DXY took a hit for the global team last night as US inflation printed high but nowhere near high enough on core measures to upset the market applecart. EUR jumped:

The Australian dollar was firm against DXY but weak elsewhere. This was not a sudden shift to bullishness:

Brent firmed with gold:

Base metals were mixed:

Big miners firmed:

EM stocks held on:

Junk was fine:

US yields laughed at the CPI:

And stocks partied led by growth:

Westpac has the data:

Event Wrap

US CPI in March was slightly stronger than analysts’ expectations. The headline measure rose 0.6%m/m and 2.6%y/y (vs median expectation +0.5%m/m and +2.5%y/y), the ex-food and energy measure +0.3%m/m and +1.6%y/y (vs +0.2%m/m and +1.5%y/y), underscoring that energy costs represented about 50% of the headline rise. The NFIB small business optimism survey rose further to 98.2 (vs. est. 98.5, prior 95.8), amid vaccine rollout progress.

The CDC and the FDA said in a joint statement that it is recommending a pause in the use of the Johnson & Johnson vaccine due to blood-clot complications.

Germany’s ZEW economic survey fell to 70.7 (est. 79.0, prior 76.6), still leaving expectations at high historical levels. The same occurred in the survey’s expectations for the Eurozone, pulling back to a still strong 66.3 (prior 74.0). Offsetting the pullbacks in expectations were gains in current conditions, for Germany to -48.8 from -61.0 (est. -54.1), and for the Eurozone to -65.5 (prior -69.8).

UK production data in Feb. was overall firmer than expectations. Industrial production rose 1.0%m/m (est. +0.5%m/m) but services activity rose a mere 0.2%m/m (est. +0.6%m/m). Construction was firm (+1.6%m/m, est. +0.5%m/m) but from a softer starting point. GDP for rose 0.4%m/m to -1.6% 3m/3m (est. +0.5%m/m and -1.9% 3m/3m), the details indicating a firmer underlying production base in the UK.

Event Outlook

Australia: The April update of the Westpac-MI Consumer Sentiment Index will be released. Developments over the last month have been less upbeat, with yet another state ‘mini-lockdown’, this time in Brisbane, highlighting that sudden virus-related disruptions are still a risk. Australia’s vaccine rollout is also running well behind schedule and struck a major problem late in the week when AstraZeneca advised against vaccinating those aged under 50 due to risks of rare but serious side-effects. News around the economy has been more positive – a strong Feb labour force report in particular – but there remains unease about impacts from the expiring JobKeeper scheme. Surging house prices may also be a factor for sentiment although this is often a ‘wedge’ issue for consumers due to affordability and sustainability concerns.

NZ: We expect no change in monetary policy settings at the upcoming RBNZ Monetary Policy Review, with the OCR to be held at 0.25% for the foreseeable future. A softer than expected starting point for the New Zealand economy will be balanced against a rapidly improving global outlook. The RBNZ is already braced for a near-term spike in inflation. However, this is expected to be temporary, and the RBNZ will reiterate that a sustained return to its inflation and employment goals is a considerable time away. February net migration will remain very low due to border closures.

Euro Area: Industrial production is expected to contract 1.2% in February, as rising case counts impede output.

US: Ahead of the March update, the import price index has been rising on stronger fuel prices. Following this, attention will turn to the Federal Reserve: the Beige Book will give an update on conditions across the Fed Districts, and Chair Powell will be speaking to the Economic Club of Washington. Vice Chair Clarida, Williams, and Bostic will also be speaking.

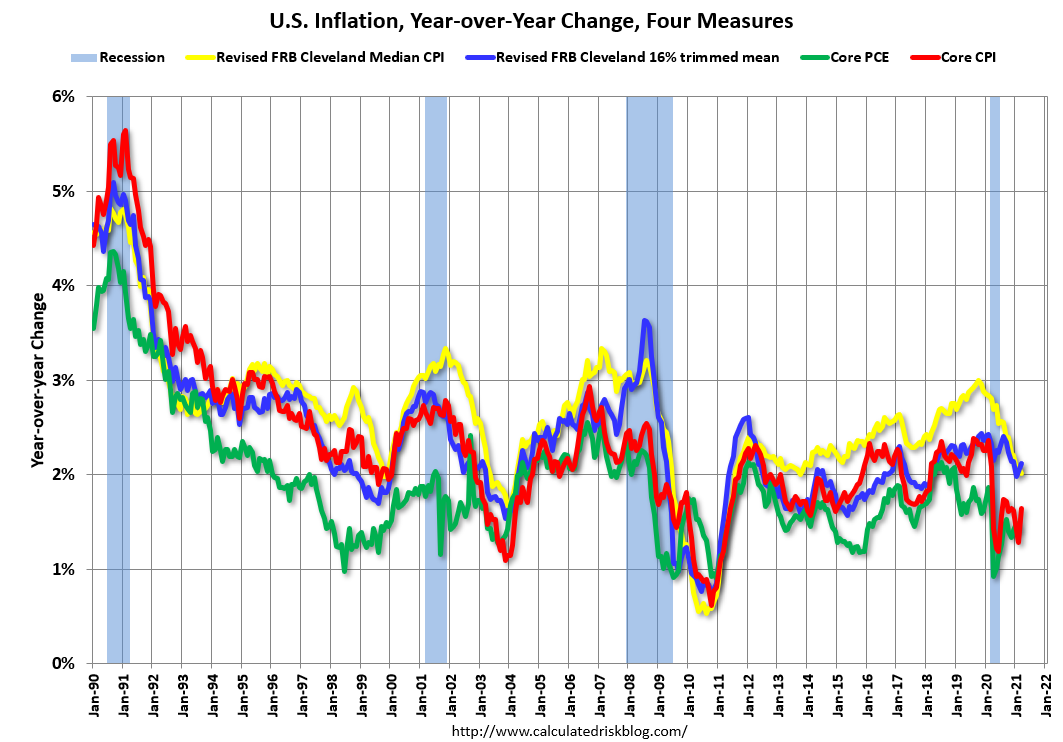

Headline CPI blasted off as expected:

But the Fed’s preferred Core PCE is still at 1.4% and going nowhere fast:

The market is well discounted for the numbers and bonds bid, DXY fell, commodities and growth led equities so on, and so forth. This was all Australian dollar bullish though, if anything, it underdid the jump.

We’ve got another three months of hot CPI data coming out of the US but judging by today’s market reaction it is no longer in any mood to fight the Fed. We may need to wait until deeper in 2022 when the Biden infrastructure stimulus goes to work amid a tightening labour market before the bond back-up gets more serious again.

Given the slowing underway in Chinese credit and serious delays in Europen vaccinations, I don’t see the need to flip my weaker AUD trend call, and will use any intermittent rises to buy more offshore assets.