DXY was soft again last night as a strong EUR took down DXY:

The Australian dollar did better against all DMS:

Gold is convinced of further DXY weakness ahead. Oil not so much:

Copper looks ready to break out:

Miners firmed:

EM stocks still look buggered:

Junk is fine:

US yields faded some more, throwing fuel on the risk rally fire:

And lifting stocks:

Westpac has the data wrap:

Event Wrap

Bank of Canada left its policy rate unchanged at 0.25% and, as was widely expected, reduced its bond purchase pace from CAD4bn per week to CAD3bn.

Its economic outlook improved, reflecting a recent strong run of data, although fresh Covid outbreaks warranted mention. The GDP forecast for 2021 was increased to 6.5% from 4.0%, the 2021 inflation forecast to 2.3% from 1.6%, while 2022 inflation was increased to 1.9% from 1.7%. The output gap was expected to close in H2 2022 (previously 2023), and the pace of economic recovery would dictate any further adjustments to the pace of QE.Canada’s headline CPI in March was a tad softer than anticipated at +0.5%m/m and +2.2%y/y (est. +0.6%m/m and +2/3%y/y), but core CPI was firmer, the trimmed measure at +2.2%y/y (est. +2.0%y/y).

UK inflation data was also slightly more subdued than expected, with headline CPI at +0.3%m/m and +0.7%y/y vs. (+0.4%m/m and +0.8%y/y). while core CPI was in line at +1.1%y/y,

Event Outlook

Australia: Ahead of the Q1 NAB business survey, the March monthly measure had reported conditions at a record high.

Euro Area: The ECB will announce its monetary policy decision. The Council will restate their commitment to accommodative conditions and will acknowledge that any imminent lift in inflation will be temporary (and be treated accordingly in a policy context). There will be some cause for cautious optimism around the coming quarters, despite extended lockdowns delaying the reopening rebound. April consumer confidence will continue to be constrained by the lockdowns and slow vaccine rollout (market f/c: -11).

US: The Chicago Fed activity index dipped below zero in March, but is poised for a stronger print in April (market f/c: 1.25%). Initial jobless claims hit a pandemic low last week and the broad downtrend is expected continue. The March leading index will be supported by jobless claims, stock prices and the ISM survey (market f/c: 1.00%). March existing home sales are expected to decline 1.1% on tight supply and elevated prices. The Kansas City Fed index should keep pace with the strength seen in other manufacturing surveys (market f/c: 28).

Broader dynamics are unchanged. The US is still leading the vaccine growth, inflation and yields race but, for now, markets are happy that it is priced so are counter-trending with EUR leading.

It can continue for a while as Europe steadily gets its vaccines in order and reopens. The higher EUR is going to prevent the kind of inflation spikes we’ll be seeing in the US but the growth rebound will be strong. That will support the AUD while it lasts.

At least while we await this to come to bear. Tightening Chinese credit:

Which does nothing good for commodity prices that have, arguably, massively overshot:

And it ends EUR bullishness to boot:

Use further strength in the AUD to move your assets offshore.

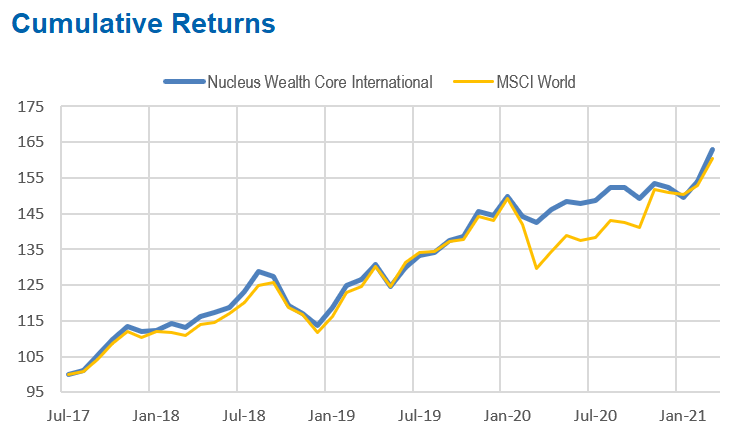

David Llewellyn-Smith is Chief Strategist at the MB Fund and Nucleus Wealth. The MB Fund/Nucleus Wealth Core International fund is one way to get quality international equities exposure. The fund has outperformed the MSCI World index for four years with consistently lower volatility:

If you are interested in knowing more about the fund then contact us below: