The Australian dollar was weak overnight despite a powerful relief rally for anything and everything that has been recently squashed by rising US yields and greenback. DXY eased as EUR rose:

The Australian dollar could not catch a bid and still sits right on the neckline of its head-and-shoulders topping pattern:

Gold did better and has a possible double bottom in place. The oil chart does not look well:

Base metals enjoyed a weaker DXY:

Big miners were more mixed:

EM stocks still look dangerously poised but did lift:

Junk is absolutely fine leaving the Fed on the sidelines:

US yields climbed:

Stocks reversed recent trends with a powerful relief rally in growth. The wider market still looks strong:

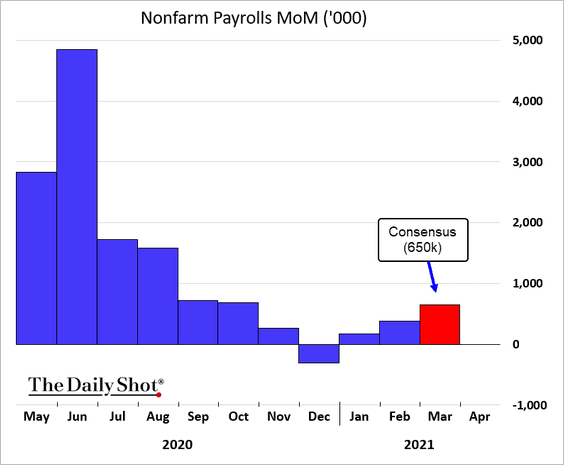

DXY took a breather but it is only that, in my view. Ahead is a booming US jobs market. If not tomorrow then over the next six months:

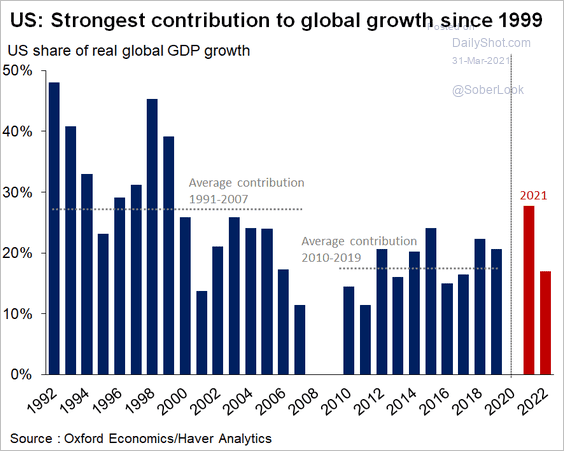

As American GDP booms back at a pace unseen in twenty years:

Leaving the world eating its dust:

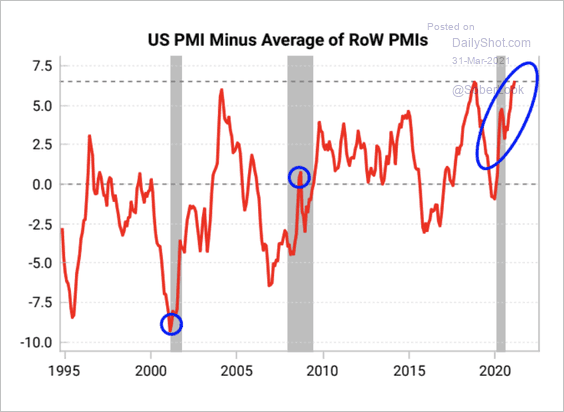

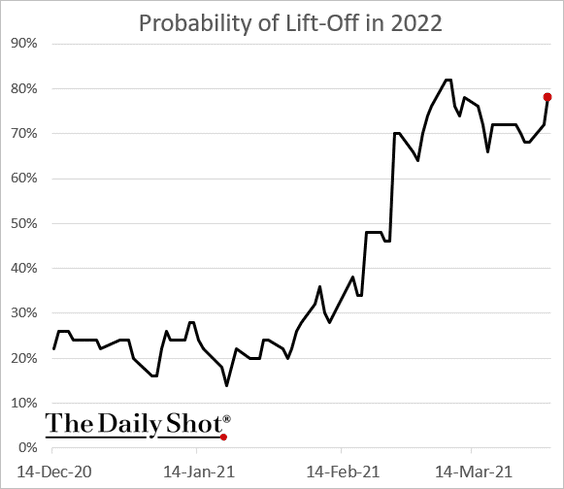

This is leading markets to fight the Fed:

This is leading markets to fight the Fed:

Thanks to the tailing Biden fiscal gale. Though it’s was more moderate than I had hoped:

- $2.2tr over ten years but mostly over eight.

- Roughly halved between hard and human infrastructure.

It is almost all new spending and will add 1%+ to GDP per annum for the life of the Democratic White House assuming it wins a second term.

US growth exceptionalism is assured as Europe does too little fiscal, China returns to restructuring and EMs get crushed between them.

No change for me. AUD, EMs, commodities and growth stocks to keep taking the heat.