The Reserve Bank of Australia (RBA) has released its private sector credit aggregates data for the month of March.

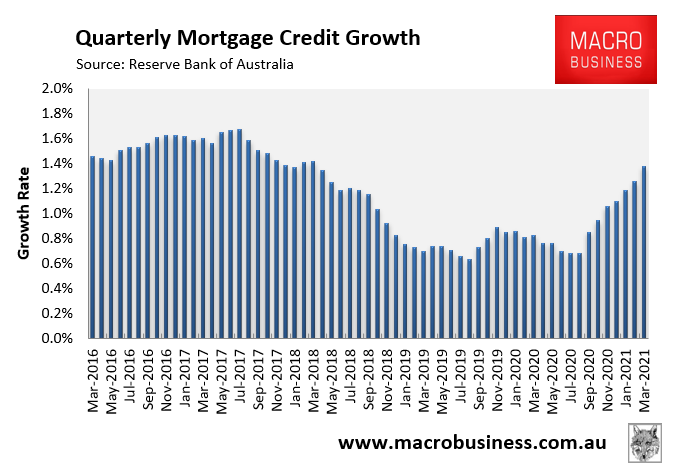

Quarterly mortgage credit growth continued to firm, rising for the 8th consecutive month to 1.4% – the highest rate of growth since March 2018:

Quarterly mortgage growth is accelerating alongside dwelling values.

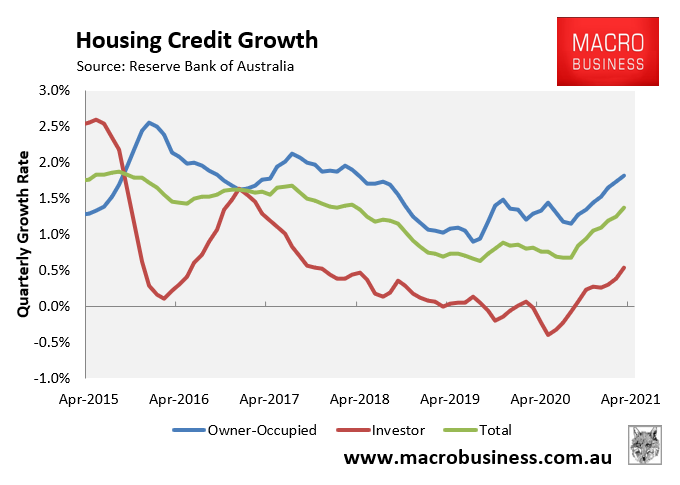

Owner-occupiers continue to drive mortgage growth, rising by 1.8% over the quarter versus only 0.5% growth for investors:

Owner-occupiers continue to drive mortgage growth.

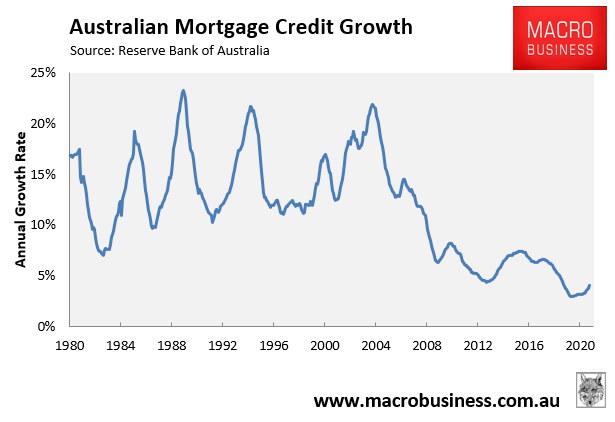

Meanwhile, annual mortgage growth continues to rise from record low levels. It rose to 4.1% in the year to March 2021 – the highest level since February 2019:

Annual mortgage growth continues to rebound from record lows.

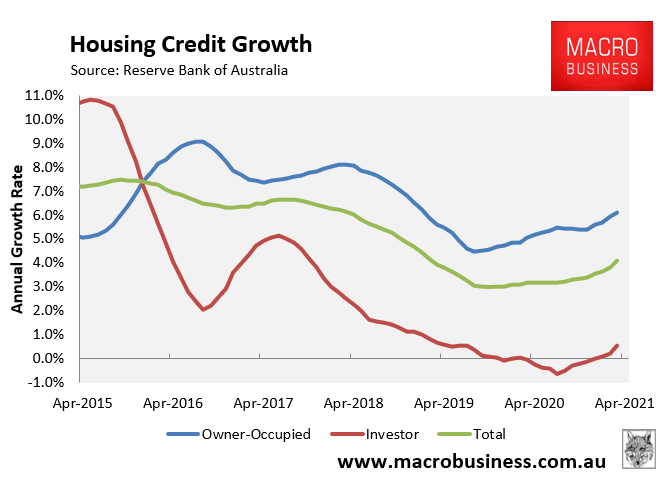

Again, this growth is being driven by owner-occupiers, whose annual mortgage growth was 6.1% in the year to March 2021, versus only 0.55% growth in investor mortgages:

Owner-occupied mortgage growth strong, investor mortgage growth weak.

The acceleration in mortgage growth is obviously far slower than the acceleration in new mortgage commitments. This is because existing mortgage holders are taking advantage of record low interest rates to repay debt, which is mostly offsetting new mortgage demand.