DXY is back to its falling regime after the US inflation print. EUR was strong. The Australian dollar is off to the races while this dynamic runs. DXY:

The Australian dollar took off against all DMs:

Gold was weak as oil rallied:

Base metals too:

And big miners:

EM stocks sat it out in hospital with COVID after dropping a Chinese vaccine that doesn’t work:

US yields rebounded:

Stocks lifted value and sold growth:

Westpac has the data wrap:

Event Wrap

The Fed’s Beige Book of regional economic conditions said that activity had accelerated to a “moderate pace” between late February and early April. Consumer spending increased; manufacturing activity expanded further, even with supply chain disruptions; and there was an increase in tourism, helped by stronger demand for leisure activities and travel. There was a slight acceleration in prices with “many Districts reporting moderate price increases and some saying prices rose more robustly. Input prices rose across the board, but especially in manufacturing, construction, retail, and transportation.”

Fed Chair Powell stressed the importance of fiscal policy with respect to the pandemic as well as stating that current debt levels are serviceable and sustainable even though a long-run deficit path is unsustainable. He also underscored that the Fed does not currently see rates rising until 2024, while unemployment can go lower without triggering inflation as the economy recovers at a fast pace.

Eurozone industrial production in February was less weak than expected at -1.0%m/m (est. -1.3%m/m), but still reflects the negative impact of the prolonged Covid restrictions in the region. Declines were led by durables and capital goods (-1.9%m/m).

Event Outlook

Australia: The March ABS labour force survey will be released. Leading indictors of employment, such as weekly payrolls, job vacancies and the various business surveys all suggest labour demand continued to strengthen through March and into April. Westpac expects an employment gain of +32k (market 35k), but there are upside risks to this forecast. Rising participation is muting the improvement in unemployment. A 0.1ppt increase in participation to 66.2% will hold the unemployment rate at 5.8%. Meanwhile, April MI inflation expectations will be supported by rising fuel costs.

New Zealand: The food price index should advance 0.8% in March, but prices have eased since Covid disruptions in mid-2020.

US: Initial jobless claims have been choppy of late, but the downtrend remains in place (market f/c: 700k). March retail sales (market f/c: 5.8%) and industrial production (market f/c: 2.5%) are both expected to lift following softer prints last month due to weather disruptions. Two regional Fed surveys, the Empire State index (market f/c: 19.2) and the Philly Fed index (market f/c: 40.9), should continue to reveal strong growth in pricing power, input costs, and new orders. Meanwhile, February business inventories will continue to accumulate as the economy recovers (market f/c: 0.5%). The NAHB housing market index has eased off its record high in November, but remains historically elevated (market f/c: 84.0). February net TIC flows are also due, following a rise in January on increased net holdings in China and Japan. Finally, Fed Vice Chair Clarida, and the FOMC’s Bostic, Daly, and Mester will speak.

Last night we saw all of the usual effects from a falling DXY with the exception of the equities action. For the time being this counter-trend rally wants to run. US inflation worries are off the table for a bit and EUR is unleashed as it approaches a growth rebound. How far it gets is anybody’s guess.

For me, it changes little. The key dynamic for the cycle ahead is the US growth in the driver’s seat and China in the caboose. Europe is, as usual, a spectactor:

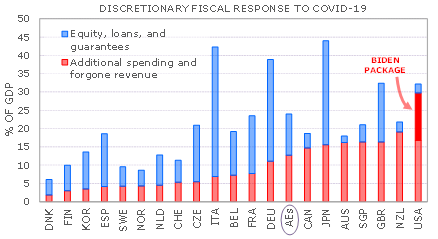

That’s 30% of GDP fiscal stimulus. The US is still 25% of global GDP. (Investors should never use PPP-based GDP aggregates. We live in a world of dollars and cents.)

So US stimulus is going to be ~7½% of global GDP.

Meanwhile, China is using this largesse to tighten fast and restructure away from commodity-intensive growth.

JPM captures my thoughts today:

The RBNZ played out almost exactly as expected overnight, with more reinforcement of the easing bias, concern over the data and the “dampening effect” of new macro pru measures on the housing market. However, the bird took little notice and in actual fact traded stronger vs AUD. Normally at this point I would point to the fact that the market reaction was out of line with the news because of market expectations, but with the market pricing in almost a full 25bphike in the next 12 months, that doesn’t seem like a satisfactory explanation. More likely, the market got itself a bit short NZD heading into the meeting on the housing news and we certainly have seen some selling, which to be honest I had thought was more unwinds of longs. The bigger factor at play here is the weak USD, and in particular, strong Euro, a theme which has been manifesting itself over the past couple of weeks and something we are increasingly more involved with. On that point, it’s worth noting that the steady RMUSD buying that we saw throughout Q1 topped out at quarter end and that community has been steady sellers of USDswith us since. I’m expecting the antipodes to underperform the bounce in growth, mobility and in turn, currency strength in Q2 and continue to run basket shorts vs EUR, GBP, CAD, NOK, SEK. Intraday moves in the portfolio can be painful, as we have seen a pretty high beta bounce in the antipodes overnight, but the rally to the 77c and 71c areas in AUDUSD and NZDUSD present opportunities to add to basket shorts.