The Australia Institute (TAI) has released a new study arguing that Australia’s compulsory superannuation system is worsening the gender gap:

[Australian] men get 72 per cent of the $41 billion per year in superannuation tax concessions.

Taxation statistics show that the average (mean) superannuation balance at the end of 2017-18 was $153,300 for males and $120,200 for females.5 This represents a 27.5 per cent difference in favour of males…

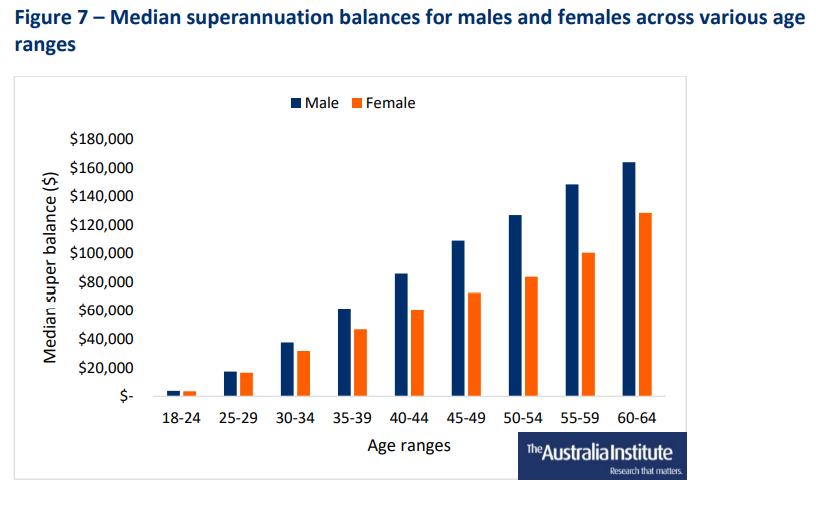

The average is susceptible to bias due to the occasional very high incomes that might be included. But looking at the median figures the advantage in favour of males is even worse. Figure 7 shows the median superannuation balances for males and females across various age ranges.

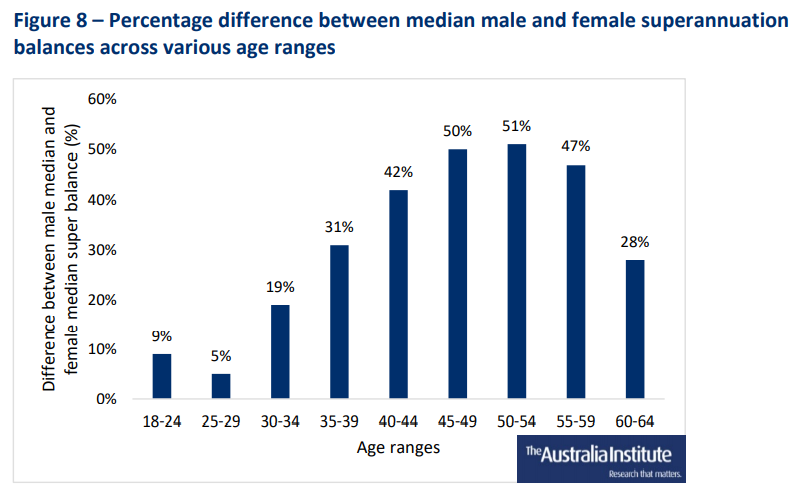

When we look at the differences between median superannuation balances for male and female, we find that men have much higher balances. For 35- to 39-year-old males the median super balance exceeds the female median by 31 per cent and peaks at a 51 per cent male advantage for the 50-to-54-year age group. Figure 8 shows the percentage difference between the median male and female superannuation balances for various age ranges…

The statistical evidence reveals large gender inequalities in the superannuation system. It is worth also pointing out that superannuation in Australia is heavily subsidised through tax concessions, especially concessions on workers’ incomes in the form of super contributions as well as concessions on the earnings of super funds. Together those two tax concessions are estimated to be worth $39 billion in 2019-20…

The reason why women accumulate less superannuation than men is obvious.

The entire system has been set up so that the longer somebody works, and the more they get paid, the bigger the superannuation balances they retire with:

Advertisement

Superannuation concessions are skewed to high income earners.

This leads to men accumulating larger superannuation balances, despite not living for as long.

Lifting the compulsory superannuation guarantee (SG) to 12% will obviously worsen the retirement gap between men and women, while also costing taxpayers an extra $2 billion in tax concessions every year.

Advertisement

Rather than lifting the SG, scarce taxpayer funds should instead be used to lift the Aged Pension, which is Australia’s genuine retirement pillar.

Unlike superannuation, the Aged Pension does not discriminate by gender. It does not discriminate on how long somebody spends in paid work or how much they earn. And because the Aged Pension is means tested, it is generally targeted towards those that need it most (with the exception of asset rich home owning retirees).

Sadly, the Morrison Government has caved-in to the superannuation industry and Labor and will procced with lifting the SG to 12%. This will increase superannuation’s budgetary cost and make it more difficult to lift the Aged Pension, while also lowering wage growth and increasing inequality (including gender equality).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.