As much of the MSM celebrates China’s post-COVID economic recovery, mistaking short-term catch-up growth for something more sustainable, MB has been arguing quite the opposite. China is going to slow relatively quickly as it returns to its program of economic restructuring and away from wasteful construction sectors. Today, Capital Economics agrees:

With the growth trajectories of China and the US likely to continue to diverge as the year goes on, we doubt the renminbi’s recent rebound against the US dollar will continue.

Data released over the past couple of days suggest an increasing contrast in the directions of the US and Chinese economies. In the US, a massive increase in retail sales capped a string of strong data, from inflation to payrolls. Meanwhile, despite a record annual figure, China’s GDP growth slowed sharply in q/q terms in the first quarter. Subscribers can read all the detail on our dedicated US and China economics services.

The big picture, though, is that we think these data reflect a divergence between the two economies that will continue over at least the next couple of years. In the US, we expect rapid growth thanks to the economy reopening and large fiscal stimulus. By contrast, China’s economic recovery from the virus is now largely in the rear-view mirror, in our view; we expect growth there to be much lower than it has been over the past year as the economy returns toward its pre-virus trend, policy support is withdrawn, and the pandemic-related boost to the country’s exports fades.

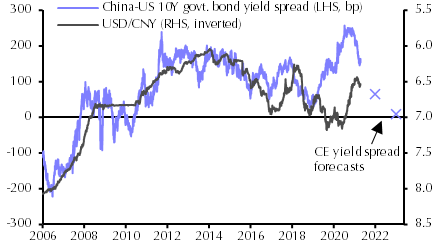

It is perhaps surprising, given all this economic news, that the renminbi has strengthened against the US dollar this month. We suspect this is largely a result of the recent decline in long-term US yields; despite the good US economic data, the 10-year Treasury yield, for example, has declined by ~15bp since the end of March. At the same time, despite some ructions in the country’s corporate bond market, the 10-year Chinese government bond yield has changed little. This has resulted in a larger 10-year China-US government bond yield spread.

Nonetheless, we expect the divergent economic outlooks to eventually pull China’s currency back down, for two reasons.

First, we think the spread between the two countries’ long-term bond yields will begin to narrow again before too long. (See Chart 1) We suspect the 10-year US Treasury yield has only paused on its climb higher, and that it has scope to increase quite a bit more as the rapid US economic recovery continues and the Fed doesn’t stand in the way. (See here.) At the same time, we think the 10-year government bond yield in China may decline over the next couple of years, as growth there slows and investors factor in the next monetary policy easing cycle.

The result is that we think the spread between 10-year government bond yields in China and the US could still narrow quite significantly from here; we forecast it to be almost zero by end-2022, compared with ~160bp currently.

The second factor we think will hold back the renminbi is the eventual narrowing of China’s massive current account surplus – which probably boosted the currency last year – as the global economy continues to return to normal. Even though strong growth in the US, and elsewhere, is likely to support China’s exports, we doubt this will prove sufficient to offset the decline in pandemic-related demand for IT and healthcare goods.

As a result of all this, we expect the recent strength in the renminbi to prove short-lived: we forecast it to finish 2022 at 6.9/$, compared with ~6.5 at present.

I agree with this conclusion. As China uses fiscal allocations and reform, plus allows bond market tightening to trigger defaults, we are going to see falling commodity prices and Chinese factory gate inflation before very long.

Those looking for PBOC rate hikes are wrong. We’re unlikely see cash rate cuts but falling growth and returning disinflation will still stink benchmark yields.

Advertisement

The result will be a falling CNY and when that happens there are a series of corollaries:

The emerging markets bid is hurt by rising Chinese competitiveness.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.