On Friday, the Senate Economics Committee released its assessment of the Morrison Government’s planned axing of responsible lending rules, which supported winding back regulations to support greater credit provision across the economy:

The committee notes that a well-functioning credit market is essential for economic growth generally, and for Australia’s recovery from the COVID-19 pandemic specifically. The committee agrees that the current consumer credit protection framework is potentially overly prescriptive and that regulatory duplication between the responsible lending obligations, under the Credit Act, and the prudential standards issued by APRA could be an issue.

The committee is concerned by evidence that the regulatory framework has resulted in consumers being unable to access credit in a timely manner to buy their first home or to obtain a grant under the HomeBuilder scheme. The committee is also concerned by the invasive and onerous nature of the inquiry and verification processes required under the existing responsible lending obligations…

The committee is of the view that these regulatory changes will not undermine consumer protections and that the principal of ‘responsible lending’ is deeply embedded in Australia’s broader regulatory framework, which credit providers and credit assistance providers must still operate within and comply with.

It must be noted that this Senate Committee was Coalition-led. Therefore, it is no surprise that it found in favour of Coalition policy.

What is particularly concerning about their assessment is that it directly contradicts the view of the exhaustive Hayne Banking Royal Commission (RC), which handed down its final report only two years ago and outlined numerous cases and examples of irresponsible and predatory lending.

In fact, the Hayne RC was so concerned about predatory lending that its very first recommendation was to ensure that existing responsible lending rules remain in place:

The Hayne Banking Royal Commission’s central recommendation was to keep responsible lending laws.

What’s the point of conducting RCs if the government that ordered the inquiry acts directly against its recommendations?

If the Morrison Government’s changes are passed by the Senate, it will represent the biggest relaxing of lending rules in a generation and act as a ‘red rag to a bull’ for Australia’s financial institutions to engage in sub-prime lending.

I would love to see Kenneth Hayne give his take on the reforms, particularly how the RC came to the polar opposite view. What has changed over the past two years to warrant scrapping the rules?

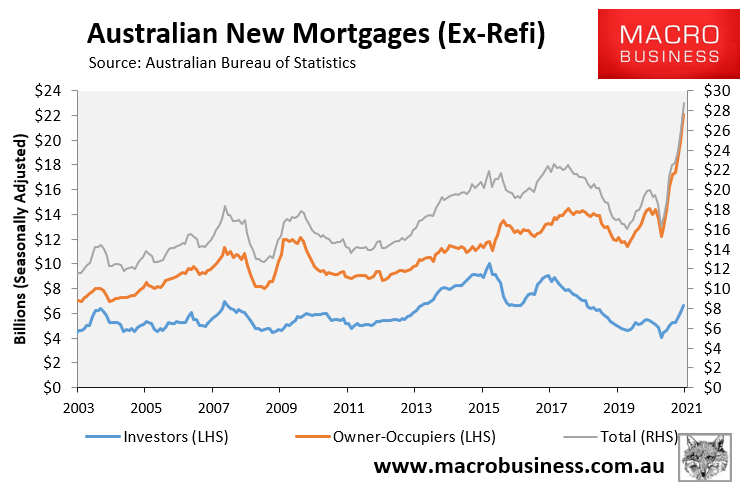

It is also difficult to argue that lending standards are too tight when the volume of new mortgage commitments are at a record high and Australian property prices are soaring.

New mortgage commitments are experiencing a record boom.

We can add the Council of Financial Regulators is on the move in the opposite direction, last week indicating that:

There has been some increased availability of mortgage finance recently, though lending standards are generally being maintained at this stage. The Council places a high emphasis on lending standards remaining sound, particularly in an environment of rising housing prices and low interest rates. It will continue to closely monitor developments and consider possible responses should lending standards deteriorate and financial risks increase.

So, if responsible lending is scrapped then it will immediately hasten macroprudential tightening with the two hands of government working at complete cross-purposes.

The National Consumer Credit Protection Amendment (Supporting Economic Recovery) Bill 2020 will be debated in the Senate today with the Bill reportedly on a knife’s edge. Labor and the Greens oppose the legislation, meaning the Bill’s fate will rest with the cross-bench.

Let’s hope the Senate upholds the Hayne Banking RC, blocks the legislation, and keeps responsible lending rules in place.