over Q2 20. It posted a rise of 0.7% over H2 20 to leave the annual rate at a soft 1.2% at end‑2020.

Headline inflation also picked up over H2 20, but the fall in Q2 20 was so large that the annual rate was just 0.9% at end‑2020. That will change, however. We have good reason to believe that inflation accelerated over Q1 21 and base effects are going to propel headline inflation comfortably above 3% by mid‑21. The RBA will consider that lift to be transitory. But our view is that not all of the lift in inflation will be fleeting. Our expectation is that underlying inflation will be on sustained upward trend over 2021. And we expect core inflation to sit within the RBA’s target band by mid‑2022. This note is a preview of the Q1 21 CPI which we think is shaping up as a particularly interesting one.

The Q1 21 CPI

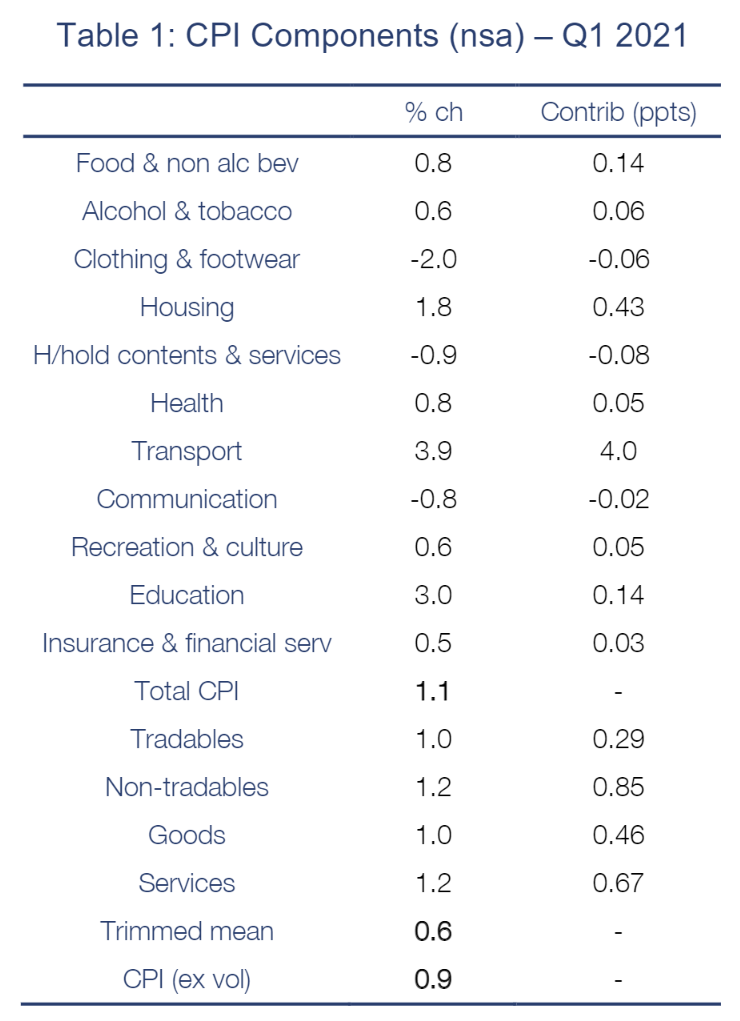

On Wednesday 28 April the ABS will publish the Q1 21 CPI. We expect to see a solid 1.1% increase in headline inflation. The consensus has not yet been formed, but we suspect that our forecast will be on the high side largely because we forecast a strong lift in rents that may not be expected by the street. See Table 1 below for our detailed forecasts for the Q1 21 CPI basket.

The main features of our call are as follows:

- a decent rise in food prices of 0.8% following a sedate 0.2% lift in Q4 20;

- seasonal falls in clothing and a range of consumer durables;

- a big lift in transport driven by a 9.5% increase in petrol prices and an expected solid lift in motor vehicles.

