What next for bond and stock market crashes? Wall Street was mostly caught on the hop by the bond and stock crash so the wisdom of asking it at all is questionable. Let’s see what it has to say now. Goldman:

This week’s move has put the velocity of the real yield selloff on par with previous post-global financial crisis spikes: late 2016, 2015, and 2013.

Given the growth-driven nature of the selloff, we would view any subsequent material spread widening as an opportunity to add risk.

We also expect the recent decline in the beta of corporate bonds to equities will likely remain in place. Energy should close its recent performance gap with crude

Despite the recent rally in oil prices, Energy credit relative performance has been flat.

Current valuations and a strong oil market backdrop should continue to support the sector.

The recent performance gap should close, and were main overweight Energy in both the USD IG and HYmarkets.

That all makes sense to me. I expect yields will go higher yet as real inflation comes through though we are probably past the illiquid panic stage. The 2013 taper tantrum analogue is useful. After the initial spike, short-end yields calmed down for a bit and then ground higher as Fed tightening became a reality. Long-end yields ground higher for a while and then began to fall ceaselessly as Fed tightening raised recession odds. I think we’re likely to repeat that.

Goldman, therefore, sees more rotation to value ahead in stocks:

Advertisement

We retain a long recommendation in Value-Cyclicals– we consider these to be the most geared to economic improvement, re-opening, rising inflation risks and modestly higher bond yields. We remain OW Energy, Basic Resources and Banks.

Re-opening: Given our above-consensus view on economic growth we shift up some of the more cyclical/services consumer sectors, including Travel &Leisure and Beverages. Our favourite re-opening recommendations are: Energy(S600ENP), Travel & Leisure (SXTP),Beverages (GSSBBEVS), Aerospace(GSSBCIVA), Transport Infrastructure (GSSBTINF), Business Services(GSSBBUSC) and our Recovery basket (GSSTRCOV).

I agree with that, also, but not in the timeframe that Goldman sees. For me, it has maybe six months to run before inflation worries turn deflation as DXY firms and China slows, meaning it’s back to growth unless we see some more super-powerful MMT.

To underline this, Mizhuo already sees US yields as overshot:

Advertisement

The ongoing market sell-off does not yet seem to be at an end, and we are cautious that more volatility could lie ahead with the critical threshold in 5Y UST now broken. Yesterday saw rates trade higher across the curves, with the weakness led by the belly of the US curve. This suggested it was moving beyond a mere repricing of inflation and growth towards a convexity move, which may cause worries that the momentum of the sell-off will take on a life of its own,despite factors pointing towards lower yields, and tighter credit.

We have warned for some time that the5Y yield remaining below 0.75% was critical for risk assets to continue to benefit through the rebound. With the level now broken convincingly, it has driven simultaneous USD appreciation, and a sell-off across equities. 10Y UST yield found support at 1.50% (close to our FV for YE), and 10Y Gilts found a bid around 0.8%. Meanwhile, 30Y Gilts were bid through much of the weakness, closing only marginally up on the open. In EGBs, 10Y OAT are now positive yielding, while 10Y BTP/Bund spread broke convincingly up through 1%. Credit, too, moved concertedly wider, with ITRX Main CDS price closing above 50 and XO closing at 263. In OAS, EURIG was generically wider, while US remained comparatively tight. HY performance was more idiosyncratic, with energy leading the weakness.

Looking to the days ahead, we see good reasons for this current weakness to fade across credit and rates, but right now does not seem to be the right time to enter into the market. As stated previously, right now the risk-reward in tactical rates shorts does not look attractive, we advise reducing bear-steepening exposure but without switching to outright long, and holding off from entering into spread positions.

Again, like 2013, there is probably some more turmoil ahead. But it’s unlikely to represent the same violent volatility seen last week. It’s already right up there for historical moves, via BofA:

GOATs: past 12 months…equity rallyis GOAT, V-shape macro recovery is GOAT, bond bear market now one of greatest-of-all-time…since Aug 4th annualized price return from +10-year US govt bonds =-29%, Australia-19% (they do YCC!), UK-16%, Canada-10%; watch bank stocks “tell” bond rout hurting liquidity & growth expectations (Chart 2).

Flows: huge week of$46.2bn inflow to equities (3rdlargest ever), $7.1bn into bonds,$0.5bn out of gold, $5.5bn out of cash.

