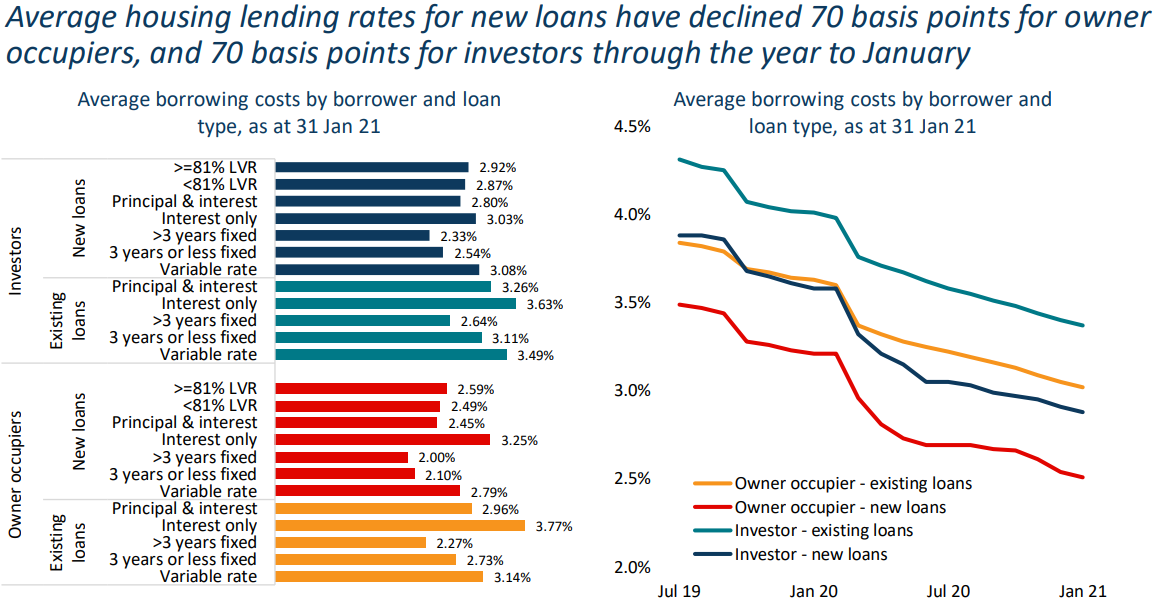

CoreLogic has released its March Housing Market Update report, which contains the below chart showing the sharp fall in mortgage rates over the past year across various owner occupied and investor loan types and terms.

Specifically, the average housing lending rates for new loans declined 70 basis points for owner occupiers, and 70 basis points for investors through the year to January 2021:

Mortgage rates fell sharply in the year to January across every loan type and term.

What should immediately spring to mind is the large gap between existing loans and new loan. The differences are listed below.

Owner Occupier Mortgages:

- Variable rate: new loans = 2.79%; existing loans = 3.14%; difference = 0.35%.

- 3-year or less fixed: new loans = 2.10%; existing loans = 2.73%; difference = 0.63%.

- Greater than 3-years fixed: new loans = 2.00%; existing loans = 2.27%; difference = 0.27%.

- Interest Only: new loans = 3.25%; existing loans = 3.77%; difference = 0.52%.

- Principal & Interest: new loans = 2.45%; existing loans = 2.96%; difference = 0.51%.

Investor Mortgages:

- Variable rate: new loans = 3.08%; existing loans = 3.49%; difference = 0.41%.

- 3-year or less fixed: new loans = 2.54%; existing loans = 3.11%; difference = 0.57%.

- Greater than 3-years fixed: new loans = 2.33%; existing loans = 2.64%; difference = 0.31%.

- Interest Only: new loans = 3.63%; existing loans = 3.03%; difference = 0.60%.

- Principal & Interest: new loans = 2.80%; existing loans = 3.26%; difference = 0.46%.

As you can see, serious mortgage savings are available if you look to refinance.

For example, a homeowner with a $500,000 mortgage that refinances from a typical existing variable mortgage at 3.14% to another provider at 2.79% could save around $1750 a year on interest repayments. Obviously, if they shop around they could find an even lower rate and achieve bigger savings.

They could also switch from variable to fixed, gaining bigger mortgage savings.

The point is that it pays to shop around for a better deal. Or at least call your lender and see whether they will drop your mortgage rate.