- the usual March quarter lift in education prices which we have pegged at 3.0%;

- a seasonal large increase in pharmaceuticals; and

- a strong 1.8% increase in the housing component driven by rents, utilities and the cost of home building.

Housing matters

The housing component of the CPI is shaping up as both a very interesting and important part of the Q1 21 CPI basket. Indeed it could end up being our point of different with the consensus.

The housing component of the CPI is worth 24% (it was slightly upwardly reweighted in the annual re‑weight). It essentially comprises three components: (i) the cost of building or renovating a home; (ii) rent; and (iii) utilities and other charges. We are expecting strong rises in each of those components.

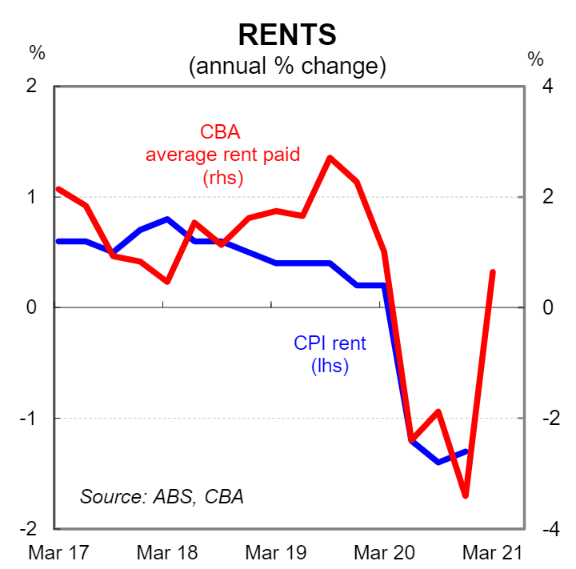

The Government’s HomeBuilder package has been an incredible success and residential investment has surged. This will no doubt be accompanied by an increase in prices due to both a spike in the demand for labour which allows builders to charge more and also a lift in the cost of materials. On rents, our internal data indicates that average rent paid increased sharply over Q1 21. We do not have a long history, but our data looks to be well correlated with the ABS rent series (see chart opposite). The CoreLogic data is sending a similar signal on rents. We forecast that rents rose by 2.0% in Q1 21. And finally we expect a partial rebound in utilities of 2.5% in Q1 21 after the big 4.6% fall in Q4 20 due to some electricity credits.

A reminder – it’s an 8 capital city inflation gauge

The CPI measures quarterly changes in the price of a ‘basket’ of goods and services for metropolitan households. It is based on capital city indexes which measure price changes across each capital city in Australia individually. It does not include price changes in regional Australia. In ‘normal’ times this does not matter much. But we suspect that price rises in regional Australia have been stronger than in the capital cities at an aggregate level due to the relative strength of spending, employment and housing that we have captured largely in our internal data.

Underlying inflation

Underlying inflation is expected to lift. Our forecast is for the trimmed mean, the RBA’s preferred measure, to rise by 0.6% over the quarter. Such an outcome would see the annual pace of core inflation lift to 1.3%. The six month annualised pace of underlying inflation on our figuring accelerates to 2.1%.

Inflation and the RBA

The RBA has forecast the trimmed mean to be 1¼%/y at Q2 21 which implies quarterly growth rates of 0.3% over both the March and June quarters. As such, if the CPI prints in line with our call that will be a big upside surprise compared to the RBA forecasts. It would mean that the RBA should make a decent upward revision to their near term inflation forecast profile in the May Statement on Monetary Policy (SMP). Indeed they will need to make material revisions to their economic forecasts more generally given the strength of the recent data, particularly around the labour market.

That all said, the RBA’s recent forecasting history suggests that even with an upside inflation surprise in Q1 21 relative to their expectations they will continue to produce a conservative set of numbers. We suspect they will do there upmost best to produce a profile that has below target inflation over their forecast horizon (to mid‑2023). It is, after all, largely required if they are to stick with their 2024 forward guidance on the cash rate.