Flows to Know: record inflow to EM ($11.6bn to debt & equity), 2nd largest to materials ever ($2.3bn), 3rd largest to tech ever ($4.5bn), 4th largest to financials ever ($3.4bn); 1st chink inflows bull armor…largest outflow from HY bonds in 3 months ($1.7bn)

Advertisement

Similar thoughts come from the robot whisperers at Nomura. They see the major yield back-up already behind us:

Market moves so far have been driven by systemic trading players that have mostly rebalanced:

Advertisement

Higher yields will only kill the stock market and therefore recovery:

They expect yields to fall from here.

Advertisement

As said, I still think we can bounce around at higher yields for a while as real inflation prints come through so volatility will be here for a while and stock rotation should continue, pressuring growth but lifting value.

Finally, what of the Fed? Will it wade in? I don’t think it needs to. This is all pretty typical market adjustment stuff. And it could get more than it bargained for if it eggs on stimulus as bonds sell, with the scent of quantitative failure in the air. Long-end yields will calm down over time and any damage to US mortgage rates should reverse.

But, if it does get out of hand as actual inflation prints come through, TS Lombard looks at the Fed’s options:

Advertisement

To combat this risk, the Fed has one more ace up its sleeve: a front-loaded SOMA portfolio. In 2011 the Fed announced Operation Twist – selling $400bn of sub-3y debt to buy long-dated Treasuries – after growth had slipped, financial conditions had tightened and the equity market had fallen by 17%. And it worked: the programme flattened the yield curve, cut TP by 100bp and eased financial conditions. A twist now would be in a very different environment, aiming to cap rising yields (which may work in the short run, but stores up longer-term problems). But the ammunition is there: thanks to massive Bill-buying last year (when Treasury issued Bills to fund pandemic spending) the SOMA portfolio has $2.3trn of Treasuries with maturities under 3 years (c.f. $570bn in 2011).

Just as important, there are over $500bn of securities maturing between now and June. Simply rolling these holdings will extend the maturity of the Fed portfolio (ordinarily Treasury would roll these maturing bonds too, for no net effect, but as Treasury plans to draw down $1trn of cash deposited with the Fed in H1 this year, there is no matching supply roll). And foreign demand may also come in: yen-hedged Treasury yields are on a par with yen-hedged BTPs and not far off yenhedged Greek yields. Yield-hungry investors will be keen to take advantage of this bond sell-off.

Improving growth expectations are putting upward pressure on yields, raising the term premium and testing this risk rally. This pressure is tightening financial conditions and weighing on equities. If the economy meets current expectations, the Fed need not Twist. But with rising term premium and signs of market stress yesterday, the Fed must carefully consider its next steps – lest Chairman Powell (an FOMC member during the 2013 tantrum, and Chairman in 2018) adds yet another policy mistake to his FOMC roll call and wake the equity bear from hibernation, again. Where does the 10y go from here? It depends on what the Fed chooses to do, but if yields continue to rise quickly the equity market will fall. We’re not chasing yields higher.

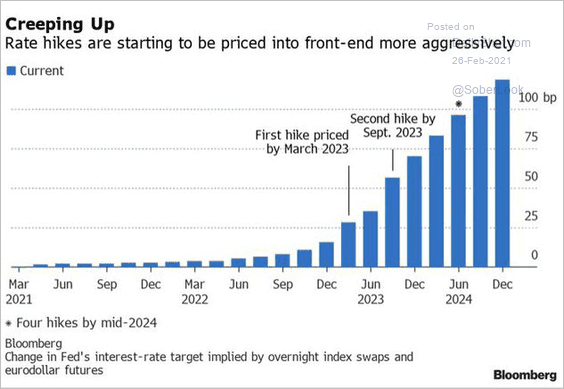

One has to remember that the Fed and market exist in tension not domination of one another. Thus it is often the market that calls the tune. Fed tapering expectations have been brought forward to early 2022. Rate hikes to later in the year:

Advertisement

My personal view is that this is overly aggressive given ongoing virus risks and the likelihood of fading Chinese growth and falling commodities in 2022, but it underlines the most crucial point emerging from last week’s bond rout.

It’s the first major market signal that growth, inflation and yield leadership of the post-COVID cycle is going to swing from China to the US in due course.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.