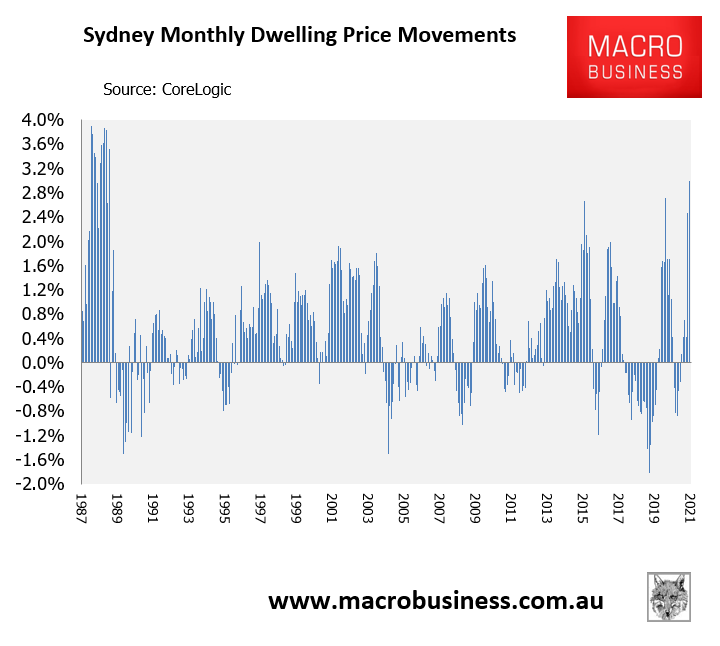

March is set to record Sydney’s strongest rise in dwelling values in 33 years, according to the CoreLogic daily index.

As at 24 March, and with one week to go before the end of the month, Sydney’s dwelling values have risen by 2.96%. And if the current pace of growth is maintained, Sydney could record dwelling value growth of around 3.5% for March 2021.

The next chart shows how March’s current rise in dwelling values compares with history:

The last time Sydney recorded monthly growth above 3% was in 1988.

The last time Sydney recorded monthly dwelling value growth above 3% was in October 1988 (3.5%).

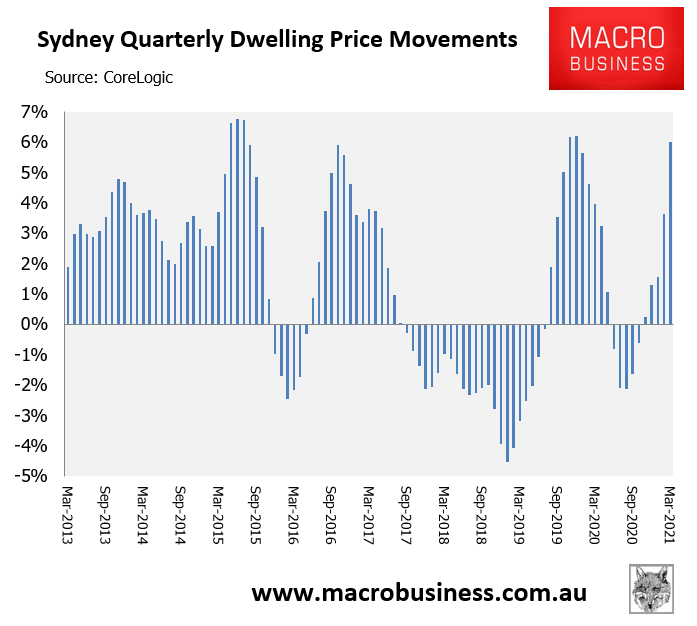

Quarterly Sydney dwelling value growth is also soaring, growing by 6.0% as at 24 March 2021. This is approaching the peak of recent price cycles:

Quarterly Sydney dwelling values are growing at 6%.

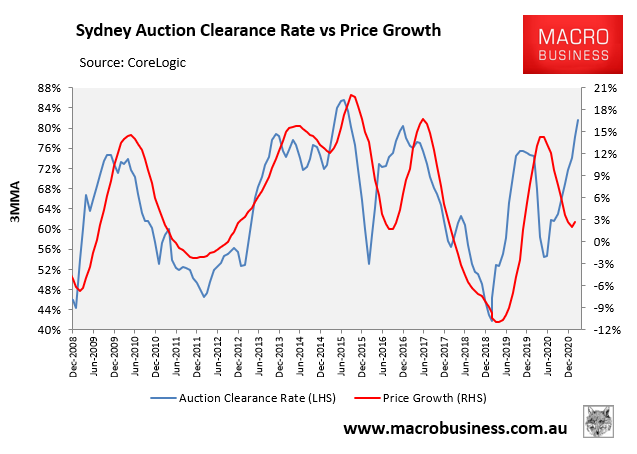

The immediate outlook for Sydney dwelling values is obviously very strong, with auction clearances now running above 80%. Based on past correlations, this suggests even stronger price growth for Sydney:

Sydney’s auction clearance rate is pointing to stronger property price growth.

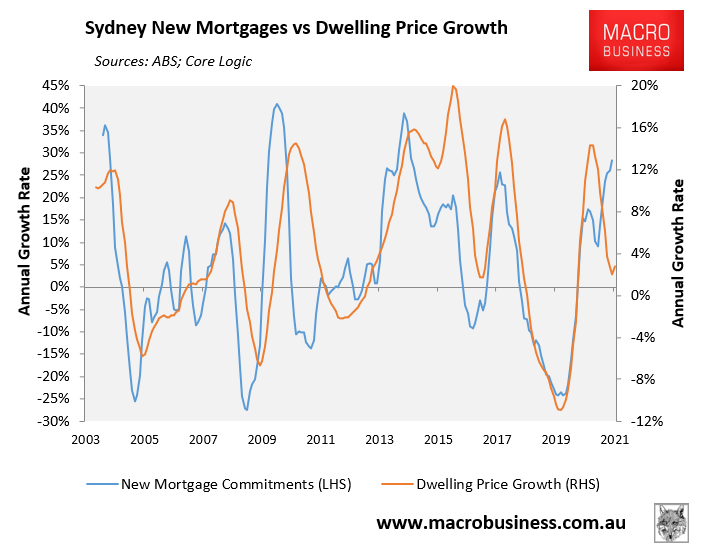

More importantly, the growth in new mortgage commitments has accelerated across Sydney, which also typically leads dwelling value growth:

The rebound in mortgage commitments points to strong price growth for Sydney property.

If the current momentum continues through the year (a big if), Sydney would register circa 25% price growth in 2021. The last time Sydney dwelling value growth peaked at 20% or above was in August 2015 (20.0%) and before that September 1989 (49.0%).

Therefore, Sydney is this year facing one of its biggest property price booms in generations.