The Australian dollar tumbled again last night as risk took another hit. We can expect this rising volatility to continue to post-COVID policy changes take their poll. DXY was firm as the safe-haven bid returned:

The Australian dollar is still wrestling with a huge head and shoulders topping pattern versus DXY and is sliding against other DM majors:

Oil was firm, gold fell:

Base metals softened:

Big miners too:

EM stocks are going nowhere fast:

Junk is stable which illustrates much of this day-to-day risk volatility is ephemeral:

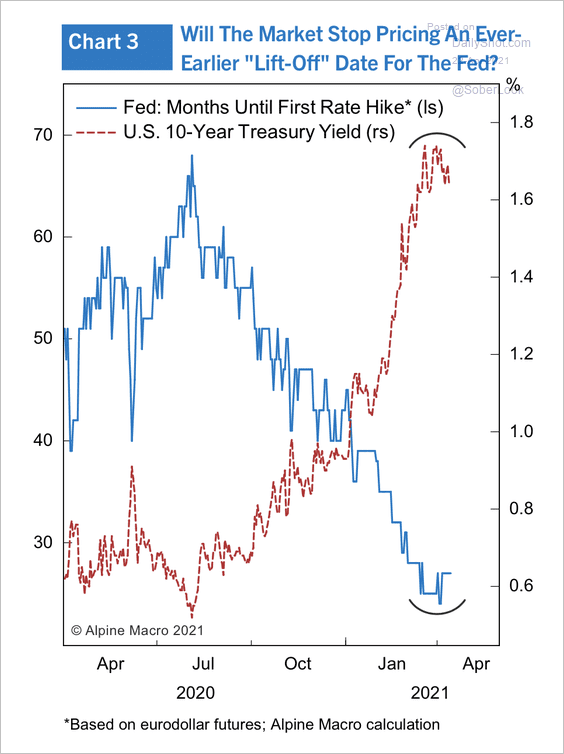

US yields fell some more:

Which did not help stocks:

Westpac has the data wrap:

Event Wrap

Media reported that US President Biden will propose a doubling of the capital gains tax rate for wealthy individuals to 39.6%, to help pay for social spending initiatives that address inequality.

US initial jobless claims rose 547k (vs estimate 610k, prior revised to 586k from 576k), with continuing claims of 3.674m (est. 3.6mn prior revised to 3.708m from 3.732m). The CB leading index rose 1.3% in March (vs est. +1.0%), employment driving the gain. Existing home sales in March slipped to 6.01m (vs. est. 6.11m, prior 6.24m). Chicago Fed activity survey index in March rose to 1.71 (est. 1.25) from a revised -1.20 (from -1.09), the rebound in growth led by consumption, housing, production, and employment. The Kansas Fed April survey also rose, the index up to 31 (est. 28, from prior 26, and 24 in Feb), driven by durable goods and transportation equipment, with record levels of employment and production.

The ECB left its policy settings unchanged, as was universally expected, and reiterated its intent to increase the pace of PEPP bond buying through the current quarter but then slow the pace later this year. An acknowledgement of improving global demand was tempered with concern over the persisting pandemic and associated downside risks. Inflation is seen as rising temporarily; with spare capacity, low wage growth and EUR appreciation capping medium term inflation. Accommodation is to remain in place with similar forward guidance to previous meetings. In response to questions Lagarde did say that talk of slowing PEPP was premature, and that is dependent upon economic developments, while noting the effectiveness of negative interest rates.

Event Outlook

Europe: April Markit manufacturing and services PMIs will be released for the Euro Area and the UK.

UK: GFK consumer sentiment has lifted off its pandemic lows and is expected to improve to -12 in April. March retail sales should advance 1.5%, with further strength ahead as lockdowns unwind and pent-up demand drives spending. March public sector net borrowing is set to rise to GBP 21.3bn on the record peacetime deficit.

US: Both the April Markit services (market f/c: 61.5) and manufacturing (market f/c: 61.0) PMIs will point to the brisk pace of the US’ economic recovery. March new home sales should see some catch up after a weather disrupted February (market f/c: 14.2%).

The mooted capital gains hike is being reported as the trigger for the selling. Perhaps. My main counter-point is that because valuations are so high, this is an inherently febrile market, so sorting signals from noise becomes much more difficult. As such, expect more volatility.

As for forex, Bloomie is reporting NAB bulls:

- Ray Attrill says the AUD is will reach 85 cents in 2022.

- Commodity prices will remain firm.

- DXY will fall as US exceptionalism passes.

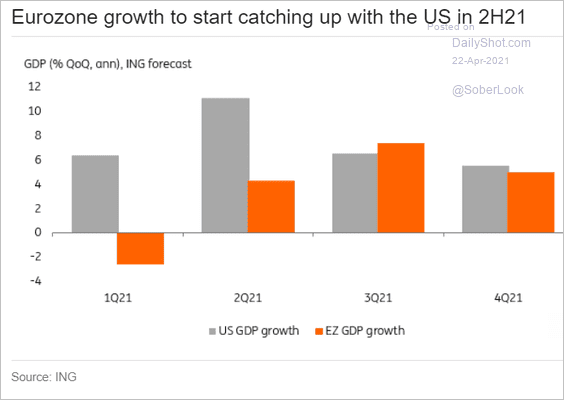

I see this as a risk case. Undoubtedly, US growth exceptionalism will ease as more of the world opens up. Europe being the most important catcher-uperer:

But are we seeing this priced now? This cycle has been non-stop acceleration through market factors. Ahead in the US is more major inflation spike followed by a large drop in H2 then re-acceleration in 2022. It is a much higher inflation profile than Europe, notwithstanding recovery:

Which is why some markets are so hawkish on the US:

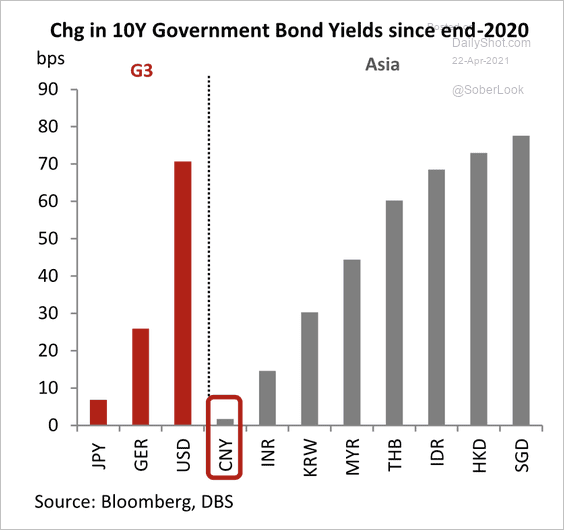

However, the forex race is also on between an accelerating Europe and a slowing China. The latter is already registering it in yield spreads, registering the slowest rise anywhere:

And there is more ahead as credit slows fast:

As I have said in recent days, the pace and volatility of recent market factors has made it very difficult to sort short-term signal from noise. I can certainly see a scenario in which a recovering Europe sinks DXY another leg. But it’s entirely plausible as well that the Chinese slowing hits with sufficient force to throw that completely off track for the AUD.

So, for me, the play right now is to dollar average into offshore assets during bouts of AUD strength. By next year, as catch-up growth and stimulus settle into more predictable trend patterns, China and Europe will both slow materially and US fiscal-led growth and inflation exceptionalism will be the only game in town.