APRA clears air after tiny Tim’s super for homes brain fart

If there’s one thing that most economists seem to agree on it is that Liberal MP Tim Wilson’s plan to allow first home buyers (FHBs) to access their superannuation savings to purchase a home is an unambiguously bad idea.

Over the past several weeks, we’ve seen economists from all walks of life oppose the plan, arguing that it would merely pour more fuel on the housing bonfire, drive up prices, and reduce affordability, while at the same time torching retirement savings.

Earlier this week, the Australian Prudential Regulatory Authority’s (APRA) chairman Wayne Byres gave testimony to a parliamentary committee where he too warned that Tim Wilson’s proposal would force up property prices:

“We are obviously in the current environment keen to avoid things that lead to further escalation in housing prices”…

“You would have to think it would add to the demand.”

“All else equal it is likely to push them [prices] up.”

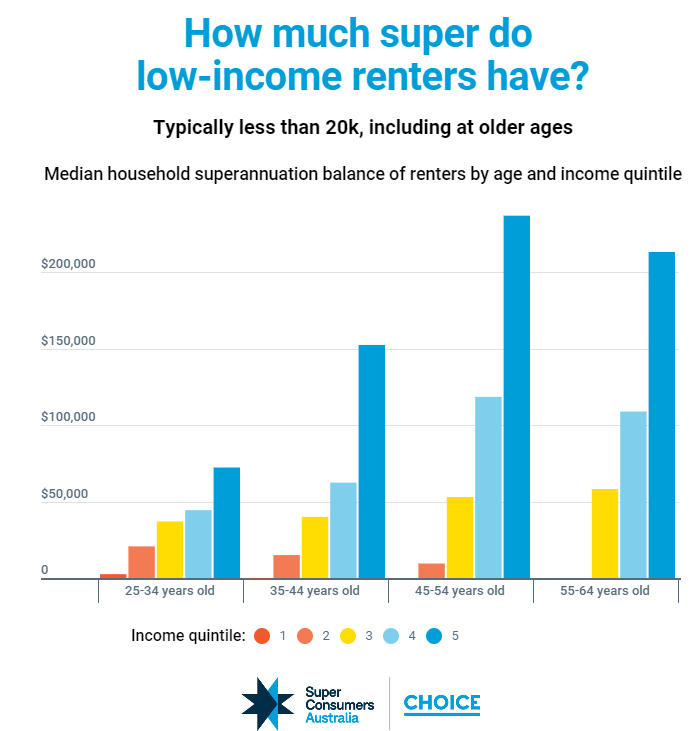

For mine, the most damning assessment came from consumer advocate Choice, which showed that Tim Wilson’s policy would overwhelming benefit higher income FHBs with larger superannuation savings, while disadvantaging lower income FHBs with minimal savings:

Young low-income renters have minimal superannuation savings.

As noted by Kate Colvin, spokesperson for national housing campaign Everybody’s Home:

“Paradoxically, allowing people to use their super for housing would increase the purchasing power of people who have a high income, and so have a relatively high super balance, exactly the group who are already most able to buy.

“Giving this group access to faster capital will push up prices across the board, making it harder for the people who were already struggling to get a foothold in the market.”

Thus, Tim Wilson’s policy would merely entrench current housing inequities, while lowering overall retirement savings.

A cynic could rightfully argue that Tim Wilson is only championing this super-for-homes policy because he and his partner, who own five residential properties between them, stand to gain financially from the associated uplift in values. Always follow the money.